Global Antimicrobial Drugs Market Analysis with US$ 178.96 Billion Forecast by 2033

Scientific advancements and

evolving healthcare needs are reshaping the global Anti-Infective Agents

Industry. Rising incidences of bacterial, viral, fungal, and parasitic

infections, combined with increasing concerns surrounding drug-resistant

pathogens, are reinforcing the importance of innovative anti-infective

therapies in modern medical practice.

According to Business Market

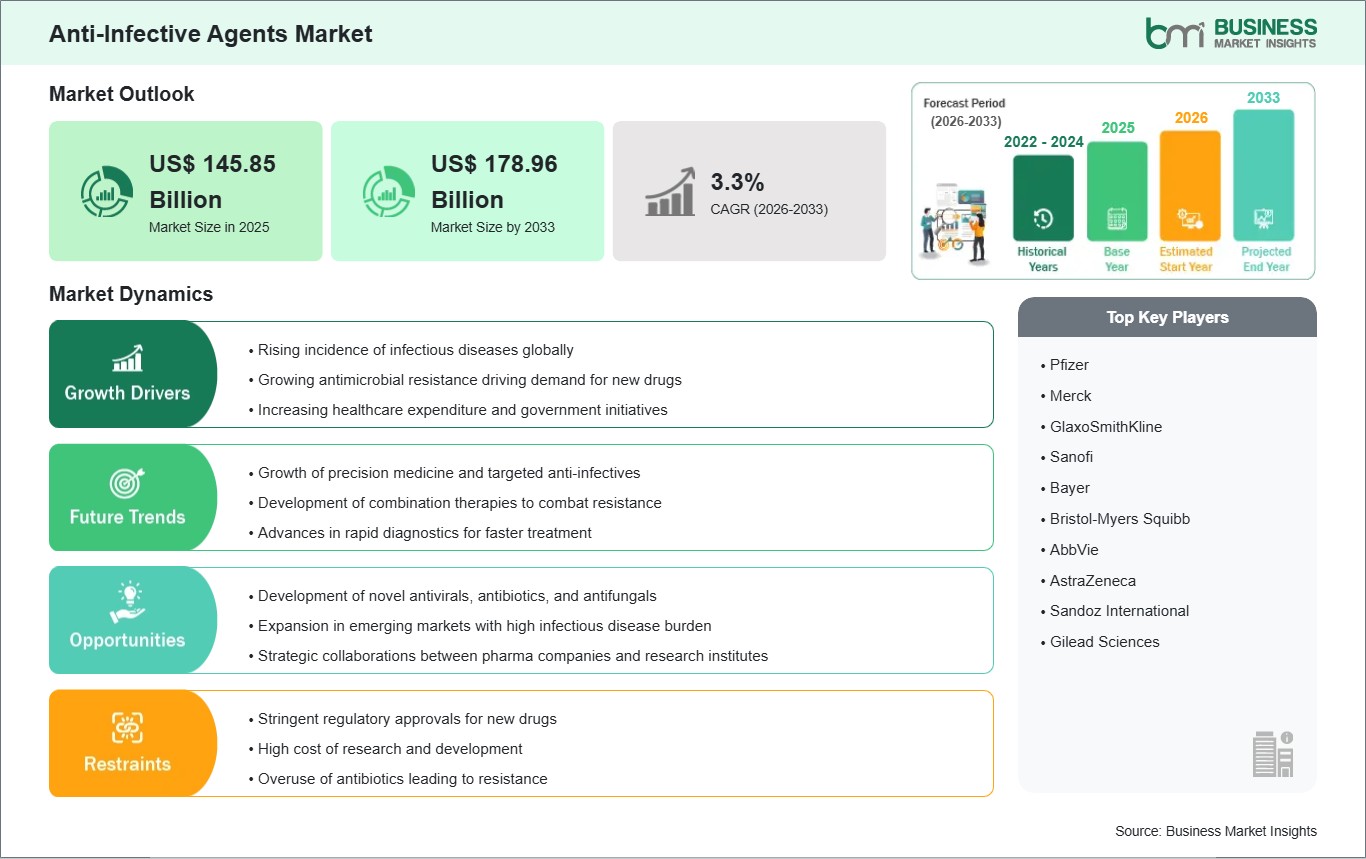

Insights, the global Anti-Infective

Agents Market was valued at US$ 145.85 billion in 2025 and is

anticipated to reach US$ 178.96 billion by 2033. The market is projected to

grow at a CAGR of 2.59% during the forecast period from 2026 to 2033.

Advancements in artificial

intelligence-driven drug discovery, novel combination therapies, specialized

targeted delivery systems, and fast-tracked regulatory pathways are

significantly reshaping the global competitive landscape. Prominent

pharmaceutical conglomerates and biotechnology firms are aggressively focusing

R&D pipelines on addressing multi-drug resistant (MDR) and pan-drug

resistant (PDR) pathogens, which pose an existential threat to standard medical

procedures. These strategic investments are closely aligned with comprehensive

international antimicrobial stewardship programs designed to balance rapid

clinical deployment with the preservation of therapeutic efficacy across acute

care, institutional, and long-term community environments.

What Are Anti-Infective Agents?

Anti-infective agents are

specialized chemical substances or pharmacological compounds designed to

systematically inhibit the replication, disrupt the metabolic pathways, or

eliminate the cellular structure of pathogenic micro-organisms within a host

organism. Operating as indispensable therapeutic countermeasures, these agents

are engineered to exhibit selective toxicity minimizing host cellular

damage while maximizing the destruction of invading pathogens. This extensive

therapeutic umbrella is deeply integrated into every tier of clinical

intervention, functioning prophylactically to prevent perioperative infections

and curatively to resolve localized or systemic bloodstream infections.

The anti-infective landscape is

classified based on the target pathogen and corresponding mechanism of action.

Antibacterials (antibiotics) target bacterial structures, such as disrupting

cell wall synthesis via beta-lactams or inhibiting protein translation through

ribosomal binding. Antivirals interfere with viral replication cycles,

utilizing protease inhibitors or nucleoside analogues to arrest viral loads in

chronic conditions like HIV, hepatitis, and acute respiratory outbreaks.

Antifungals systematically degrade fungal cell membranes containing ergosterol,

while antiparasitics neutralize complex protozoal and helminthic vectors,

altogether forming a multi-tiered therapeutic shield across global clinical

pipelines.

Download Sample Report: https://www.businessmarketinsights.com/sample/BMIPUB00032647

Market Drivers

A primary driver accelerating the

global Anti-Infective Agents Industry is the Escalating Global Threat of

Antimicrobial Resistance (AMR) and Multi-Drug Resistant Strains. The historical

over-prescription and empirical misuse of broad-spectrum antibiotics have

accelerated natural bacterial mutation rates, culminating in the rise of highly

resilient pathogens like MRSA, VRE, and carbapenem-resistant

Enterobacteriaceae. Because these "superbugs" render standard

first-line therapies obsolete, international healthcare networks are forced to

procure advanced, high-margin reserve antibiotics and novel combination

therapies, driving substantial revenue expansion within the specialized

institutional segment.

The rapid expansion of the Global

Immunocompromised Patient Population and Advanced Surgical Procedures

represents another core market driver. The worldwide surge in multi-organ

transplantations, aggressive oncology chemotherapy regimens, and advanced autoimmune

therapies has created a vast patient demographic possessing severely depressed

immune systems. These individuals are exceptionally vulnerable to opportunistic

healthcare-associated infections (HAIs) and lethal systemic fungal conditions.

Consequently, institutional clinical networks are systematically expanding

their mandatory prophylactic anti-infective protocols, guaranteeing persistent,

high-volume demand for premium therapeutic lines across hospital groups

globally.

Furthermore, an increasing volume

of Public-Private R&D Funding Initiatives and Fast-Track Regulatory

Incentives is acting as a powerful growth catalyst. Legislative

frameworks such as the Generating Antibiotic Incentives Now (GAIN) Act and

Qualified Infectious Disease Product (QIDP) designations offer

pharmaceutical developers extended market exclusivity, streamlined clinical

trial phases, and prioritized regulatory review cycles. This favorable

financial and regulatory environment has effectively revitalized the

historically stagnant anti-infective research sector, incentivizing major

biotechnology firms to resume active discovery pipelines and launch

sophisticated molecular entities into the global market.

Market Segmentation

By Drug Type

- Antibaсterials

(Antibiotics) (Commands the leading volume share due to universal

application in routine clinical infections, though facing intense generic

pricing pressures)

- Antivirals

(The highest revenue-generating segment, propelled by long-term management

therapies for chronic viral diseases and post-pandemic safety stockpiling)

- Antifungals

(Tracking high compound growth driven by a rising incidence of invasive

candidiasis and aspergillosis among critical care patients)

- Antiparasitics

(Maintaining steady, localized volume patterns across tropical and

subtropical regions experiencing shifting vector distributions)

By Route of Administration

- Intravenous

(IV) (The dominant segment in acute care settings, critical for achieving

immediate, maximum systemic bioavailability in severe septic or

hospitalized states)

- Oral

(Widely preferred for outpatient care, chronic disease management, and

standard step-down therapeutic transitions)

- Topical

and Other Routes (Utilized for localized dermatological, ophthalmic, and

respiratory anti-infective delivery applications)

By Application

- Hospital-Acquired

Infections (HAIs) (A massive therapeutic vertical focus, addressing

central line infections, ventilator-associated pneumonia, and surgical

site contamination)

- Community-Acquired

Infections (Sustaining highly stable, non-cyclical baseline volumes across

standard respiratory, urinary, and gastrointestinal tracts)

- Other

Applications (Including preventative pediatric prophylactic regimens and

long-term travel medicine interventions)

By End-User

- Hospitals

and Clinics (The dominant procurement and administration channel, managing

high-concentration distribution networks and reserve-class formulary

lists)

- Ambulatory

Care Centers and Pharmacies (Experiencing rapid expansion due to the

steady transition toward outpatient clinics and localized long-term care

management)

The Antivirals segment held the

largest revenue share of the market matrix in 2025, driven by the premium

pricing structures associated with long-term viral suppression regimens and

high-demand prophylactic therapies. Simultaneously, the Intravenous (IV)

segment led the administration matrix due to the clinical necessity of direct

vascular access in severe, acute institutional infections, while the Hospital

End-User sector continues to command the largest overall purchasing power

globally.

Regional Insights

- North

America holds the premier revenue share of the global

anti-infective agents market, controlling a significant portion of the

total geographic matrix. This leadership is sustained by high per-capita

healthcare expenditure, a mature framework of antimicrobial stewardship

programs, and substantial federal funding for biodefense and pandemic

readiness. The immediate clinical adoption of high-cost, newly approved

molecular entities solidifies the region as the primary hub for premium

value generation.

- Europe maintains

a highly regulated, substantial market presence, characterized by strict

centralized oversight via the European Medicines Agency (EMA) and an

intensive institutional focus on limiting broad-spectrum antibiotic

overuse. Regional expansion across Germany, France, and the UK centers

tightly on value-based procurement contracts, standardized clinical

guidelines, and publicly funded cross-border research alliances aimed at

combating multi-drug resistance.

- Asia-Pacific represents

the fastest-growing geographic block, recording an exceptional forward

trajectory during the forecast period. Driven by rapid healthcare

modernizations, expanding public health insurance schemes, a high baseline

density of infectious diseases, and expanding pharmaceutical production

capabilities across China and India, this region is generating immense

volume requirements. Multinational firms are actively forming local

distribution ventures to capitalize on the rapid expansion of medical

infrastructure.

- Rest

of the World (Middle East & Africa and South America) is

demonstrating steady, progressive expansion patterns. Growth across South

America is anchored by expanding public health infrastructure in Brazil,

while the Middle East is recording an uptick in premium critical care

facilities, driven by a regional focus on self-reliance in pharmaceutical

manufacturing and advanced clinical infection control.

Top Players in the

Anti-Infective Agents Industry

The industrial landscape features

high corporate consolidation among top-tier global pharmaceutical

conglomerates, balanced by a highly specialized network of clinical-stage

biotechnology firms managing targeted molecular pipelines.

- Pfizer

Inc.

- Merck

& Co., Inc.

- GlaxoSmithKline

plc

- F.

Hoffmann-La Roche Ltd

- Novartis

AG

- Sanofi

- Gilead

Sciences, Inc.

- AstraZeneca

plc

- Shionogi

& Co., Ltd.

- Viatris

Inc.

Technological and Clinical

Innovations

The implementation of Artificial

Intelligence (AI) and Machine Learning Algorithms in Novel Molecular Screening

represents a monumental technological breakthrough for the anti-infective

sector. Historically, traditional phenotypic and genomic screening methods

required years of laboratory experimentation, frequently resulting in high

attrition rates and exorbitant development costs. Modern drug discovery

platforms leverage advanced deep-learning models to screen billions of

synthetic and natural chemical structures in silico within days. These systems

precisely predict a compound's ability to disrupt structural pathogen targets

while ensuring minimal mammalian cell toxicity, effectively shortening the

pre-clinical development phase and introducing entirely unique chemical classes

to combat resistant pathogens.

Concurrently, the clinical

development of Advanced Combination Therapeutics and Monoclonal Antibody

Pairings has fundamentally revolutionized the management of complex infections.

To circumvent rapid resistance development, modern therapeutic designs combine

established anti-infective backbones with innovative beta-lactamase inhibitors

or adjunctive targeted monoclonal antibodies. This dual-action approach

neutralizes the pathogen's primary enzymatic defense mechanisms simultaneously,

restoring full clinical efficacy to standard therapies and providing highly

specialized, targeted defense vectors that successfully clear severe systemic

infections without inducing widespread microbial mutations.

Future Market Outlook

The future trajectory for the

Anti-Infective Agents Market remains exceptionally robust. As global health

models permanently prioritize defensive readiness against emerging biological

strains and clinical networks continue to demand highly specific, resistance-resistant

therapeutic choices, the global volume consumption of advanced antivirals,

antifungals, and reserve-class antibacterials will scale continuously,

establishing the benchmarks of modern disease control.

Future research and development

capital will be heavily directed toward the commercialization of fully

personalized anti-infective therapies guided by rapid companion diagnostics,

the deployment of peptide-based membrane disruptors that physically eradicate

bacterial cells, and the expansion of smart, time-released oral formulations

designed to maintain precise therapeutic windows in outpatient environments.

Organizations that successfully align their development pipelines with rapid

point-of-care susceptibility testing will comfortably secure long-term global

market leadership.

Frequently Asked Questions

(FAQs)

What primary factor is driving

the rapid revenue expansion within the anti-infective agents market?

The primary driver is the alarming

rise of antimicrobial resistance (AMR) and multi-drug resistant superbugs

globally. This critical shift forces healthcare institutions to transition away

from low-cost generic antibiotics and procure advanced, higher-margin

reserve-class therapies to resolve life-threatening clinical infections.

Why does the Antivirals segment

command the largest revenue share in the market matrix?

The Antivirals segment leads the

market in value due to the premium pricing structures and long-term,

non-cyclical consumption patterns associated with chronic viral suppression

regimens (such as HIV and Hepatitis B/C management) alongside continuous institutional

pandemic stockpiling initiatives.

How do public-private

legislative incentives like the GAIN Act impact drug development?

Incentives like the GAIN Act

provide critical advantages to pharmaceutical firms, including extended market

exclusivity and fast-tracked regulatory reviews for newly discovered infectious

disease products. This significantly enhances the financial viability of

anti-infective R&D pipelines.

Which geographic territory is

recording the fastest compound growth rate for anti-infective solutions?

The Asia-Pacific region is

tracking the fastest projected compound annual growth rate (CAGR), propelled by

massive hospital infrastructure expansions, rising disposable income, expanding

public insurance coverage, and a high regional patient density requiring

efficient infection control.

Browse More Reports:

About Us

Business Market Insights is a

market research platform that provides subscription service for industry and

company reports. Our research team has extensive professional expertise in

domains such as Electronics & Semiconductor; Aerospace & Defense;

Automotive & Transportation; Energy & Power; Healthcare; Manufacturing

& Construction; Food & Beverages; Chemicals & Materials; and

Technology, Media, & Telecommunications.

Contact Us

If you have any questions about

this report or would like further information, please contact us:

Contact person: Ankit Mathur

Email: sales@businessmarketinsights.com

Phone: +16467917070

Comments

Post a Comment