Drilling Fluids Market Projected to Achieve US$ 14.1 Billion by 2033

The global Drilling Fluids Industry is undergoing accelerated evolution, supported by increasing exploration activities in deepwater regions, rising energy demand, and growing requirements for effective drilling performance in complex geological formations. Manufacturers are focusing on developing advanced fluid systems that enhance well control, lubrication, and environmental compliance.

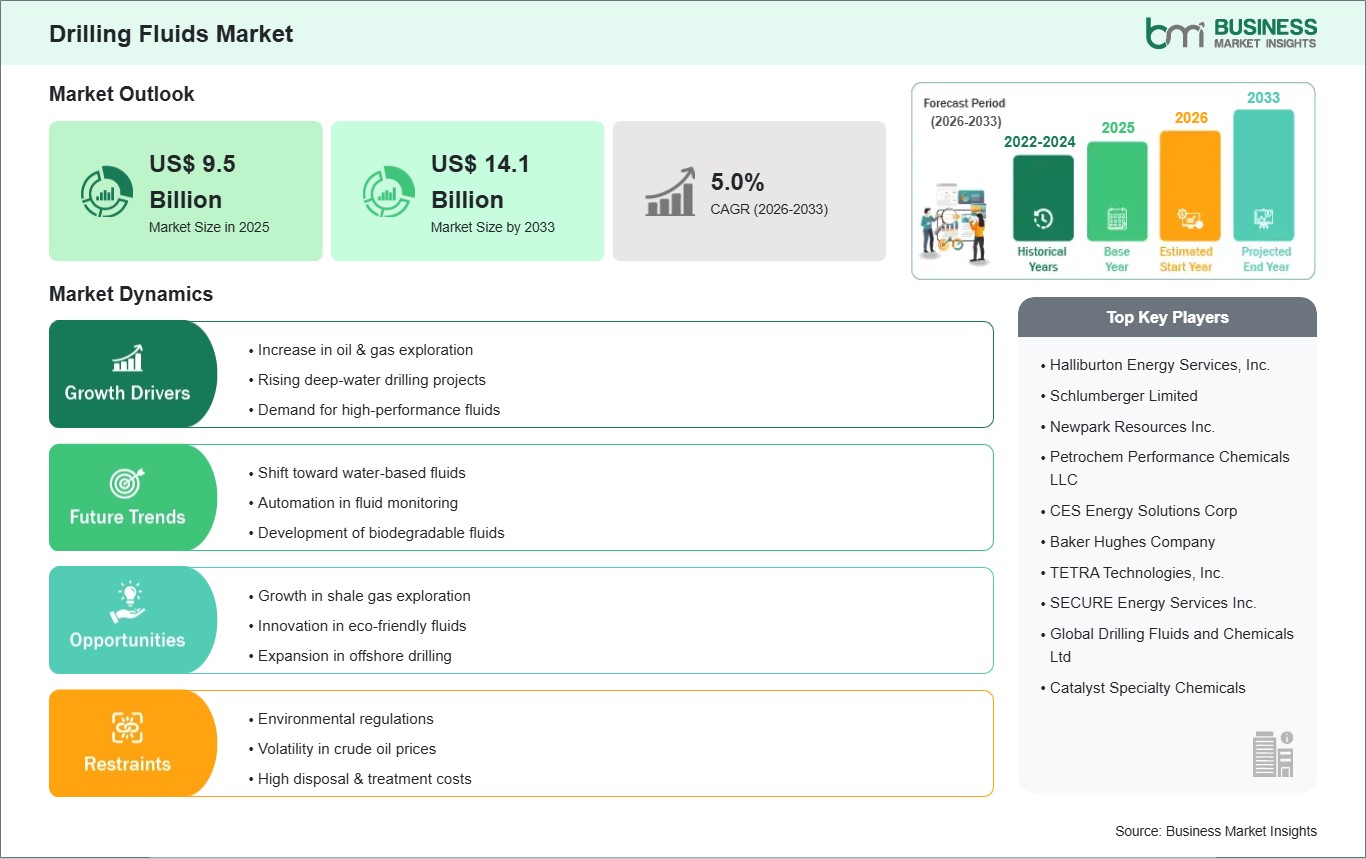

As per Business Market Insights, the global Drilling

Fluids Market is expected to increase from US$ 9.5 billion in 2025

to US$ 14.1 billion by 2033. This growth reflects a projected CAGR of 5.06%

throughout the forecast period of 2026–2033.

Advancements in additive chemistry, biodegradable base-oil

synthesis, and smart, real-time mud telemetry systems are rapidly reconfiguring

the competitive market landscape. Leading oilfield service providers and

international chemical developers are channeling substantial R&D capital

into expanding the operational windows of eco-friendly water-based and

synthetic-based systems. These strategic engineering efforts aim to achieve

optimal shale inhibition and robust wellbore integrity while successfully

complying with increasingly strict international environmental discharge

restrictions.

What Is a Drilling Fluid?

A drilling fluid is a highly engineered, multi-component

chemical and physical mixture circulated through a wellbore during oil, natural

gas, geothermal, or mining drilling procedures. Entering the well via the

interior hollow drill string and exiting back up the annular space between the

pipe and the formation wall, these fluids must possess highly specific, dynamic

rheological properties. Their primary composition typically relies on a

distinct continuous base liquid such as fresh water, saturated brine, diesel,

mineral oil, or synthetic linear alpha-olefins densely packed with

functional chemical additives including weighting agents like barite, polymers

for fluid-loss control, viscosifiers like bentonite clay, and localized

corrosion inhibitors.

The fundamental physical objective of a drilling fluid is to

balance external hydrostatic pressure against internal formation pressures to

prevent catastrophic well control incidents or blowouts. Simultaneously, the

fluid acts as a hydraulic conveyor, dynamically encapsulating heavy rock

cuttings and transporting them to surface solids-control equipment where the

mixture is filtered and recycled. By coating permeable formation zones with a

thin, impermeable filter cake, advanced drilling muds eliminate structural

wellbore collapse, lower mechanical torque and drag on steerable bottom-hole

assemblies, and protect sensitive hydrocarbon production zones from structural

fluid invasion.

Download Sample Report: https://www.businessmarketinsights.com/sample/BMIPUB00032584

Market Drivers

A primary driver accelerating the global Drilling Fluids

Industry is the Accelerating Development of Unconventional Shale and Tight Oil

Reservoirs. The continuous refinement of horizontal drilling and multi-stage

hydraulic fracturing, particularly across complex onshore basins, has vastly

expanded the total length of individual lateral wellbore segments. Because

navigating these extensive horizontal horizons exposes the equipment to

prolonged contact with highly reactive, water-sensitive shale layers, operators

require specialized, high-performance drilling fluids to prevent clay swelling,

manage hole enlargement, and dramatically reduce expensive non-productive time

(NPT) caused by stuck pipes.

The intensifying institutional shift toward Deepwater and

Ultra-Deepwater Offshore Exploration serves as another vital market driver. As

mature onshore fields experience natural depletion cycles, state-owned and

international energy corporations are expanding operations into complex

offshore blocks, such as those in the Gulf of Mexico, the North Sea, and the

pre-salt basins of Latin America. These maritime operations present severe

logistical and operational challenges, including subsea mud-line temperatures

nearing freezing alongside extremely high downhole pressures. These conditions

require the bulk deployment of synthetic-based fluid systems capable of

maintaining stable viscosity profiles and preventing gas hydrate formation

under extreme thermal stresses.

Market Segmentation

By Product Type

- Water-Based

Fluids (WBFs) (Including dispersed, non-dispersed, and advanced

high-performance water-based muds)

- Oil-Based

Fluids (OBFs) (Formulated with high-stability diesel or low-toxicity

mineral oil bases for premium lubrication)

- Synthetic-Based

Fluids (SBFs) (Utilizing biodegradable synthetic esters, ethers, and

polyalphaolefins for extreme offshore conditions)

- Synthetic

and Non-Aqueous Gas Systems (Including air, mist, and stable foam drilling

applications)

By Application

- Onshore

Drilling (Sustained by massive unconventional asset developments and

pad-drilling efficiency updates)

- Offshore

Drilling (Comprising shallow water, deepwater, and ultra-deepwater

exploration architectures)

By End-Use Industry

- Oil

& Gas Extraction (The foundational global consumption vertical for

both exploratory and production wells)

- Geothermal

Energy Drilling (Requiring ultra-high temperature fluid stabilities to tap

deep thermal reservoirs)

- Mining

& Mineral Exploration

- Infrastructure

& Trenchless Civil Construction

The Water-Based Fluids (WBFs) segment commanded the dominant

revenue and volume share of the global market matrix in 2025, accounting for

over 52% of global volume. This leading position is supported by its universal

cost-efficiency, ease of environmental handling, and widespread utilization

across standard top-hole onshore drilling intervals globally. Concurrently, the

Onshore Drilling application segment led the overall end-use footprint, while

the Offshore Synthetic-Based Fluids vertical is registering the fastest

projected compound growth rate due to escalating technical demands in complex

deepwater projects.

Regional Insights

- North

America commands the premier share of the global drilling fluids

market, driven by mature unconventional shale operations across the United

States and Canada. High rig density across the Permian, Delaware, and

Bakken basins, combined with intensive horizontal drilling and robust

regulatory compliance infrastructure, maintains a massive, non-cyclical

volume demand for advanced high-performance water-based and low-toxicity

oil-based fluids.

- Asia-Pacific represents

the fastest-growing regional market over the forecast timeline, capturing

a significant chunk of global volume expansion. Growth is heavily

accelerated by state-backed energy modernization programs, massive

infrastructure drilling projects in China and India, and rising

investments to commercialize deep shale gas reserves and coalbed methane

blocks to satisfy soaring local industrial energy demands.

- Europe maintains

a stable, premium market presence focused primarily on advanced offshore

applications across the North Sea corridor. Regional market dynamics are

closely governed by highly rigorous environmental protocols, such as the

OSPAR Convention, which heavily restricts chemical discharges and

continuously drives the local development of ultra-clean, highly

biodegradable synthetic fluids.

- Rest

of the World (Middle East & Africa and South America) is

demonstrating robust incremental growth patterns. Massive offshore

pre-salt expansions in Brazil, paired with major national oil company

expansions across the Persian Gulf and East Africa, are attracting heavy

capital investments to construct advanced regional fluid blending centers

and solid-control support infrastructure.

Top Players in the Industry

The competitive marketplace features a highly consolidated

ecosystem of multi-national oilfield service giants alongside specialized

chemical developers who utilize advanced chemical patents and integrated

rig-site solids control systems to secure long-term operator contracts.

- SLB

(Schlumberger Limited)

- Halliburton

Company

- Baker

Hughes Company

- Weatherford

International plc

- Newpark

Resources, Inc.

- Imerys

S.A.

- Tetra

Technologies, Inc.

- SECURE

Energy Services Inc.

- National

Oilwell Varco (NOV Inc.)

Technological Innovations

The industrial integration of Nanoparticle-Enhanced Fluid

Additives represents a massive technological milestone for modern drilling

fluid engineering. Conventional micro-sized additives frequently struggle to

seal the microscopic pore throats found in tight shale formations, allowing

fluid filtrate to migrate into the rock and cause structural destabilization or

wellbore collapse. By incorporating engineered nanoparticles such as

nano-silica, graphene oxide, or carbon nanotubes into the mud matrix,

material scientists can create a highly optimized physical barrier. These

ultra-fine particles seamlessly plug micro-fractures, drastically reduce fluid

loss, lower overall filter cake thickness, and provide exceptional thermal and

shear stability under extreme downhole environments.

Concurrently, the deployment of Automated Smart Rheology

Control and Real-Time Fluid Monitoring Systems is radically modernizing

rig-site efficiency. Historically, mud properties like density, viscosity, and

gel strength were measured manually by mud engineers at scheduled intervals,

creating lag times in identifying downhole fluid degradation. Next-generation

automated mud logging trailers utilize inline sensors and advanced ultrasonic

analytics to continuously track chemical variations in real time. This streaming

data feeds directly into machine-learning algorithms that instantly calculate

fluid hydraulics, automatically alerting operators or triggering digital dosing

pumps to adjust chemical concentrations, thereby preventing non-productive time

caused by wellbore breathing or sudden influxes.

Future Market Outlook

The future trajectory for the Drilling Fluids Market remains

highly resilient and positive. As global energy demands require exploration

teams to drill deeper, hotter, and more structurally tortuous well paths, the

global utilization of highly customized, high-performance fluid architectures

will steadily scale, transforming traditional reservoir extraction boundaries.

Future research and development capital will be heavily

directed toward the commercialization of fully circular, closed-loop mud

recycling systems to maximize chemical recovery and minimize environmental

footprint, the synthesis of bio-derived, zero-carbon base oils from renewable

agricultural side-streams, and the expansion of digital telestroke-style remote

mud monitoring frameworks. Strategic organizations that successfully optimize

fluid performance metrics while delivering verifiable low-toxicity and low-carbon

profiles will comfortably command long-term global market leadership.

Frequently Asked Questions (FAQs)

What product type currently dominates the global drilling

fluids market?

The Water-Based Fluids (WBFs) segment holds the absolute

largest market share, capturing over 52% of the market in 2025. This dominance

is driven by its universal cost-effectiveness, environmental compliance

advantages, and widespread application across standard onshore top-hole

intervals globally.

Why is the offshore synthetic-based fluids vertical

expanding so rapidly?

Synthetic-Based Fluids (SBFs) combine the high lubrication,

thermal stability, and shale-inhibition performance of traditional oil-based

muds with the superior biodegradability and low toxicity required for offshore

marine discharge compliance, making them essential for complex deepwater wells.

How do drilling fluids help prevent catastrophic wellbore

blowouts?

Drilling fluids utilize heavy weighting agents, such as

barite, to dynamically adjust the fluid's density. This allows the fluid column

to exert a precise outward hydrostatic pressure that counteracts and controls

internal high-pressure gas or oil zones within the formation.

Which geographic region leads the consumption of drilling

fluids?

North America commands the leading global market share,

supported by dense, high-volume horizontal drilling activities, unconventional

shale plays like the Permian Basin, and advanced subsea exploration projects

within the Gulf of Mexico.

Browse More Reports:

Ceramic Matrix Composites Market

About Us

Business Market Insights is a market research platform that

provides subscription service for industry and company reports. Our research

team has extensive professional expertise in domains such as Electronics &

Semiconductor; Aerospace & Defense; Automotive & Transportation; Energy

& Power; Healthcare; Manufacturing & Construction; Food &

Beverages; Chemicals & Materials; and Technology, Media, &

Telecommunications.

Contact Us

If you have any questions about this report or would like

further information, please contact us:

Contact person: Ankit Mathur

Email: sales@businessmarketinsights.com

Phone: +16467917070

Comments

Post a Comment