3D Printing Ceramic Market Future Outlook and 22.75% CAGR Trends

Technological innovation is

transforming the global 3D Printing Ceramic Industry, with advancements in

materials science, printing techniques, and post-processing technologies

enabling the production of increasingly sophisticated ceramic components. Industries

seeking lightweight, durable, and high-temperature-resistant materials are

accelerating the adoption of ceramic additive manufacturing solutions.

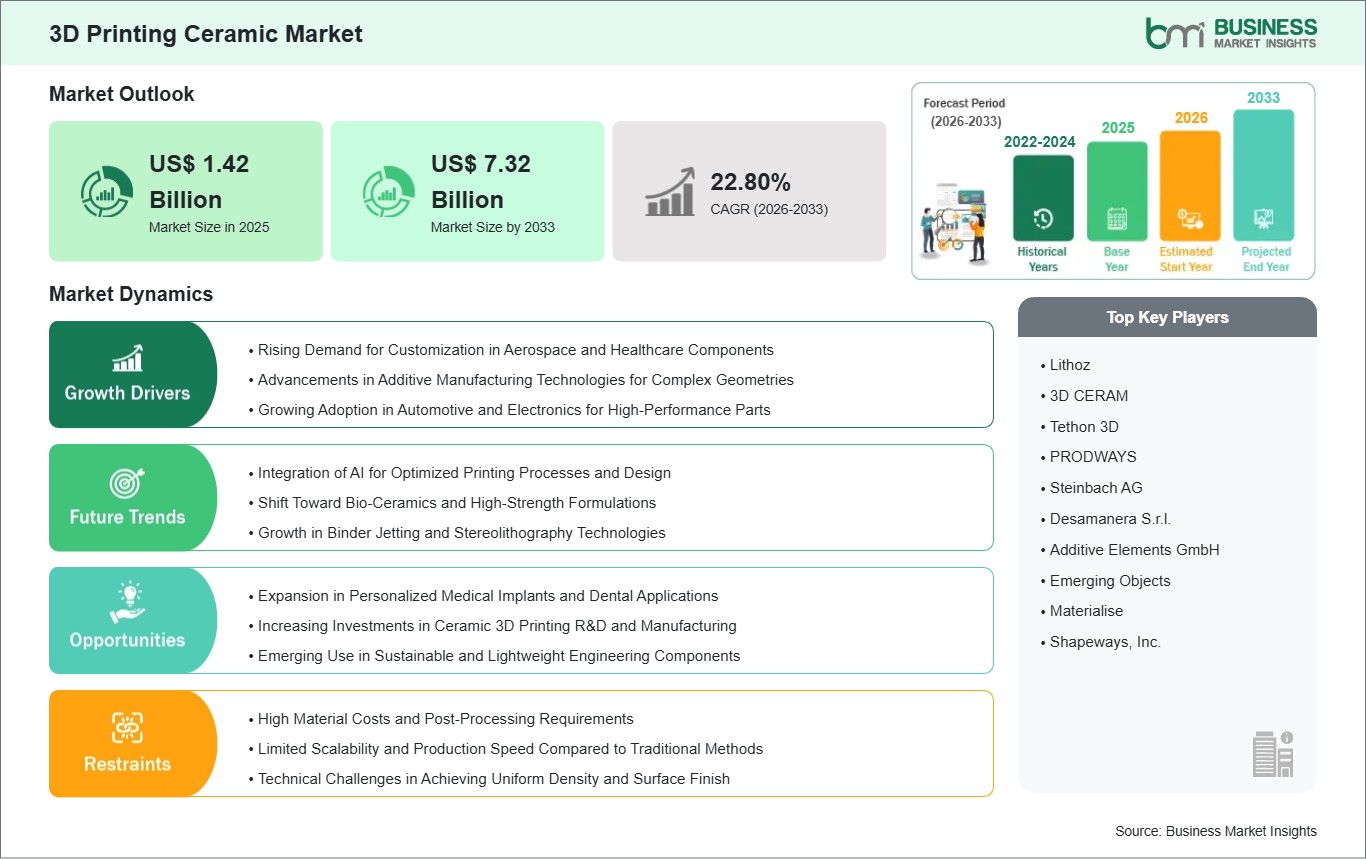

According to Business Market

Insights, the global 3D

Printing Ceramic Market was valued at US$ 1.42 billion in 2025 and

is anticipated to reach US$ 7.32 billion by 2033. The market is projected to

grow at a CAGR of 22.75% during the forecast period from 2026 to 2033.

Advancements in stereolithography

(SLA), digital light processing (DLP), binder jetting, and material extrusion

technologies are rapidly reshaping the competitive landscape. Leading advanced

materials corporations and digital manufacturing innovators are investing

heavily in improving slurry flow behaviors, developing multi-material ceramic

printers, and optimizing thermal post-processing cycles like debinding and

high-temperature sintering. These aggressive research and development outlays

are engineered to eliminate micro-structural defects, maximize sintered

material density, and deliver an exceptionally reliable, highly scalable

manufacturing framework that integrates smoothly with modern aerospace supply

chains, medical implant productions, and next-generation electronic

architectures.

What Is 3D Printing Ceramic

Technology?

3D printing ceramic technology

refers to an advanced additive manufacturing workflow that builds complex

ceramic structures layer-by-layer directly from three-dimensional

computer-aided design (CAD) models. Far exceeding the boundaries of traditional

ceramic processing, these modernized systems operate as high-precision digital

factories. They utilize sophisticated technical layers such as UV-curable

ceramic pastes, photopolymer resin suspensions, or fine ceramic powder beds

that capture intricate details at the micron level, transforming digital

geometric blueprints into solid, functional parts with zero material waste.

These critical industrial

manufacturing configurations employ distinct technical steps to achieve optimal

mechanical properties. In vat photopolymerization setups, a high-intensity

laser or light projector selectively cures a liquid resin packed with ceramic

particles, forming a "green body" part. This intermediate component

then undergoes a highly controlled thermal debinding phase to burn away the

polymer binders, followed by a high-temperature sintering cycle in an

industrial furnace. This final thermal process fuses the ceramic particles

together into a dense, fully consolidated structure, yielding a finished

component that boasts extreme hardness, excellent wear resistance, and the

ability to withstand intense thermal shocks.

Download Sample Report: https://www.businessmarketinsights.com/sample/BMIPUB00033223

Market Drivers

A primary driver accelerating the

global 3D Printing Ceramic Industry is the Expanding Adoption of

Additive Manufacturing and Digital Factory Infrastructure. Modern

industrial manufacturing sectors are universally forcing a transition toward

agile, toolless production models to compress product development timelines,

eliminate expensive hard-tooling storage requirements, and optimize complex

supply chains. Ceramic 3D printing fulfills these operational mandates

perfectly, allowing aerospace, automotive, and defense companies to print

custom, low-volume components on demand with significant cost-containment

benefits.

The skyrocketing demand for Customized

High-Performance Components across High-Tech Industries represents

another core market driver. Specialized sectors like medical diagnostics, space

exploration, and chemical processing require unique, customized parts that can

reliably perform under high-stress, corrosive, or extreme temperature settings.

Whether it is custom-shaped bioceramic bone implants matching a patient's exact

anatomy or specialized thruster nozzles for micro-satellites, additive ceramic

tech provides the precise design freedom needed to meet these complex

engineering goals.

Additionally, rapid Advancements

in Material Formulations and a Focus on Manufacturing Sustainability serve

as a powerful catalyst. Material scientists are consistently developing new,

easily printable ceramic slurries utilizing alumina, zirconia, silicon carbide,

and hydroxyapatite. These innovative formulations are increasingly paired with

sustainable, eco-friendly binding agents that lower emissions during the

debinding phase, while the inherent additive nature of the printing process

dramatically reduces raw material waste compared to traditional subtractive

milling methods.

Market Segmentation

By Material Type

- Oxide

Ceramics (Commanding a dominant revenue share globally, heavily led by

alumina and zirconia formulations due to their exceptional

biocompatibility, deep structural reliability, and widespread use in

medical and electrical industries)

- Non-Oxide

Ceramics (Tracking exceptional growth trends across aerospace and defense

sectors, utilizing silicon carbide and silicon nitride to provide extreme

thermal resistance and structural durability under harsh loads)

By Technology

- Vat

Photopolymerization (SLA/DLP) (The premier technology segment by volume,

favored for its ability to deliver ultra-high surface finishes, superior

dimensional accuracy, and highly dense final ceramic components)

- Binder

Jetting (Securing a substantial market footprint, highly valued for its

fast build speeds and capability to manufacture large-scale structural

ceramic parts without requiring support structures)

- Material

Extrusion & Jetting (Expanding steadily as an accessible,

cost-effective alternative for localized prototyping, specialized tooling,

and custom industrial component trials)

By End-Use Industry

- Medical

and Healthcare (The fastest-growing application vertical, driven by

high-value custom dental restorations, bone graft scaffolds, and

personalized orthopedic implants utilizing biocompatible ceramics)

- Aerospace

and Defense (Securing massive procurement budgets for printing lightweight

thermal protection tiles, intricate turbine blades, and high-temperature

fluid-handling components)

- Electronics

and Electrical (Utilizing precision 3D printing to create highly intricate

electrical insulators, customized semiconductor handling equipment, and

advanced substrate boards)

- Automotive

and Energy (Deploying additive ceramics for high-wear engine valves,

specialized exhaust sensors, and durable solid oxide fuel cell components)

Regional Insights

- North

America holds the premier position in the global landscape,

securing a dominant market share in 2025. This regional leadership is

anchored by an exceptionally dense cluster of advanced aerospace

enterprises, massive defense engineering projects, and a highly

progressive medical device sector backing early adoption of advanced

additive technologies across the United States.

- Europe exhibits

a highly robust, mature market footprint, characterized by deep industrial

automation integration, highly advanced fine ceramic material processing

networks, and strict technical validation frameworks across Germany,

France, and the UK.

- Asia-Pacific represents

the fastest-growing geographical segment, projected to expand at an

explosive double-digit CAGR through the forecast window. This rapid

scaling is fueled by widespread industrial digitalization, massive

consumer electronics manufacturing hubs across China, Japan, and South

Korea, and strong government-backed initiatives supporting advanced

additive manufacturing tech.

- Rest

of the World is displaying steady, progressive growth patterns,

driven by ongoing manufacturing infrastructure upgrades and targeted

adoptions of advanced tooling techniques across Latin American and Middle

Eastern industrial hubs.

Top Players in the Industry

The competitive ecosystem displays

a sophisticated matrix of specialized additive manufacturing equipment

builders, advanced industrial ceramic suppliers, and integrated engineering

service bureaus executing long-term commercial supply agreements with global

tier-one manufacturers.

- 3D

Ceram

- Lithoz

GmbH

- Prodways

Group

- ExOne

(The Digital Manufacturing Chemical Company)

- XJet

Ltd.

- Admatec

(Nano Dimension)

- Formlabs

Inc.

- Voxeljet

AG

- Kyocera

Corporation

- CeramTec

GmbH

Technological Innovations

The commercial implementation of

advanced Multi-Material Ceramic Printing and Integrated Multi-Light

Engine SLA Systems represents a monumental engineering breakthrough

for the ceramic additive sector. Historically, 3D printers were strictly

limited to processing a single material type per build cycle, preventing the

creation of integrated smart parts. Next-generation systems employ advanced

jetting or multi-vat layouts to deposit distinct ceramic formulations such as

alternating layers of insulating alumina and conductive tracking materials

within a single component. This structural capability enables the direct

printing of smart ceramic parts with built-in circuitry, drastically lowering

post-assembly requirements and opening up massive design paths for the

electronics and aerospace fields.

Concurrently, the integration

of AI-Driven Sintering Simulation and Automated Tomography Quality

Controls is completely modernizing the industrial production

landscape. Because ceramics shrink by up to 15% to 22% during the

high-temperature sintering furnace phase, predicting and preventing dimensional

distortion or internal cracking has always been a primary manufacturing

bottleneck. Modern software platforms leverage advanced machine learning models

to simulate thermal shrinkage dynamics pre-operatively, automatically altering

the initial "green" print geometry to ensure the final sintered part

meets perfect tolerances, minimizing scrap rates and accelerating production

throughput.

Future Market Outlook

The long-term trajectory for the

3D Printing Ceramic Market remains exceptionally robust. As international

engineering specifications permanently validate additive ceramics for critical

structural duties in aerospace propulsion and deep-tissue medical implants, and

global industrial supply chains move permanently toward distributed, digital

on-demand manufacturing setups, the universal reliance on advanced ceramic 3D

printing solutions will expand continuously.

Future research and development

capital will be heavily directed toward the commercialization of ultra-fast

binder jetting platforms optimized for high-volume mass production, the

refinement of hybrid laser-sintering heads that combine printing and partial

densification into a single machine step, and the expansion of affordable,

sub-micron resolution desktop printers for specialized dental labs. Technology

developers that successfully bridge the gap between complex thermal

post-processing management and competitive, accessible machinery pricing models

will comfortably secure long-term global market leadership.

Frequently Asked Questions

(FAQs)

What is the projected valuation

of the global 3D printing ceramic market by 2033?

The global 3D printing ceramic

market is projected to reach an estimated valuation of US$ 7.32 Billion by

2033, expanding rapidly from its established value of US$ 1.42 Billion in 2025.

What is the expected compound

annual growth rate (CAGR) of the market over the forecast timeline?

The market is anticipated to

expand at a powerful Compound Annual Growth Rate (CAGR) of 22.8% globally

during the forecast period spanning from 2026 through 2033.

Why is the medical and

healthcare sector adopting 3D printed ceramics so quickly?

The medical sector utilizes 3D

printed ceramics because materials like zirconia and alumina match the natural

wear resistance and high strength needed for dental restorations and bone

implants, while the additive process allows for custom, patient-specific

matching.

What are the primary technical

challenges associated with 3D printing ceramics?

The core challenges lie in the

complex post-processing phases, where parts must undergo careful thermal

debinding and high-temperature sintering. Managing the significant volumetric

shrinkage that occurs during these stages is vital to avoid part distortion or

internal micro-cracks.

Browse More Reports:

About Us

Business Market Insights is a

market research platform that provides subscription service for industry and

company reports. Our research team has extensive professional expertise in

domains such as Electronics & Semiconductor; Aerospace & Defense;

Automotive & Transportation; Energy & Power; Healthcare; Manufacturing

& Construction; Food & Beverages; Chemicals & Materials; and

Technology, Media, & Telecommunications.

Contact Us

If you have any questions about

this report or would like further information, please contact us:

Contact person: Ankit Mathur

Email: sales@businessmarketinsights.com

Phone: +16467917070

Comments

Post a Comment