Global Isocyanates Market Analysis with US$ 7.8 Billion Forecast by 2033

Growing demand for polyurethane-based products is driving the continued advancement of the global Toluene Diisocyanate (TDI) Industry. Key growth factors include rising consumption of flexible foams in furniture and bedding applications, increasing use in automotive interiors, and expanding demand for insulation materials within the construction sector.

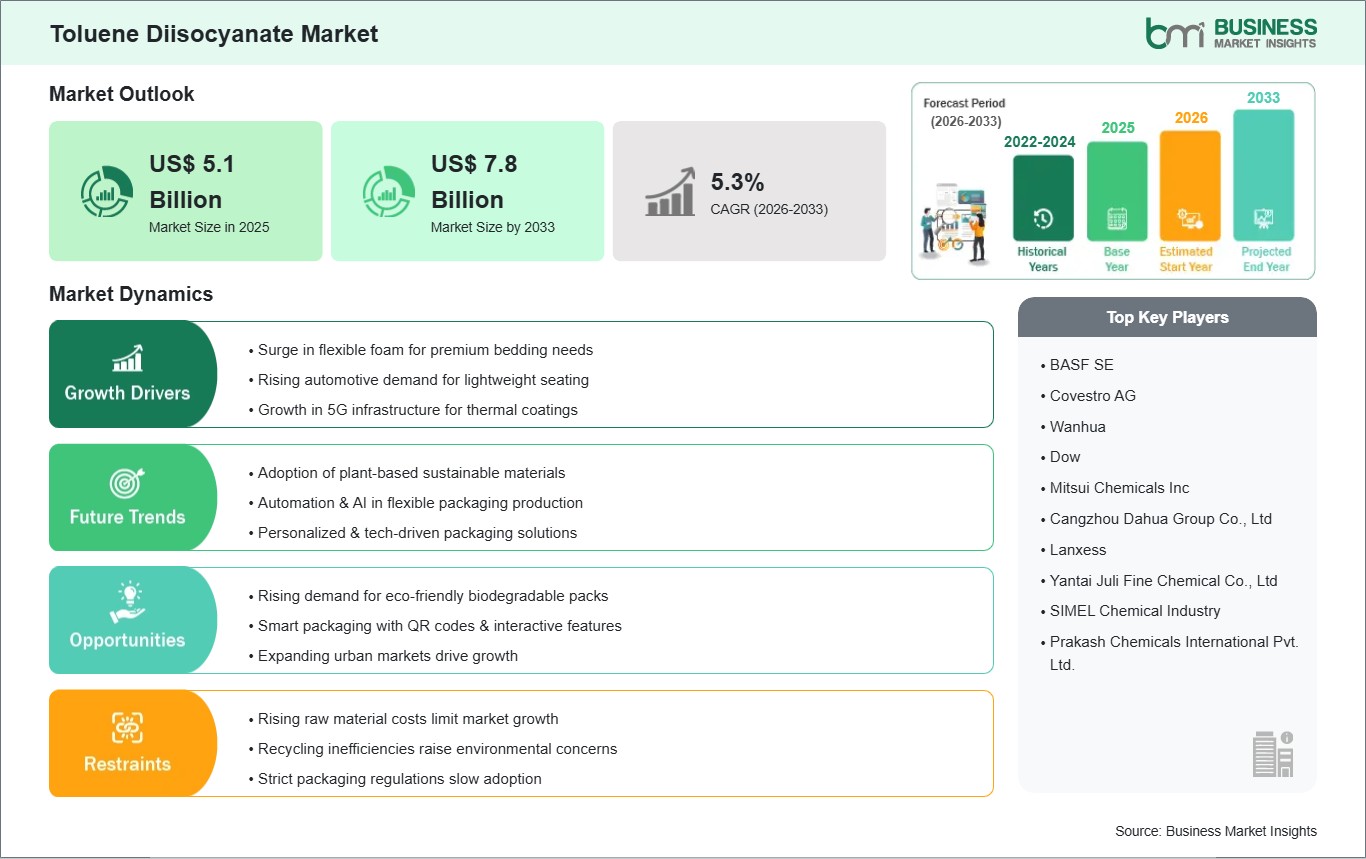

Business Market Insights projects the global Toluene

Diisocyanate Market to grow steadily, reaching US$ 7.8 billion by

2033 from US$ 5.1 billion in 2025. The market is expected to record a CAGR of

5.45% over the forecast period spanning 2026 to 2033.

Advancements in product performance, process improvements,

and the development of lower-emission production routes are continuously

reshaping the competitive landscape. Leading global chemical conglomerates are

prioritizing capital efficiency and strategic supply chain localization to

offset volatile feedstock prices. By aligning manufacturing capacities with

rapid downstream demand in expanding urban clusters, industry participants are

securing sustained profitability across highly competitive regional blocks.

What Is Toluene Diisocyanate?

Toluene Diisocyanate (TDI) is a highly reactive aromatic

diisocyanate chemical intermediate that is fundamentally essential for

synthesizing flexible polyurethane polymers. Commercially manufactured through

a multi-step process involving the nitration of toluene to yield

dinitrotoluene, followed by catalytic hydrogenation to form toluene diamine,

and final phosgenation, TDI exists primarily in two main isomers: 2,4-TDI and

2,6-TDI. The most globally ubiquitous formulation is TDI 80/20, a specific

blend of 80% 2,4-isomer and 20% 2,6-isomer, which commands the largest volume

of global industrial consumption.

TDI delivers profound performance advantages over

traditional cushioning and insulation alternatives by imparting exceptional

mechanical elasticity, superior load-bearing capacity, and outstanding physical

resilience to the final polymer matrix. Its inherently lower viscosity and

rapid reactivity grant critical processing benefits that ensure highly uniform

cell structures, enhanced tear resistance, and optimal compression sets in

advanced foam manufacturing. This versatility allows industrial converters to

seamlessly customize foam densities and create specialized formulations

tailored for demanding residential, commercial, and transportation systems.

Download Sample Report: https://www.businessmarketinsights.com/sample/BMIPUB00032577

Market Drivers

A primary driver accelerating the global Toluene

Diisocyanate Industry is the Rising Urbanization and Premium Comfort Demand in

Furniture and Bedding sectors. Rapid global population expansion, growing

middle-class disposable income, and continuous residential and commercial

housing developments particularly within emerging markets have created an

immense need for flexible polyurethane foams. Because TDI serves as the primary

chemical anchor for manufacturing mattresses, high-resilience upholstered seating,

and ergonomic pillows, shifting consumer preferences toward long-lasting

comfort products provide a robust, reliable volume base for global TDI

consumption.

The intensifying focus on Automotive Interior Lightweighting

and Acoustic Insulation serves as another vital market driver. Global

automotive original equipment manufacturers (OEMs) are increasingly

incorporating high-performance polyurethane systems to reduce overall vehicle

mass, which directly cuts carbon emissions for internal combustion engines and

extends the driving range of electric vehicles (EVs). Vehicle manufacturers

utilize TDI-rich flexible foams for seat cushions, integrated head restraints,

headliners, and complex vibration-dampening panels because the material

successfully trims weight while maximizing passenger impact protection and

cabin sound isolation.

Furthermore, stringent Energy-Efficiency Building Codes and

Infrastructure Modernization initiatives are expanding the market footprint.

Modern structural engineering practices increasingly emphasize thermal envelope

performance to reduce municipal energy expenditure. Consequently, TDI-based

coatings, adhesives, sealants, and elastomers (CASE) are experiencing broad

market penetration. These specialized chemical systems offer exceptional

weather-proofing, cross-linking density, and corrosion resistance, making them

invaluable for structural bonding, protective architectural finishes, and

energy-efficient building envelopes.

Market Segmentation

By Application

- Flexible

Polyurethane Foam (The dominant product form heavily integrated into

lifestyle and seating cushioning)

- Rigid

Polyurethane Foam (Utilized for structural thermal barriers and

refrigeration panels)

- Coatings,

Adhesives, Sealants, and Elastomers (CASE) (High-performance chemical

systems for industrial bonding and surface protection)

By End-Use Industry

- Furniture

& Interiors (The largest overall consumption vertical for comfort and

bedding applications)

- Automotive

& Transportation (Fastest-growing end-use sector supporting vehicle

lightweighting and EV thermal-acoustic solutions)

- Construction

(Driven by infrastructure investments and energy-efficient building

requirements)

- Electronics

& Packaging (Utilized for shock-absorbing foam inserts and delicate

component coatings)

- Textiles

& Others (Including synthetic leather backings and specialized

industrial compounds)

The Flexible Polyurethane Foam application segment commanded

the absolute largest revenue share of the global market matrix in 2025,

maintaining its long-standing position as the principal driver of difunctional

aromatic isocyanates due to robust international furniture and bedding trends.

Concurrently, the Furniture & Interiors sector led the end-use market

share, while the Automotive & Transportation vertical is recording the

highest projected compound growth, driven by escalating material-performance

requirements in modern electric vehicle platforms.

Regional Insights

- Asia-Pacific commands

the largest share of the global toluene diisocyanate market, holding

approximately 45% of the total geographic matrix. This dominant presence

is sustained by abundant natural feedstock availability, lower production

overheads, and extensive state-backed industrial corridors across China

and India. Widespread urbanization, rising middle-class disposable

incomes, and a flourishing domestic manufacturing hub make Asia-Pacific

the primary focal point for global foreign direct investment (FDI) and

capacity additions.

- Europe maintains

a substantial and highly regulated market footprint, capturing roughly 30%

of global demand. Regional market dynamics are heavily shaped by strict

compliance with European chemical safety frameworks and an industrial

focus on formulating low-VOC, ultra-low-emission specialty polyurethanes.

Growth in this region is primarily replacement-oriented and centers on

advanced construction insulation and premium automotive applications.

- North

America represents a premium, value-driven market block, holding

an estimated 18% share. Market expansion across the United States and

Canada is propelled by a mature polyurethane manufacturing sector,

expanding infrastructure renewal projects, and strong corporate

investments in advanced, high-performance coatings and structural

adhesives.

- Rest

of the World (Middle East & Africa and South America) is

demonstrating gradual, steady adoption patterns. Market development in

these regions is supported by localized smart city infrastructure

investments, expanding commercial hospitality construction, and growing

automotive assembly networks that elevate regional requirements for bulk

chemical intermediates.

Top Players in the Toluene Diisocyanate Industry

The competitive ecosystem is characterized by a high level

of market concentration among major multi-national chemical technology

conglomerates that manage fully integrated upstream supply chains and global

distribution networks.

- BASF

SE

- Covestro

AG

- Wanhua

Chemical Group Co., Ltd.

- Dow

- Mitsui

Chemicals Inc.

- Tosoh

Corporation

- Yantai

Juli Fine Chemical Co., Ltd.

- SABIC

(Saudi Basic Industries Corporation)

Technological Innovations

The industrial scale-up of Phosgene-Free TDI Production

Technologies represents a massive technological milestone for chemical

engineering. Traditionally, the synthesis of toluene diisocyanate relies on a

phosgenation route, which presents significant hazardous material transport,

storage, and occupational safety challenges. Next-generation manufacturing

processes are shifting toward non-phosgene alternative pathways, such as the

direct liquid-phase carbonylation of toluene diamine with dimethyl carbonate. This

breakthrough drastically reduces severe environmental exposure risks,

simplifies industrial plant safety compliance profiles, and lowers processing

capital expenditure over traditional setups.

Concurrently, material scientists are successfully deploying

Advanced Low-Emission and Bio-Based Polyurethane Foam Formulations to meet

modern environmental criteria. Downstream foam manufacturers are utilizing

optimized TDI components paired with bio-polyols derived from natural oil

feedstocks like castor or soybean oil. These innovative chemical matrixes

eliminate volatile organic compound (VOC) emissions within vehicle passenger

cabins and residential living spaces, delivering exceptional mechanical performance,

flame-retardant properties, and high compression sets while substantially

lowering the overall carbon footprint of final lifestyle consumer goods.

Future Market Outlook

The future trajectory for the Toluene Diisocyanate Market

remains robust and highly resilient. As global construction codes permanently

mandate energy efficiency and global transport sectors move aggressively toward

vehicle weight reduction, the integration of high-performance polyurethane

systems will steadily expand, preserving TDI's position as a fundamental

volume-driven industrial asset.

Future research and development capital will be heavily

directed toward the commercialization of fully circular polyurethane recycling

pathways to extract raw chemical intermediates back from post-consumer foam

waste, the optimization of advanced catalyst packages to improve raw material

conversion efficiency, and the execution of margin optimization strategies

across key manufacturing plants. Organizations that successfully balance scale

and supply chain localization while offering advanced, eco-friendly low-VOC

chemical grades will comfortably command long-term global market leadership.

Frequently Asked Questions (FAQs)

What application type currently dominates the global

toluene diisocyanate market?

The Flexible Polyurethane Foam segment holds the absolute

largest market share. This dominant presence is driven by the universal

utilization of flexible foams as the core cushioning material within the global

bedding, residential upholstery, and automotive seating sectors.

What factors are primary growth drivers for the

automotive end-use segment?

The automotive vertical is expanding due to an intense

industry focus on vehicle lightweighting to improve fuel economy and electric

vehicle battery driving ranges. TDI-based foams cut vehicle interior component

mass while ensuring superior acoustic insulation and structural comfort.

How are regulatory safety standards impacting the global

TDI supply chain?

TDI is classified as a respiratory sensitizer, leading to

highly stringent occupational exposure limits enforced by bodies like OSHA and

European regulators. These stringent worker-safety rules increase compliance

and handling costs, encouraging producers to invest heavily in low-emission

formulations and advanced automated processing systems.

Which regional block leads global toluene diisocyanate

consumption and production?

The Asia-Pacific region leads the global market, accounting

for approximately 45% of total market value. This leadership is sustained by

massive production capacities in China, rapid regional urbanization, expanding

private housing construction, and low-cost labor frameworks attracting

extensive investments.

Browse More Reports:

Automotive Plastic Additives Market

About Us

Business Market Insights is a market research platform that

provides subscription service for industry and company reports. Our research

team has extensive professional expertise in domains such as Electronics &

Semiconductor; Aerospace & Defense; Automotive & Transportation; Energy

& Power; Healthcare; Manufacturing & Construction; Food &

Beverages; Chemicals & Materials; and Technology, Media, &

Telecommunications.

Contact Us

If you have any questions about this report or would like

further information, please contact us:

Contact person: Ankit Mathur

Email: sales@businessmarketinsights.com

Phone: +16467917070

Comments

Post a Comment