Global Hearing Care Devices Market Analysis with US$ 48.41 Billion Forecast by 2033

Technological innovation is

reshaping the global Hearing Aids Industry, with manufacturers increasingly

developing compact, high-performance devices that provide superior sound

amplification and enhanced user convenience. Growing adoption of connected hearing

solutions and rising demand for personalized hearing care are supporting

long-term market growth.

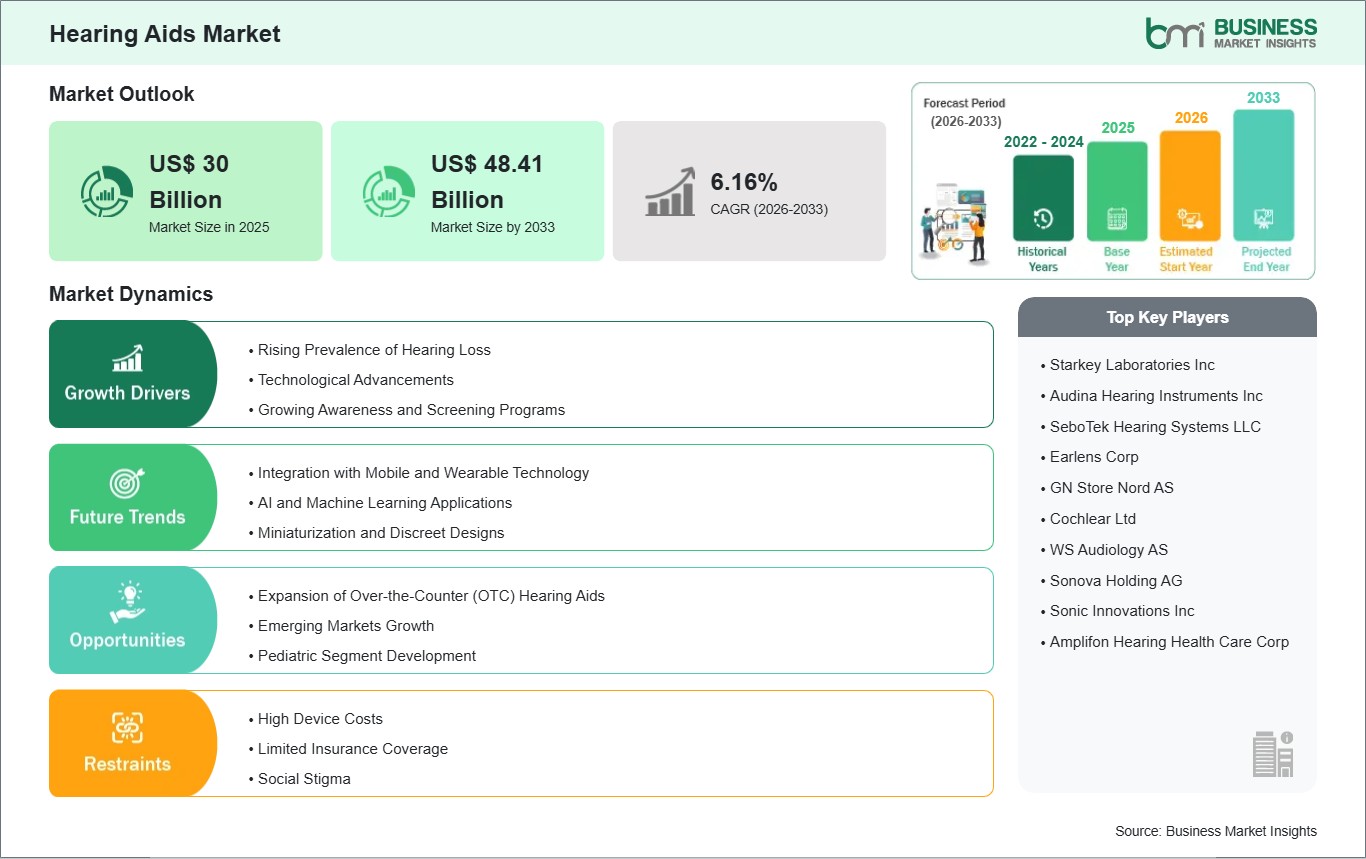

According to Business Market

Insights, the global Hearing

Aids Market was valued at US$ 30 billion in 2025 and is anticipated

to reach US$ 48.41 billion by 2033. The market is projected to grow at a CAGR

of 6.16% during the forecast period from 2026 to 2033.

Advancements in miniaturized

digital signal processing (DSP), rechargeable lithium-ion battery blocks,

artificial intelligence-driven soundscape optimization, and low-energy wireless

connectivity are resetting the market landscape. Crucially, recent regulatory

relaxations most notably the historic approval of over-the-counter (OTC)

hearing aid classifications have unlocked extensive direct-to-consumer

distribution models. These structural shifts have significantly lowered

financial entry barriers, encouraged vibrant cross-industry technological

collaborations, and expanded clinical treatment pathways into previously

underserved mild-to-moderate hearing loss segments worldwide.

What Is a Hearing Aid?

A hearing aid is a specialized

medical device comprising miniature acoustic components microphones,

micro-amplifiers, digital processing chips, and micro-speakers meticulously

calibrated to compensate for localized inner ear hair cell deficiencies or mechanical

auditory pathway damage. Unlike general audio amplifiers, modern hearing aids

do not merely boost total ambient volume. Instead, they dynamically analyze

spatial sound environments, separate human speech frequencies from disruptive

background noise, and route tailored acoustic outputs directly into the user's

ear canal, thereby protecting remaining auditory reserves and optimizing

long-term speech comprehension metrics.

Modern hearing aids operate across

two primary product categories: non-invasive hearing aid devices and surgically

anchored hearing implants. Devices vary across diverse physical form factors,

including traditional Behind-the-Ear (BTE) units, highly discreet

Receiver-in-the-Ear (RITE/RIE) layouts, and custom-molded In-the-Ear (ITE) or

completely In-the-Canal (ITC) architectures. Conversely, for profound or

complex cases where sound amplification is clinically insufficient, specialized

hearing implants such as advanced multi-channel cochlear systems or

bone-anchored devices surgically bypass dysfunctional acoustic mechanics to

stimulate the auditory nerve or mastoid bone directly via micro-electrical

pulses.

Download Sample Report: https://www.businessmarketinsights.com/sample/BMIPUB00032626

Market Drivers

A primary driver accelerating the

global Hearing Aids Industry is the Skyrocketing Global Prevalence of

Presbycusis and Disabling Hearing Loss. According to epidemiological data, over

1.5 billion individuals globally experience some degree of auditory impairment,

with hundreds of millions living with severe or disabling hearing loss. Because

unmanaged hearing degradation in older adults is directly linked to

accelerating cognitive decline, profound social isolation, clinical depression,

and an elevated risk of physical falls, public health organizations and family

networks are aggressively prioritizing early audiological screening and timely

device intervention, driving non-cyclical, volume-based market expansion.

The historic regulatory

normalization and commercial rollout of Over-the-Counter (OTC) Hearing Aids

serves as another critical driver. Historically, acquiring a hearing aid

required a mandatory, costly, and multi-stage clinical pipeline involving

professional ENT consultations, audiology exams, and bespoke clinical

programming. The passage of regulatory frameworks permitting direct OTC sales

for mild-to-moderate hearing impairments has democratized market access. Major

consumer tech brands are partnering with established medical manufacturers to

introduce highly accessible, self-fitting acoustic solutions directly through

mainstream retail and digital e-commerce channels, expanding the active

consumer pool.

Additionally, the rapid

integration of Next-Generation Wireless Environments and Smart Sound

Optimization platforms acts as a powerful catalyst. Modern consumers expect

medical devices to interface seamlessly with their everyday digital ecosystems.

The addition of Bluetooth Low Energy (LE) Audio and Auracast broadcast

technologies allows hearing aids to act simultaneously as premium communication

headsets, streaming crystal-clear audio from smartphones, public public-address

systems, and television modules directly into the user’s ear. This

technological convergence has effectively neutralized the historical social

stigma associated with wearing hearing equipment, driving rapid adoption among

tech-savvy demographics.

Market Segmentation

By Type

- Prescription

Hearing Aids (Clinically fitted, high-power systems targeting complex,

severe, or profound auditory structural loss)

- Over-the-Counter

(OTC) Hearing Aids (Self-adjusting, highly accessible devices tailored for

mild-to-moderate hearing impairments)

By Product Type

- Hearing

Aid Devices (Receiver-in-the-Ear (RITE/RIE), Behind-the-Ear (BTE),

In-the-Ear (ITE), and Canal styles)

- Hearing

Implants (Surgically placed Cochlear Implants and specialized

Bone-Anchored Conduction Implants)

By Technology

- Digital

Hearing Aids (Dominating market value through multi-channel compression,

AI noise dampening, and programmable frequency profiles)

- Conventional

/ Analog Hearing Aids (Legacy formats limited to linear, baseline sound

wave amplification)

By Type of Hearing Loss

- Sensorineural

Hearing Loss (The largest application vertical resulting from inner ear

hair cell or auditory nerve degradation)

- Conductive

Hearing Loss (Resulting from fluid barriers, physical obstructions, or

structural outer/middle ear anomalies)

By Patient Type

- Adults

& Geriatric Cohorts (The clear volume-leading patient base driven by

age-related presbycusis and occupational acoustic wear)

- Pediatric

Demographics (Specialized micro-scaled configurations optimizing

early-stage language acquisition and classroom learning integration)

By Distribution Channel

- Audiology

Clinics & ENT Centers (The leading channel for high-value prescription

diagnostics and complex surgical implant fittings)

- Retail

Pharmacies & Specialized Optical/Hearing Chains (High-velocity

transactional storefronts rapidly adopting OTC product placements)

- Online

E-Commerce Channels (The fastest-growing direct-to-consumer segment

supported by smartphone-driven self-calibration software)

The Digital Hearing Aids segment

commanded the overwhelming majority of global market revenue in 2025, driven by

patient demands for real-time sound customization and seamless smart

connectivity. Concurrently, the Receiver-in-the-Ear (RITE) product format held

the dominant physical design share due to its superior blend of acoustic

delivery and near-invisible aesthetic placement, while the online e-commerce

distribution vertical is tracking the fastest projected compound growth rate as

consumer purchasing habits favor self-directed OTC digital checkouts.

Regional Insights

- North

America holds the leading revenue share of the global hearing

aids market, capturing roughly 42% of the overall geographic matrix. This

market presence is sustained by an ultra-advanced audiological diagnostic

network, extensive public awareness campaigns regarding the cognitive

impacts of untreated hearing loss, and rapid retail deployment following

the formal legalization of direct OTC assistive hearing lines within the

United States.

- Europe maintains

a highly sophisticated, deeply consolidated market footprint, supported by

comprehensive universal healthcare coverage models and state-subsidized

device procurement pipelines across Germany, France, Denmark, and the UK.

Crucially, Western Europe serves as the global industrial R&D

epicenter for hearing assistance technology, housing several of the

world's premier audiologic engineering syndicates.

- Asia-Pacific is

recording the highest projected CAGR during the forecast matrix, propelled

by aggressive healthcare infrastructure build-outs, surging middle-class

disposable capital, and rapidly aging demographic profiles across China,

India, and Japan. Strategic retail acquisitions by global brands and the

localized launch of ultra-affordable, AI-powered hearing devices are

driving massive volumetric market penetration across emerging APAC

communities.

- Rest

of the World (Middle East & Africa and South America) is

demonstrating steady incremental growth, supported by targeted expansions

of private ENT clinic networks within prominent urban zones, international

medical outreach programs delivering subsidized pediatric cochlear care,

and expanding municipal hearing screening mandates.

Top Players in the Industry

The competitive marketplace

features a highly consolidated industrial structure, with a select group of

global life science and medical audio conglomerates controlling the vast

majority of international patent portfolios, clinical networks, and supply-chain

pipelines.

- Sonova

Holding AG

- Demant

A/S

- GN

Store Nord A/S

- WS

Audiology AS

- Starkey

Hearing Technologies

- Cochlear

Ltd.

- Audina

Hearing Instruments Inc.

- Eargo,

Inc.

- MED-EL

GmbH

- Amplifon

S.p.A.

Technological Innovations

The industrial deployment of Deep

Neural Networks (DNN) and Edge-AI Sound Processing within miniature hearing aid

architectures represents a massive technological milestone for the industry.

Historically, hearing aids utilized rigid, rule-based algorithms to suppress

background noise, which frequently resulted in muffled, unnatural speech

delivery in echo-heavy or crowded environments. Next-generation smart hearing

aids incorporate advanced onboard neural processing chips trained on tens of

millions of distinct acoustic soundscapes. These intelligent modules scan the

user's surrounding audio field hundreds of times per second, executing

instantaneous adjustments to suppress abrupt sound spikes and emphasize human

vocal clarity based on the wearer's immediate environmental context.

Concurrently, the transition to

Bluetooth Low Energy (LE) Audio and the introduction of Auracast Broadcast

Audio are radically redefining the functional parameters of assistive hearing.

Traditional Bluetooth streaming causes heavy battery drain, requiring large

physical device frames and frequent battery replacements. Bluetooth LE Audio

utilizes highly efficient compression codecs to stream high-fidelity

multi-stream audio with minimal power draw. Furthermore, the incorporation of

Auracast enables a single audio transmitter such as a microphone in a lecture

hall, an airport information terminal, or a public cinema system to broadcast

high-definition audio streams directly to an unlimited number of nearby

Auracast-enabled hearing aids simultaneously, entirely bypassing ambient room

echo and maximizing public accessibility.

Future Market Outlook

The long-term trajectory for the

Hearing Aids Market remains exceptionally strong. As international healthcare

guidelines permanently recognize auditory health as a critical, non-negotiable

metric of overall healthy aging, and ongoing global demographic realignments

expand the base consumer population requiring reliable hearing management, the

global adoption of digital and smart acoustic systems will scale consistently.

Future research and development

capital will be heavily directed toward the commercialization of multi-modal

health-tracking hearing aids equipped with integrated biometric sensors capable

of monitoring real-time heart rate, tracking daily steps, and issuing automated

emergency alerts via cloud links if an elderly user experiences a physical

fall. Device developers that successfully balance advanced micro-acoustic

processing with comfortable, long-lasting physical structures and competitive

pricing profiles will comfortably command long-term global market leadership.

Frequently Asked Questions

(FAQs)

What product category currently

commands global hearing aids market revenue?

The Digital Hearing Aids segment

commands the dominant revenue share, driven by widespread patient demand for

programmable multi-channel sound modification, automated ambient noise

dampening, and seamless direct wireless connectivity with smart devices.

How have over-the-counter (OTC)

regulatory paths changed the market?

OTC regulatory pathways allow

consumers with mild-to-moderate hearing loss to purchase self-fitting hearing

aids directly from consumer retail electronics and online storefronts without a

mandatory clinical prescription, substantially reducing acquisition costs and

increasing market penetration.

What are the acoustic benefits

of Thulium and Deep Neural Network (DNN) features in modern hearing aids?

Integrated Deep Neural Networks

instantly analyze ambient sound environments, separating speech from chaotic

background noise in real time. This allows the hearing aid to automatically

optimize voice clarity and minimize listening fatigue in crowded environments

like restaurants or transit hubs.

Which geographic region is

exhibiting the fastest growth rate for hearing aids?

The Asia-Pacific region is

tracking the fastest projected compound growth rate, propelled by rapid

hospital modernizations, expanding public and private insurance accessibility,

and a massive, expanding geriatric demographic requiring auditory correction

therapies in China and Japan.

Browse More Reports:

Diagnostic Imaging Equipment Market

Asia Pacific Cancer Hormone Therapy Market

About Us

Business Market Insights is a

market research platform that provides subscription service for industry and

company reports. Our research team has extensive professional expertise in

domains such as Electronics & Semiconductor; Aerospace & Defense;

Automotive & Transportation; Energy & Power; Healthcare; Manufacturing

& Construction; Food & Beverages; Chemicals & Materials; and

Technology, Media, & Telecommunications.

Contact Us

If you have any questions about

this report or would like further information, please contact us:

Contact person: Ankit Mathur

Email: sales@businessmarketinsights.com

Phone: +16467917070

Comments

Post a Comment