Airborne Collision Avoidance System Market Future Outlook and 5.62% CAGR Trends

Technological innovation is

reshaping the global Airborne Collision Avoidance System Industry, with

manufacturers developing sophisticated surveillance, tracking, and alerting

solutions that enhance pilot decision-making and operational safety. Advancements

in avionics, sensor fusion, and air traffic management systems are supporting

the widespread adoption of next-generation collision avoidance platforms.

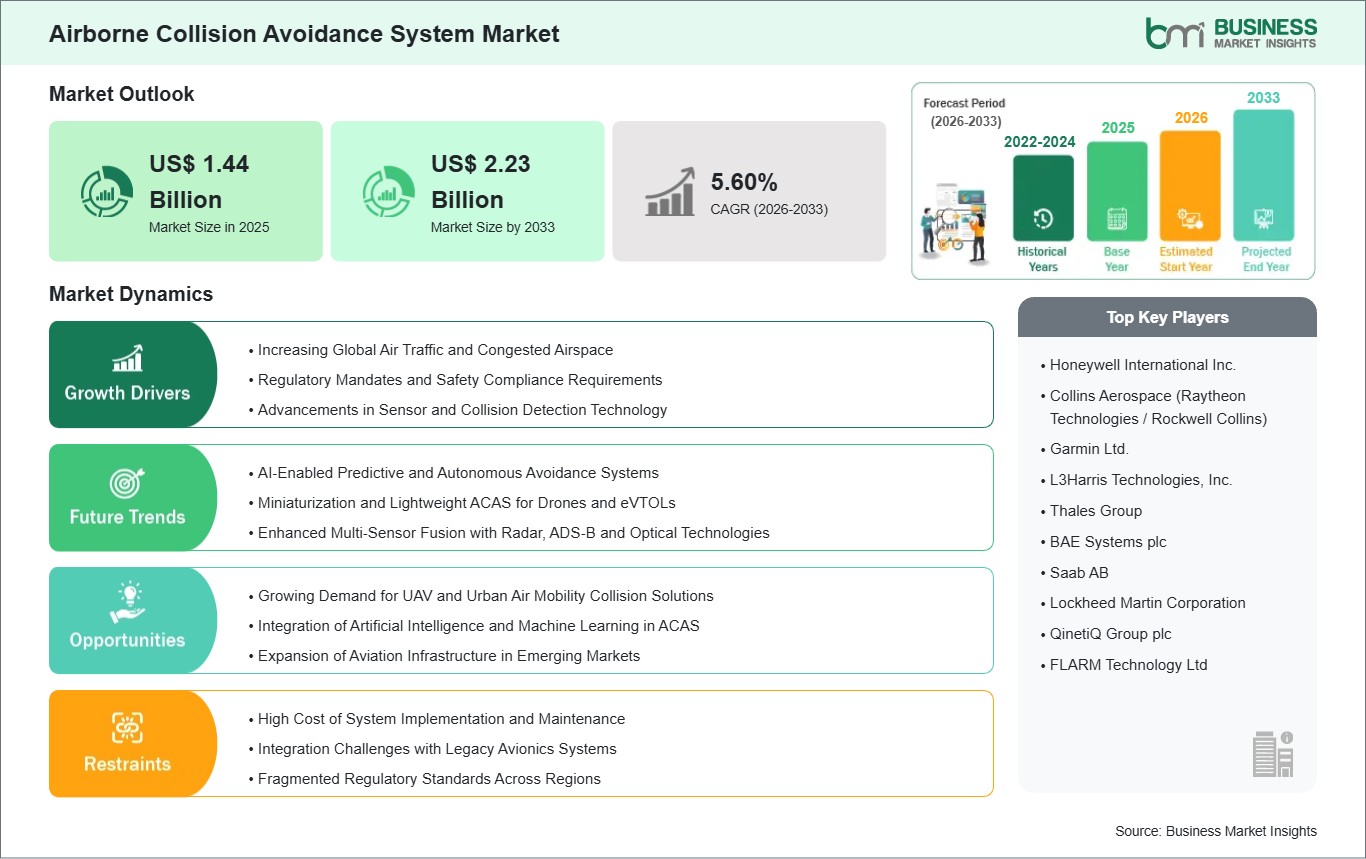

According to Business Market

Insights, the global Airborne

Collision Avoidance System Market was valued at US$ 1.44 billion in

2025 and is anticipated to reach US$ 2.23 billion by 2033. The market is

projected to grow at a CAGR of 5.62% during the forecast period from 2026 to

2033.

As advanced glass cockpits become

standard across regional and international fleets, modern ACAS architectures

act as a crucial line of safety defense against mid-air collisions. By actively

interrogating the transponders of nearby aircraft via specialized radio

frequencies, these systems map regional airspace in real time, calculate

potential flight path intersections, and issue split-second automated

Resolution Advisories (RAs) to pilots. Capital investment within the industry

is heavily focusing on multi-sensor data fusion, blending radar, ADS-B

(Automatic Dependent Surveillance-Broadcast), and cooperative transponder feeds

into a single unified safety stream.

What Are Airborne Collision

Avoidance Systems?

Airborne Collision Avoidance

Systems (ACAS) are specialized aircraft avionics arrays designed to operate

independently of ground-based air traffic control (ATC) infrastructure. These

systems function by continuously broadcasting interrogation signals and

listening for responses from transponders equipped on other nearby aircraft. By

calculating the time delay, signal frequency shift, and directional vector of

the reply, the onboard ACAS computer establishes a real-time relative position

matrix of surrounding air traffic.

If the system detects an impending

conflict where the horizontal and vertical separation boundaries are

compromised, it acts as a tiered safety shield. It first issues a visual and

auditory Traffic Advisory (TA) to alert the flight crew of nearby traffic. If

the collision risk escalates, the system elevates the warning to a Resolution

Advisory (RA), providing explicit vertical maneuver instructions (such as

"Climb" or "Descend") natively on the primary flight

display to guide the pilots along a safe evasive path.

Download Sample Report: https://www.businessmarketinsights.com/sample/BMIPUB00033251

Market Drivers

A primary driver accelerating the

global ACAS Industry is the Transition to Next-Generation ACAS X

Architecture. The global aviation industry is actively transitioning from

legacy TCAS II architectures to the next-generation ACAS X framework. While

traditional systems rely on rigid, pre-programmed, rule-based lookup tables

that often trigger unnecessary warnings, ACAS X utilizes dynamic, probabilistic

models and advanced software-defined algorithms. This optimization improves

collision avoidance efficiency by approximately 30%, drastically minimizing

"nuisance" alerts in highly congested terminal radar service areas

and allowing closer, safer aircraft separation profiles near major global

airport hubs.

The Proliferation of

Autonomous Systems and Advanced Air Mobility (AAM) serves as another

core driver. The massive expansion of commercial drone applications across

logistics, agricultural monitoring, and critical infrastructure inspection is

structurally altering market demand. UAV platforms require robust "detect

and avoid" capabilities to safely navigate non-segregated commercial

airspace. Additionally, the emergence of electric vertical takeoff and landing

(eVTOL) systems designed for urban air mobility has created an entirely new

pipeline for certified, low-power, lightweight collision avoidance modules

tailored for dense, low-altitude city environments.

Additionally, Regulatory

Compliance and Fleet Modernization Mandates remain primary market

catalysts. Stricter safety mandates issued by international regulatory

authorities, including the Federal Aviation Administration (FAA) in the United

States and the European Union Aviation Safety Agency (EASA) in Europe, require

commercial passenger liners, cargo transports, and high-capacity regional

aircraft to be equipped with interoperable transponder networks. New

operational guidelines require continuous tracking updates, forcing extensive

hardware retrofits and aftermarket upgrades across aging commercial fleets.

Market Segmentation

By System Type

- Traffic

Collision Avoidance Systems (TCAS) (Maintained a dominant position with a

38.4% market share in 2025, sustained by long-standing global mandates for

commercial passenger aircraft transport)

- Airborne

Collision Avoidance Systems (ACAS) (Represents the fastest-accelerating

segment with a projected 9.1% CAGR, propelled by software-defined ACAS X

upgrades and military transport installations)

- FLARM

& Portable Systems (PCAS) (Combines for over 25% of total market

revenue, providing highly cost-effective, ultra-lightweight safety layers

tailored for general aviation, gliders, and private light-sport aircraft

operators)

By Platform

- Commercial

Aircraft (Commands the largest overall presence at 42.6% market share,

driven by the persistent recovery and expansion of international tourism

and commercial fleet expansions)

- Military

Aircraft (Secures a major share of 27.3%, backed by tactical data-link

integration, defense modernization programs, and the deployment of

collision avoidance layers within high-performance fighters and strategic

airlifters)

- Unmanned

Aerial Vehicles (UAVs) (Tracks the highest forward growth index at 12.4%

CAGR, as regulatory frameworks require commercial drones to possess robust

airspace awareness capabilities)

By Component Architecture

- Transponders

(Mode S/ADS-B) (Controls 39.8% of the component market share, operating as

the essential transceiver backbone required for active signal broadcasting

and vehicle-to-vehicle coordinate exchange)

- High-Performance

Processors (Expanding at a 7.8% CAGR due to the intensive computing

demands required to execute complex machine-learning vision algorithms and

real-time flight trajectory analytics)

- Display

Units & Cockpit Interfaces (Comprising 19.6% of the sector, this

segment focuses heavily on integrating visual resolution advisory vectors

natively into primary flight displays)

Regional Insights

- North

America holds the premier position globally with a commanding 35%

market share. This leadership is anchored by the immense operational scale

of domestic airlines, high general aviation penetration, and continuous

NextGen air traffic management system rollouts by the FAA.

- Europe captures

28% of global revenues, supported by strict compliance structures under

EASA, a highly unified airspace architecture, and anchor Tier-1 aerospace

supply chains across Germany, France, and the United Kingdom.

- Asia-Pacific is

positioned as the fastest-accelerating geographic theater, expanding at an

impressive localized sub-CAGR of 9.2%. Rapid commercial fleet growth in

China and India, coupled with expanding domestic defense allocations,

underpins this regional surge.

- Rest

of the World accounts for the remaining 12% market share,

displaying progressive growth patterns driven by sovereign smart-airport

overhauls and massive long-haul fleet expansions across major Middle

Eastern transportation hubs.

Top Players in the Industry

The competitive ecosystem of the

ACAS sector is characterized by intense consolidation among established, tier-1

defense and aerospace electronics conglomerates. Key market strategies involve

creating tightly coupled hardware-software ecosystems capable of sensor fusion.

- Honeywell

International Inc.

- Collins

Aerospace (RTX Corporation)

- L3Harris

Technologies, Inc.

- Garmin

Ltd.

- BAE

Systems plc

- Saab

AB

- Thales

Group

- Lockheed

Martin Corporation

Strategic Industry Challenges

Despite high enterprise demand,

widespread market deployment is restricted by steep upfront capital intensity.

Upgrading legacy avionics to next-generation ACAS X systems introduces

significant integration complexities, with operators reporting an average 25%

increase in installation overhead costs. Furthermore, routine lifecycle

maintenance, multi-modal calibrations, and mandatory regulatory testing account

for approximately 20% of total system lifecycle expenses, creating an adoption

barrier for small regional carriers and general aviation pilots.

Future Market Outlook

The long-term trajectory for the

Airborne Collision Avoidance System Market remains highly resilient as civil

and commercial airspace grows increasingly dense. The ongoing intersection of

AI software analytics, miniaturized microelectronics, and multi-sensor data

arrays ensures that collision avoidance technologies will remain an absolute

baseline requirement for global aviation safety operations through the coming

decades.

Frequently Asked Questions

(FAQs)

What is the projected size of

the global ACAS market by 2034?

The market is projected to reach

an estimated valuation of USD 5.1 Billion by 2034, growing from an established

base of USD 2.8 Billion in 2025.

What makes ACAS X superior to

legacy TCAS II systems?

ACAS X replaces rigid lookup

tables with probabilistic models and software-defined algorithms, reducing

unnecessary "nuisance alerts" by 30% and improving overall spatial

safety in congested flight corridors.

Which regional market is

expanding at the fastest rate?

The Asia-Pacific region is the

fastest-growing geographical market, expanding at a CAGR of 9.2% due to massive

fleet expansions in China and India.

Browse More Reports:

Data Center Construction Market

About Us

Business Market Insights is a

market research platform that provides subscription service for industry and

company reports. Our research team has extensive professional expertise in

domains such as Aerospace & Defense; Automotive & Transportation;

Electronics & Semiconductor; Energy & Power; Healthcare; Manufacturing

& Construction; Food & Beverages; Chemicals & Materials; and

Technology, Media, & Telecommunications.

Contact Us

If you have any questions about

this report or would like further information, please contact us:

Contact person: Ankit Mathur

Email: sales@businessmarketinsights.com

Phone: +16467917070

Comments

Post a Comment