Global Automotive Polymer Materials Market Analysis with US$ 77.1 Billion Forecast by 2033

The Automotive Elastomers Industry is experiencing steady growth worldwide, driven by the escalating adoption of lightweight, high-performance materials across diverse vehicle production lines, a rising global focus on improving fuel efficiency and reducing greenhouse gas emissions, and the pressing need to enhance structural durability and noise, vibration, and harshness (NVH) damping precision in next-generation automotive platforms.

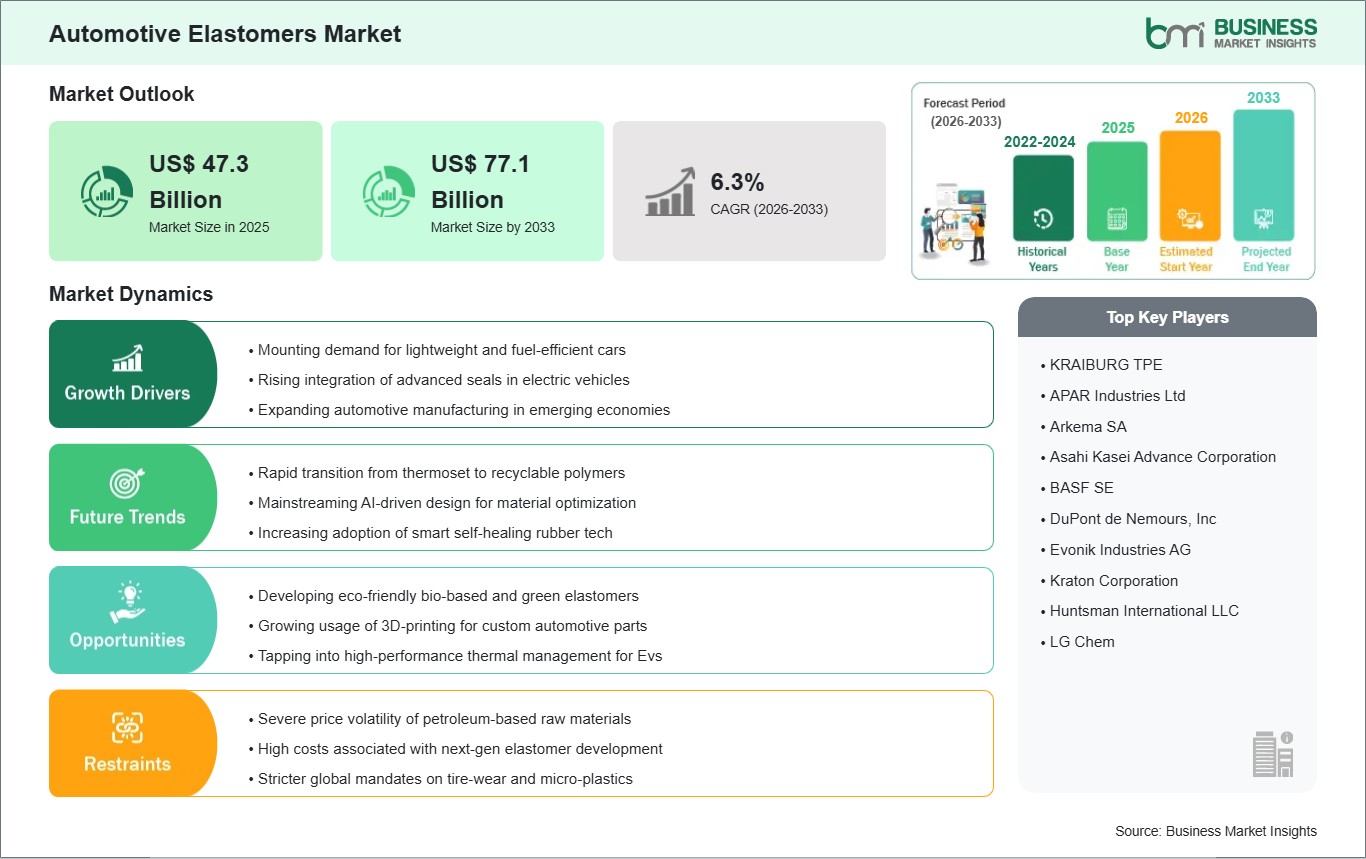

According to Business Market Insights, the global Automotive

Elastomers Market size is expected to reach US$ 77.1 Billion by 2033

from US$ 47.3 Billion in 2025. The market is estimated to record a CAGR of

6.30% from 2026 to 2033.

Advancements in specialized polymer compounding, the

integration of bio-based circular material grades, and innovative injection

molding technologies, along with the rising deployment of high-resilience

sealing systems in electric vehicles (EVs) and hybrid power systems, are

significantly transforming the market landscape. Automotive OEMs are

increasingly prioritizing high-temperature resistance, ozone and weathering

protection, and lightweight processing characteristics to meet shifting

regulatory preferences for eco-conscious vehicle manufacturing and minimized

volatile organic compound (VOC) interior emissions.

What Are Automotive Elastomers?

Automotive elastomers encompass a comprehensive range of

highly flexible, high-durability, synthetic and natural macromolecular polymers

engineered with low intermolecular strength and high elastic deformation

capabilities, tailored for heavy-duty vehicular sealing, structural damping,

and fluid-handling applications. Their primary objective is to execute highly

continuous, reliable, and leak-proof isolation of automotive components under

intense mechanical stresses, fluid exposure, and severe temperature fluctuations

without suffering premature material failure.

Because modern automotive engineering demands continuous

weight reduction and zero-defect assembly optimization, automotive elastomers

are extensively deployed across passenger cars, utility trucks, and electric

mobility architectures. Legacy automotive setups relied heavily on rigid, heavy

metal links and traditional thick vulcanized rubbers that suffered from rapid

environmental aging. In contrast, advanced automotive elastomer configurations

integrate sophisticated thermoplastic polyolefins (TPO), advanced

fluoroelastomers (FKM), and intelligent molecular cross-linking techniques

designed to handle delicate fuel lines, EV battery pack enclosures, and complex

dynamic under-hood environments.

Download Sample Report: https://www.businessmarketinsights.com/sample/BMIPUB00032430

Market Drivers

A primary driver for the Automotive Elastomers Industry is

the rapid structural evolution and digital transformation of the global

transport sector, particularly in the production of electric vehicles (EVs) and

high-efficiency hybrid drivetrains. These high-tech automotive fields require

ultra-lightweight components and specialized thermal management gaskets that

traditional heavy materials cannot consistently achieve.

The rising focus on passenger comfort and widening raw

material supply chain constraints across major Tier-1 manufacturing divisions

also act as a vital growth factor. Implementing advanced thermoplastic

elastomers (TPE) allows components to be completely reprocessed and recycled,

helping automotive manufacturers maintain high production output while

shielding their operational overhead from global synthetic monomer cost

volatility.

Furthermore, stringent environmental protection regulations

and corporate sustainability initiatives aimed at lowering fleet-wide exhaust

emissions significantly contribute to market demand. The growing transition

toward deploying specialized compounds for eco-conscious interiors such as

low-VOC door seals, non-toxic acoustic insulators, and dashboard soft-touch

panels is heavily driving market volume.

Additionally, the increasing physical accessibility of

optimized injection-molding systems and standardized plug-and-play material

matrices is prompting localized automotive parts molders to adopt innovation,

removing the historical barrier of high upfront tooling capital investments and

further propelling sustained market growth.

Market Segmentation

By Type

- Thermoset

Elastomers (Natural Rubber, EPDM, SBR, Nitrile Rubber)

- Thermoplastic

Elastomers (TPE, TPO, TPV, TPU)

By Application

- Tires

- Interior

Components

- Exterior

Components

- Under-the-Hood

& Powertrain Parts

- EV-Specific

Sealing & Thermal-Management

By Vehicle Type

- Passenger

Vehicles

- Light

Commercial Vehicles (LCVs)

- Heavy

Commercial Vehicles (HCVs)

The thermoset elastomers segment dominates the market due to

its high material stability, extensive historical integration in tire

manufacturing, and established track record of handling harsh under-hood

temperatures and high mechanical loads. The thermoplastic elastomers segment is

witnessing the fastest growth, heavily supported by its ease of closed-loop

recyclability, fast injection-molding cycle times, and ability to operate

safely alongside complex electric vehicle components without the need for lengthy,

energy-intensive vulcanization steps.

Regional Insights

- Asia-Pacific dominates

the Automotive Elastomers Industry, driven by rapid industrial

development, massive automotive assembly lines in China, Japan, and India,

and heavy local manufacturing of cost-efficient synthetic polymers.

- Europe exhibits

steady growth, heavily regulated by strict vehicular carbon emission

targets and a strong regional focus on circular economy mandates that

encourage the deployment of certified recyclable and bio-derived

automotive elastomers.

- North

America accounts for a substantial market share, supported by

high capital investments in electric vehicle manufacturing clusters, the

accelerating implementation of high-end consumer luxury trucks, and strong

demand for advanced crash safety and NVH solutions.

- Middle

East & Africa and South & Central America are

gradually expanding due to escalating investments in expanding localized

automotive parts production hubs, rising regional vehicle assembly

capabilities, and concentrated infrastructure efforts to modernize

commercial transportation networks.

Top Players in the Automotive Elastomers Industry

The market is highly competitive, with leading manufacturers

focusing on R&D investments, strategic bio-based feedstock supplier

partnerships, and expanding their global compounding facilities to optimize

long-term material lifecycle stability.

- BASF

SE

- Exxon

Mobil Corporation

- LANXESS

AG

- The

Dow Chemical Company

- LG

Chem Ltd.

- DuPont

de Nemours, Inc.

- Arkema

SA

- Evonik

Industries AG

- Asahi

Kasei Corporation

- SABIC

(Saudi Basic Industries Corporation)

These companies continue to invest heavily in advanced

chemical engineering and materials science simulation systems to produce

tailored compounding formulations that meet the exact physical performance,

low-emission, and long-term fluid resistance requirements of their global

automotive OEM and component manufacturing clientele.

Technological Innovations

Technological advancements in molecular tailoring and

additive compounding are significantly transforming the Automotive Elastomers

Market. Manufacturers are optimizing modern elastomer batches by integrating

nano-filler materials and structural reinforcements, enabling seals and hoses

to dynamically withstand high pressure and reduce hydraulic fluid

micro-permeation in real time.

Furthermore, innovations in 3D-printable elastomeric

filaments and flexible prototyping lattices are gaining traction. Polymer

design houses are increasingly commercializing high-efficiency thermoplastic

grades that allow manufacturers to customize, iterate, and produce intricate

structural gaskets for low-volume niche electric vehicle platforms, completely

removing the need for expensive dedicated steel molds.

The development of integrated digital material twin

simulation tools is also opening new frontiers, allowing automotive design

engineers to completely simulate, test, and debug the long-term

stress-relaxation and thermal aging behavior of specific elastomer

configurations virtually before executing physical manufacturing rollouts,

minimizing costly material waste and testing downtime.

Future Market Outlook

The future outlook for the Automotive Elastomers Industry

remains highly positive. As global supply chains increasingly prioritize

vehicle weight reductions, regulatory sustainability, and long-range electric

mobility architectures, the transportation sector will continue to transition

away from traditional rigid metallic assemblies toward highly adaptive, modular

elastomer layers.

The ongoing expansion of lightweight

"Material-as-a-Service" design networks, alongside the rising

integration of smart functional elastomers embedded with responsive sensory

elements for real-time wear monitoring, is expected to create substantial

growth opportunities. Manufacturers that prioritize seamless software-aided

mold optimization, robust low-emission compounding compliance, and lightweight,

high-temperature resistant formulations will be best positioned to capture

market share in the coming years.

Frequently Asked Questions (FAQs)

What is the main operational difference between thermoset

and thermoplastic elastomers in vehicles?

Thermoset elastomers undergo a permanent chemical

cross-linking process (vulcanization) that provides superior high-heat

resilience and structural sets, but they cannot be re-melted or recycled.

Thermoplastic elastomers (TPEs) combine the physical flexibility of rubbers

with the rapid processing advantages of plastics, allowing them to be

repeatedly melted down, reshaped, and fully recycled into new automotive parts.

How do automotive elastomers contribute to electric

vehicle range extension?

By replacing heavy metal parts, steel bracket linings, and

traditional thick rubbers with high-strength, thin-walled thermoplastic

elastomers, automotive engineers can achieve significant vehicle

lightweighting. Lowering overall vehicle weight directly reduces the energy

required for propulsion, thereby extending battery range.

How do digital material twins assist in automotive

elastomer selection?

A digital material twin is an advanced virtual replica that

simulates a polymer formulation's exact physical, chemical, and thermal

properties under extreme conditions. It allows chemical engineers to

stress-test elastic fatigue, fluid exposure degradation, and compression

profiles in a digital space, ensuring zero part failure before starting

production runs.

Can modern automotive elastomers function reliably inside

high-heat EV batteries?

Yes, specialized engineering grades like fluoroelastomers

(FKM) and engineered thermoplastic vulcanizates (TPVs) feature enhanced ingress

protection and exceptional thermal barriers. They are specifically formulated

to handle structural insulation, protect cells from electrical short-circuits,

and withstand localized thermal runaway pressures without degrading.

Browse More Reports:

Agriculture Bactericides Market

About Us

Business Market Insights is a market research platform that

provides subscription service for industry and company reports. Our research

team has extensive professional expertise in domains such as Electronics &

Semiconductor; Aerospace & Defense; Automotive & Transportation; Energy

& Power; Healthcare; Manufacturing & Construction; Food &

Beverages; Chemicals & Materials; and Technology, Media, &

Telecommunications.

Contact Us

If you have any questions about this report or would like

further information, please contact us:

Contact person: Ankit Mathur

Email: sales@businessmarketinsights.com

Phone: +16467917070

Comments

Post a Comment