Data Center Construction Market Technology Trends and Forecast to US$ 469.8 Billion by 2033

Technological innovation is

reshaping the global Data Center Construction Industry, with operators

increasingly adopting sophisticated cooling technologies, resilient power

architectures, and modular facility designs to support growing computational

requirements. The rise of hyperscale data centers and edge computing

infrastructure continues to create substantial opportunities across the

construction ecosystem.

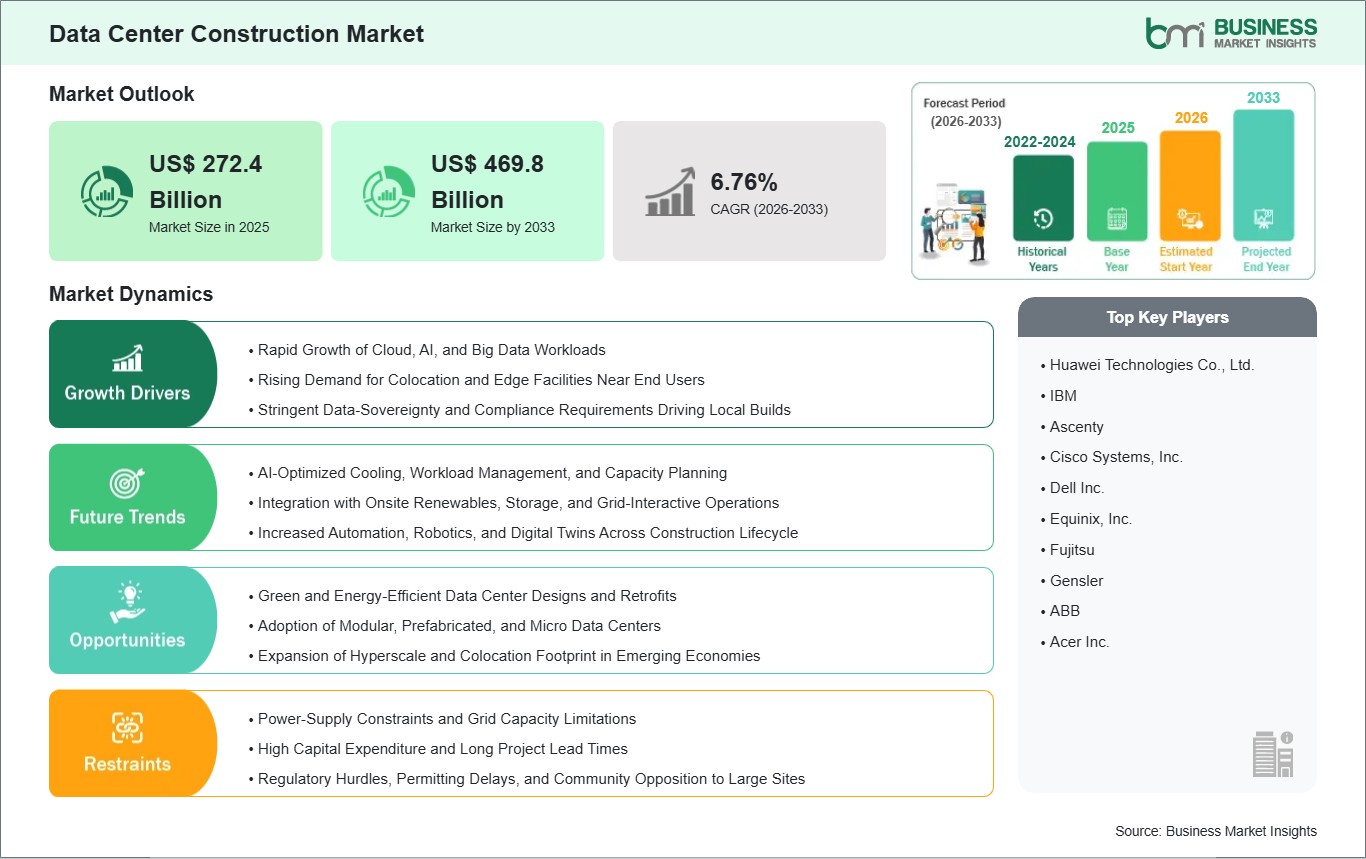

According to Business Market

Insights, the global Data

Center Construction Market was valued at US$ 272.4 billion in

2025 and is anticipated to reach US$ 469.8 billion by 2033. The market is

projected to grow at a CAGR of 7.05% during the forecast period from 2026 to

2033.

Advancements in prefabricated

modular construction techniques, liquid immersion cooling systems, dynamic

uninterruptible power supply (UPS) modules, and grid-wide sustainable energy

utilization are rapidly shifting the competitive environment. Leading engineering

and infrastructure firms are funneling substantial capital into consolidating

multi-phase builds into rapid-deployment architectures, introducing intelligent

real-time thermal monitoring, and embedding zero-trust physical security

perimeters directly into facility operations. These investments are

specifically engineered to eliminate high-voltage distribution bottlenecks,

reduce massive structural capital outlays, and provide a fault-tolerant,

scalable hosting matrix that seamlessly integrates with modern smart cities and

edge-computing applications.

What Is Data Center

Construction?

Data center construction refers to

the highly specialized process of designing, building, and commissioning the

structural shell and internal critical infrastructure required to house

thousands of networked computer servers securely. Far exceeding standard

commercial building standards, these modernized facilities operate as the

structural backbone of the internet. They incorporate sophisticated layers of

redundancy such as backup power generation lines and dedicated fiber-optic

vaults alongside advanced environmental controls that capture rising

thermal emissions at the source and instantly translate them into optimized

cooling flows to protect delicate silicon hardware.

These mission-critical physical

frameworks utilize highly distinct functional components to manage extreme

power densities. At the foundational level, heavy-duty electrical designs act

as the critical link between municipal power grids and internal server racks,

managing voltage step-downs and handling automated power-failover protocols

smoothly. Concurrently, complex mechanical designs manage intricate

liquid-to-chip or precision air conditioning loops, which process environmental

logic dynamically, allowing facility operators to manage acute heat

fluctuations and isolate structural failures within microseconds, guaranteeing

complete operational uptime (up to 99.995%) without data corruption.

Download Sample Report: https://www.businessmarketinsights.com/sample/BMIPUB00032683

Market Drivers

A primary driver accelerating the

global Data Center Construction Industry is the critical focus on Expanding

Hyperscale Architectures and Enhancing Cloud Capacity. Legacy enterprise data

rooms suffer from extreme spatial and power limitations, where localized

thermal overloads can trigger expansive network crashes. Modern data center

construction addresses this vulnerability by establishing continuous,

high-capacity mega-facilities across strategic geographical corridors. The

massive scale of these builds allows cloud service providers to perform

proactive load-balancing, centralize IT operations instantly, and dramatically

reduce system-wide latency, establishing an exceptionally stable foundation for

the digital economy.

The global push for High-Density

AI Workloads and Revolutionizing Thermal Efficiency represents another core

market driver. As enterprise digitization expands and heavy commercial end

users deploy highly automated machine learning models, the baseline requirements

for localized rack power densities have grown intensely strict. Modern data

centers utilize intelligent mechanical layouts to dynamically route chilled

water or dielectric fluids directly to server clusters based on changing

computational demand pools. This limits baseline power-usage effectiveness

(PUE) scores, eliminates systemic hardware overheating, and optimizes capital

returns for colocation operators running high-throughput environments.

Additionally, the universal

transition toward Green Data Centers and Digital Solutions for a Sustainable

Future acts as a powerful catalyst. To reach international carbon neutrality

goals, modern computing facilities must smoothly integrate massive volumes of

renewable energy inputs, such as utility-scale solar purchasing agreements and

direct wind-farm grid links. Advanced data center construction provides the

ultra-efficient physical baselines and adaptive resource configurations

necessary to handle extreme electrical consumption footprints, safely

insulating corporate operators from escalating fossil-fuel utility tariffs.

Market Segmentation

By Types of Construction

- Electrical

Design (Commanding a leading position within construction budgets due to

heavy outlays for specialized switchgears, transformers, and continuous

UPS battery arrays)

- Mechanical

Design (Expanding steadily as high-density server configurations mandate

expensive, specialized structural adaptations for direct-to-chip and

immersion cooling infrastructures)

- General

Construction (Encompassing the physical core and shell development, site

grading, security perimeter walls, and structural engineering compliance)

By Tier Standards

- Tier 3

(The dominant volume segment, preferred across colocation networks and

enterprise hubs due to its optimal balance of N+1 redundancy and

concurrent maintainability without prohibitive costs)

- Tier 4

(Tracking high growth as critical infrastructure authorities and major

financial institutions deploy maximum-fault-tolerant layouts that

guarantee 99.995% uptime)

- Tier 1

& Tier 2 (A smaller segment utilized for localized, non-critical

enterprise storage and standard administrative processing)

By Industry Verticals

- IT

& Telecommunication (The premier revenue-generating vertical,

capturing the dominant market share supported by massive hyperscale

expansions and 5G network rollout frameworks)

- BFSI

(Exhibiting an accelerating forward growth trajectory fueled by the

necessity for hyper-secure, low-latency trading infrastructure and

localized financial data compliance)

- Government

(Demanding highly secure, physically hardened data center setups to safely

manage classified public records and national digital identity networks)

- Healthcare

(Utilizing dedicated compliant facilities to protect heavy volumes of

sensitive patient data and complex genomic processing workloads)

- Others

(Expanding via manufacturing, retail, and media networks requiring

localized edge-computing data storage for streaming and logistics

tracking)

Regional Insights

- North

America holds the premier position in the global landscape,

securing a commanding revenue share valued at US$ 89.00 Billion in 2022.

This market dominance is anchored by massive technology giant

headquarters, strict regulatory mandates regarding data storage

infrastructure, and aggressive private-sector hyperscale investments

across the United States.

- Europe exhibits

a highly structured, substantial market presence, characterized by

aggressive public sustainability targets focused on minimizing carbon

footprints and achieving ultra-low PUE standards in hubs like Frankfurt,

London, Amsterdam, and Paris (FLAP). European implementations prioritize

stringent data sovereignty compliance and district heating integrations.

- Asia-Pacific represents

the fastest-growing geographic block, recording an exceptional forward

CAGR of 10.4% during the forecast window. This rapid expansion is

propelled by massive digital adoption rates, accelerating urbanization,

and enormous capital outlays directed toward colocation hubs in China,

India, and Japan to reduce latency for booming internet user bases.

- Rest

of the World (Middle East, Africa, South & Central America) is

displaying steady, progressive growth patterns, driven by targeted cloud

service expansions in the Gulf region to power newly developed smart

cities, international submarine cable landings boosting African digital

hubs, and enterprise digital migrations in Brazil and Chile.

Top Players in the Industry

The competitive ecosystem displays

a sophisticated matrix of diversified heavy-industrial engineering

conglomerates and specialized general contracting firms executing massive

multi-phase supply agreements with multinational cloud networks.

- AECOM

- DPR

Construction Inc.

- Eaton

Corporation PLC

- Holder

Construction Company

- Mercury

Engineering Ltd.

- Nikom

InfraSolutions Pvt. Ltd.

- Rittal

GmbH & Co KG

- Schneider

Electric SE

- STO

Building Group Inc.

- Turner

Construction Co.

Technological Innovations

The commercial implementation of

Prefabricated Modular Data Centers (PMDCs) represents a monumental structural

breakthrough for the construction sector. Historically, capacity upgrades

required the installation of traditional "stick-built" structural

expansions that took years to acquire, permit, and construct, which raised

system integration complexity. Next-generation modular designs consolidate the

functionalities of power, cooling, and server racks into fully integrated,

factory-tested structural blocks. This substantial simplification reduces

on-site construction footprints, limits weather-related delays, and

significantly compresses installation timelines for tech companies executing

rapid capacity expansions.

Concurrently, the integration of

Liquid Cooling Architectures is completely modernizing the mechanical

engineering landscape. Modern high-performance compute (HPC) nodes face

persistent thermal throttling threats under traditional air cooling protocols. To

address this limitation, leading developers are embedding advanced liquid

immersion tanks and direct-to-chip microchannel plates directly into

station-level server designs. These integrated thermal systems continually

assess localized heat traffic patterns to extract and reject massive BTU loads

in real time, guaranteeing robust hardware lifespans without compromising the

electrical power limitations of the facility.

Future Market Outlook

The long-term trajectory for the

Data Center Construction Market remains exceptionally robust. As international

data regulatory frameworks permanently establish local storage mandates and

global AI initiatives expand the baseline volume of high-density processing

assets requiring specialized physical housing, the universal demand for

intelligent construction platforms will scale continuously, defining

point-of-care digital infrastructure protocols.

Future research and development

capital will be heavily directed toward the commercialization of fully

decarbonized eco-efficient facility solutions that utilize advanced nuclear

small modular reactors (SMRs) to completely phase out grid reliance, the implementation

of autonomous robotic construction systems connected directly to 3D

architectural modeling diagnostics, and the expansion of smart construction

supply chains. General contractors and technology developers that successfully

balance premium structural execution with highly competitive, modular green

designs will comfortably secure long-term global market leadership.

Frequently Asked Questions

(FAQs)

What is the projected valuation

of the global data center construction market by 2030?

The global data center

construction market is projected to reach a valuation of US$ 440.30 Billion by

2030, expanding significantly from its established baseline value of

approximately US$ 230.50 Billion in 2022.

What is the expected compound

annual growth rate (CAGR) of the market over the forecast window?

The market is anticipated to

expand at a steady Compound Annual Growth Rate (CAGR) of 8.4% globally during

the forecast timeline spanning from 2023 through 2030.

Which end-user industry segment

commands the dominant revenue share in the global market?

The IT & Telecommunication

segment holds the leading market share because major cloud service providers

and telecommunications networks command massive capital budgets required to

execute comprehensive hyperscale facility developments.

How does the tier standard

system dictate data center construction?

Tier standards dictate the

structural redundancy and concurrent maintainability of the facility. A Tier 3

data center (the most common) requires dual power and cooling paths to ensure

equipment can be maintained without taking the servers offline, fundamentally

altering the electrical and mechanical blueprints of the building.

Browse More Reports:

Asset Management System Market

Air Insulated Automated Material Handling Equipment Market

Arc-based Plasma Lighting Market

About Us

Business Market Insights is a

market research platform that provides subscription service for industry and

company reports. Our research team has extensive professional expertise in

domains such as Electronics & Semiconductor; Aerospace & Defense;

Automotive & Transportation; Energy & Power; Healthcare; Manufacturing

& Construction; Food & Beverages; Chemicals & Materials; and

Technology, Media, & Telecommunications.

Contact Us

If you have any questions about

this report or would like further information, please contact us:

Contact person: Ankit Mathur

Email: sales@businessmarketinsights.com

Phone: +16467917070

Comments

Post a Comment