Blood Glucose Monitoring System Market Future Outlook and 9.67% CAGR Trends

Technological innovation is

reshaping the global Blood Glucose Monitoring System Industry, with

manufacturers developing next-generation biosensors and connected healthcare

platforms that enable real-time glucose tracking and personalized diabetes

management. Increasing integration with smartphones, cloud-based applications,

and digital health ecosystems is further accelerating market growth.

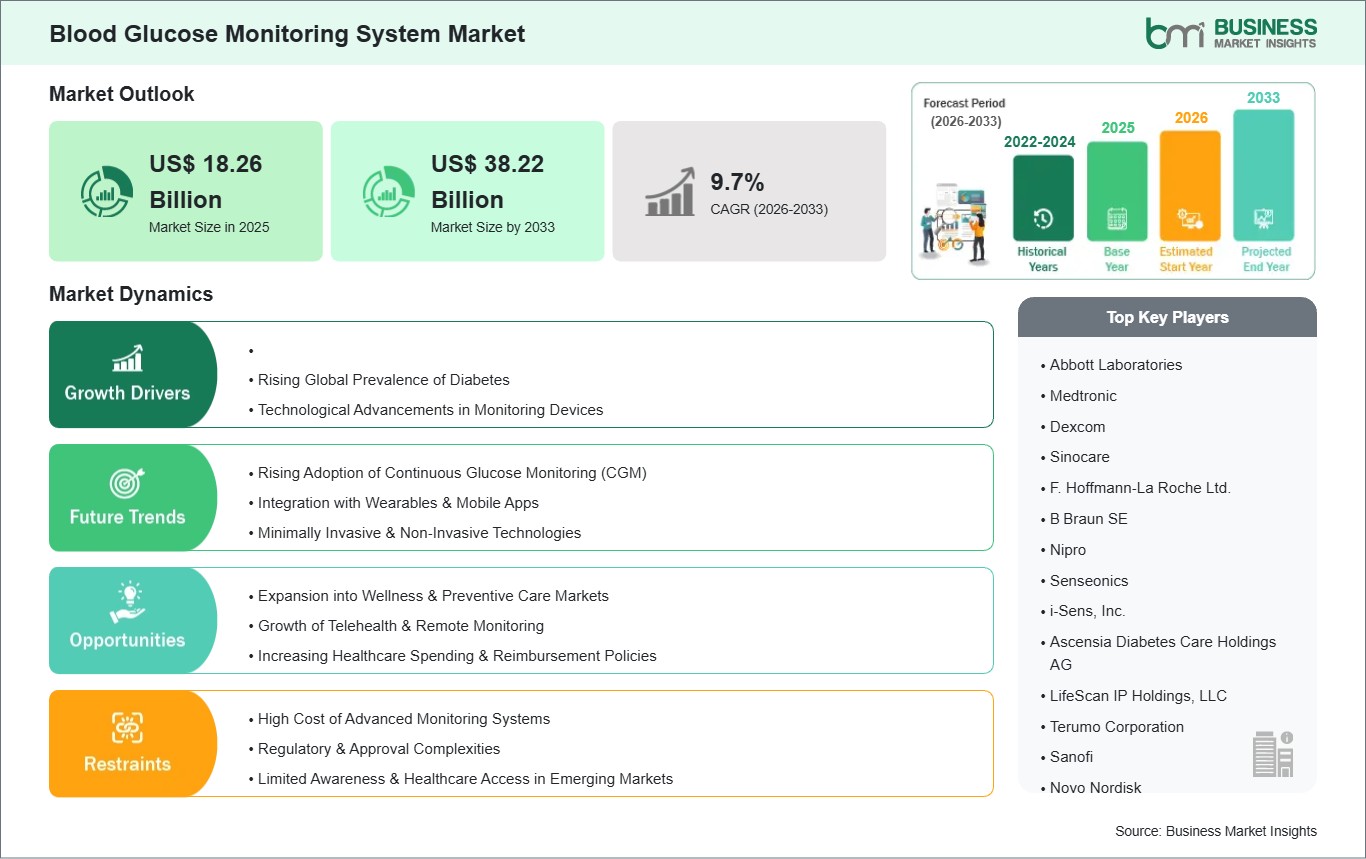

According to Business Market

Insights, the global Blood

Glucose Monitoring System Market was valued at US$ 18.26 billion in

2025 and is anticipated to reach US$ 38.22 billion by 2033. The market is

projected to grow at a CAGR of 9.67% during the forecast period from 2026 to

2033.

Advancements in transcutaneous

electrochemical sensors, Bluetooth Low Energy (BLE) telemetry, algorithm-driven

trend analysis, and automated insulin pump integration are fundamentally

altering the market competitive landscape. Leading medical device conglomerates

and digital health innovators are investing heavily in improving enzymatic

sensor longevity, developing non-invasive optical spectroscopy sensing

platforms, and establishing secure cloud-hosted dashboards for real-time

patient-provider visibility. These aggressive research and development outlays

are explicitly designed to overcome historic patient compliance barriers,

eliminate manual calibration errors, and deliver an integrated, closed-loop

metabolic ecosystem that bridges clinical triage with daily at-home patient

self-management.

What Is a Blood Glucose

Monitoring System?

A blood glucose monitoring system

is a dedicated diagnostic platform designed to quantify the concentration of

glucose within a patient's biological fluids, serving as a critical tool for

metabolic regulation and glycemic control. Moving far beyond the constraints of

periodic lab-based testing, contemporary monitoring systems act as a real-time,

dynamic sensor grid. These technologies integrate sophisticated hardware

layers including glucose oxidase or dehydrogenase enzyme reagents,

micro-needle insertion mechanisms, and low-power processing

transmitters that record biochemical shifts at the cellular level and

instantly convert them into clear, actionable metrics regarding metabolic

stability.

These critical medical tracking

setups utilize distinct modalities to manage metabolic data profiles safely. In

self-monitoring configurations, disposable strip architectures use

electrochemical capillary suction to generate a small electrical current proportional

to the blood glucose volume, sending accurate readings to a portable reader

within seconds. Concurrently, continuous monitoring models employ flexible

subcutaneous sensors that continuously evaluate interstitial fluid glucose

values, automatically transmitting data packets to mobile applications or

integrated insulin pumps every few minutes. This allows individuals and medical

teams to detect glycemic trends, predict immediate risks of hypoglycemia, and

adjust clinical strategies seamlessly.

Download Sample Report: https://www.businessmarketinsights.com/sample/BMIPUB00033209

Market Drivers

A primary driver accelerating the

global Blood Glucose Monitoring System Industry is the Surge in the

Global Diabetic Population and Growing Metabolic Health Awareness.

Sedentary modern lifestyles, shifting dietary trends, and rising global obesity

rates have led to an unprecedented surge in Type 1 and Type 2 diabetes cases

across both developed and developing regions. Because chronic glycemic

volatility leads to major medical complications if left unmanaged, public

health organizations and clinical teams are universally enforcing strict,

frequent glucose monitoring regimens, creating a sustained, high-volume demand

for reliable diagnostic equipment globally.

The clear clinical shift

toward Continuous Glucose Monitoring (CGM) Adoption and Outpatient Care

Frameworks represents another core market driver. Healthcare systems

and private insurance providers are focusing heavily on reducing expensive

hospital readmissions driven by sudden metabolic crises. Traditional

finger-stick testing provides only a single point-in-time reference, frequently

missing dangerous overnight or post-meal glucose spikes. Next-generation CGM

arrays address this diagnostic gap by providing 24/7 continuous data tracking,

encouraging proactive patient self-management and allowing clinics to manage

expanding patient groups remotely with exceptional safety margins.

Additionally, the rapid

convergence of Digital Tools, Wearables, and Closed-Loop Delivery

Networks serves as a powerful market catalyst. Modern consumers expect

medical technology to integrate smoothly with their daily personal devices.

Next-generation monitoring systems connect directly via Bluetooth to

smartphones, smartwatches, and automated insulin pumps to form "artificial

pancreas" systems. This structural connectivity automates insulin delivery

based on real-time glucose changes, removing manual user calculation errors and

substantially improving patient treatment adherence.

Market Segmentation

By Product Type

- Continuous

Glucose Monitoring (CGM) Systems (Commanding the highest growth trajectory

and securing a dominant revenue share due to rapid technological adoption,

longer sensor wear times, and high recurring consumable reorders)

- Self-Monitoring

Blood Glucose (SMBG) Systems (Maintaining a large, stable baseline volume

globally, especially within budget-conscious consumer segments and regions

requiring lower-cost diagnostic solutions)

By Testing Site

- Fingertip

Testing (The historical market standard for SMBG systems, securing

significant volume due to established clinical training patterns and

consumer familiarity)

- Alternate

Site Testing (Gaining consistent market interest by allowing fluid

collection from the palm, forearm, or upper arm to significantly reduce

patient injection pain and tissue scarring)

By Indication

- Type-2

Diabetes (The largest indication segment by volume, expanding rapidly due

to rising global diagnosis rates linked to changing lifestyles and aging

demographics)

- Type-1

Diabetes (Exhibiting intensive, high-value product penetration due to the

absolute clinical necessity for intensive, continuous glucose tracking and

integrated insulin pump therapy)

- Gestational

Diabetes & General Wellness (An emerging growth segment driven by

specialized maternal care protocols and health-conscious consumers

tracking metabolic efficiency)

By Distribution Channel

- Retail

Sales (The dominant distribution channel, holding over 79% of the consumer

market through pharmacy chains, online medical stores, and

direct-to-consumer e-commerce fulfillment)

- Institutional

Sales (Encompassing volume supply procurement across hospitals,

specialized diabetes clinics, long-term care facilities, and

multi-specialty diagnostic centers)

Regional Insights

- North

America holds the premier position in the global landscape,

securing a dominant market share of over 44.20% in 2025. This leadership

is sustained by high per-capita healthcare spending, strong commercial

reimbursement support for advanced CGM platforms, and rapid clinical

adoption of smart medical technologies across the United States.

- Europe exhibits

a highly structured, substantial market footprint, supported by clear

public healthcare frameworks, centralized diabetic care initiatives, and

extensive regional approvals for next-generation, non-invasive glucose

monitoring technologies.

- Asia-Pacific represents

the fastest-growing geographical segment, projected to expand at a

double-digit CAGR through 2034. This rapid scaling is propelled by massive

population bases in China and India, expanding medical distribution

networks, and rising disposable incomes that allow consumers to transition

to premium self-care tech.

- Rest

of the World is showing steady, progressive growth patterns,

driven by targeted government diabetes awareness campaigns in the Middle

East and ongoing expansions of retail pharmacy networks across Latin

American urban business hubs.

Top Players in the Industry

The competitive ecosystem displays

a sophisticated matrix of diversified medical technology conglomerates and

specialized biosensor innovators executing long-term ecosystem integration

strategies with digital health platforms and global retail pharmacy networks.

- Abbott

Laboratories

- Dexcom,

Inc.

- Medtronic

plc

- F.

Hoffmann-La Roche Ltd.

- Ascensia

Diabetes Care

- LifeScan

IP Holdings, LLC

- Senseonics

Holdings, Inc.

- Terumo

Corporation

- B.

Braun Melsungen AG

- Sinocare

Inc.

Technological Innovations

The commercial development of

advanced Implantable Long-Term Sensors and Enzyme-Free Biosensing

Layouts represents a monumental engineering breakthrough for the blood

glucose monitoring sector. Historically, standard continuous sensors required

users to replace transcutaneous needles every 7 to 14 days, creating persistent

skin irritation, compliance fatigue, and substantial ongoing medical waste.

Next-generation subcutaneous optical sensors utilize unique fluorescent

chemistry to remain fully functional inside the tissue for up to 180 days from

a single minor outpatient insertion. This gives patients continuous diagnostic

coverage, reduces sensor calibration tasks, and minimizes regular interaction

hassles for the user.

Concurrently, the transition

toward Non-Invasive Optical Spectroscopy and Electromagnetic Tracking is

completely modernizing the consumer diagnostic landscape. To completely

eliminate the physical pain and infection risks associated with traditional

skin-piercing needles, innovators are developing wearable form factors that

analyze blood glucose levels through the skin using infrared light and

radiofrequency waves. By measuring changes in optical absorption and electrical

impedance caused by shifting blood glucose levels, these advanced systems

enable continuous, painless monitoring, opening up massive growth paths across

consumer wellness markets and pediatric care networks globally.

Future Market Outlook

The long-term trajectory for the

Blood Glucose Monitoring System Market remains exceptionally robust. As

international healthcare guidelines permanently cement early, continuous

glycemic tracking as a core standard of care for metabolic disorders and global

corporate wellness programs expand their adoption of metabolic metric tracking,

the universal reliance on smart glucose monitoring systems will grow

continuously, establishing baseline parameters across modern diagnostic health

sciences.

Future research and development

capital will be heavily directed toward the commercialization of multi-analyte

wearable sensors capable of tracking glucose, lactate, and ketones

simultaneously from a single skin patch, the deployment of AI-powered predictive

telemetry to alert users of impending glycemic dips hours in advance, and the

optimization of ultra-low-cost non-invasive smart rings. Technology developers

that successfully balance high clinical diagnostic accuracy with accessible,

budget-friendly consumer pricing models will comfortably secure long-term

global market leadership.

Frequently Asked Questions

(FAQs)

What is the projected valuation

of the global blood glucose monitoring system market by 2034?

The global market is projected to

reach a valuation of US$ 59.87 Billion by 2034, expanding significantly from

its established baseline valuation of approximately US$ 23.45 Billion in 2025.

What is the expected compound

annual growth rate (CAGR) of the market over the forecast window?

The global blood glucose

monitoring system market is anticipated to expand at a powerful Compound Annual

Growth Rate (CAGR) of 10.75% during the forecast timeline spanning from 2026

through 2034.

Why is the continuous glucose

monitoring (CGM) segment outperforming traditional self-monitoring (SMBG)

systems?

CGM systems outperform traditional

options because they provide continuous, 24/7 real-time tracking of glucose

trends and supply critical data warnings for hypoglycemia, completely replacing

the limited, single point-in-time snapshots offered by manual finger-prick

methods.

Which regional market currently

commands the largest revenue share in the glucose monitoring space?

North America holds the largest

revenue share, commanding over 44.20% of the market in 2025, driven by high

diabetes prevalence rates, robust insurance reimbursement support for advanced

digital monitors, and an extensive network of specialized clinics.

Browse More Reports:

Anesthesia Monitoring Devices Market

About Us

Business Market Insights is a

market research platform that provides subscription service for industry and

company reports. Our research team has extensive professional expertise in

domains such as Electronics & Semiconductor; Aerospace & Defense;

Automotive & Transportation; Energy & Power; Healthcare; Manufacturing

& Construction; Food & Beverages; Chemicals & Materials; and

Technology, Media, & Telecommunications.

Contact Us

If you have any questions about

this report or would like further information, please contact us:

Contact person: Ankit Mathur

Email: sales@businessmarketinsights.com

Phone: +16467917070

Comments

Post a Comment