Global Manual and Powered Wheelchairs Market Analysis with US$ 8.99 Billion Forecast by 2033

Technological advancements are

transforming the global Wheelchair Industry, with manufacturers introducing

lightweight materials, smart mobility features, and enhanced ergonomic designs

to improve user comfort and functionality. Growing emphasis on independent

living and patient-centered rehabilitation is further supporting the adoption

of advanced wheelchair solutions.

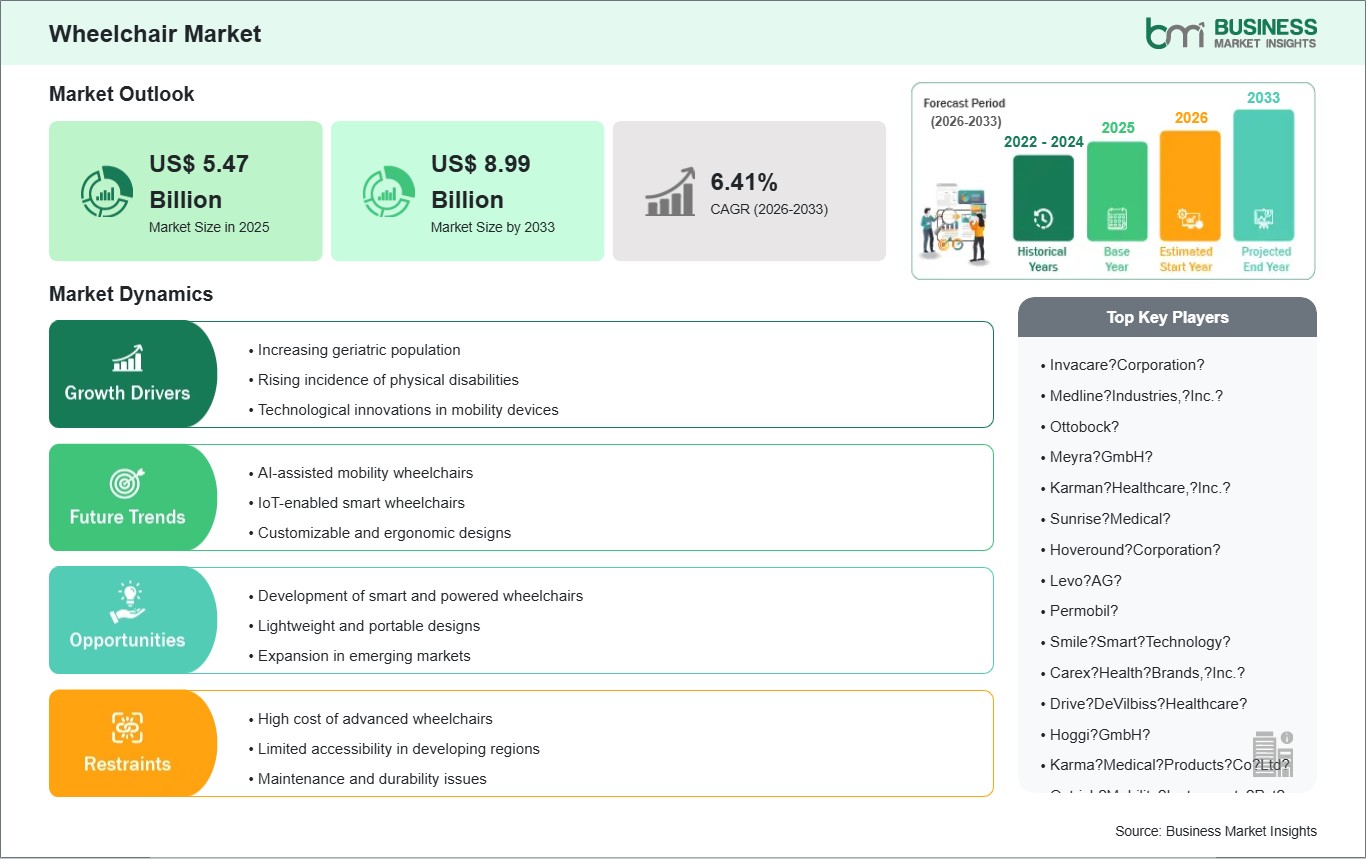

According to Business Market

Insights, the global Wheelchair

Market was valued at US$ 5.47 billion in 2025 and is anticipated to

reach US$ 8.99 billion by 2033. The market is projected to grow at a CAGR of

6.41% during the forecast period from 2026 to 2033.

Advancements in carbon-fiber

structural composites, smart omnidirectional center-wheel drive systems,

advanced joystick telemetry, and IoT-enabled remote monitoring platforms are

rapidly shifting the competitive environment. Leading medical engineering firms

are funneling substantial capital into optimizing battery performance through

high-capacity lithium-ion cells, improving pressure-redistributing seating

ergonomics, and refining terrain-adaptive tracking sensors. These innovations

are specifically engineered to mitigate upper-body strain during manual

propulsion, prevent skin breakdown and pressure ulcers during prolonged usage,

and provide intuitive, safe navigation control for individuals with severe

neurological or physical limitations.

What Is a Wheelchair?

A wheelchair is a highly

engineered personal mobility medical device incorporating a structural wheeled

frame, specialized support seating, and dedicated control interfaces designed

to compensate for temporary or permanent lower-limb dysfunction or severe

physiological walking constraints. Far exceeding standard consumer transport

chairs, clinical-grade wheelchairs are complex orthopedic systems tailored to

specific anatomical, postural, and functional requirements. They feature

advanced mechanical attributes such as adjustable center-of-gravity axels,

precision anti-tip modules, customized tension-adjustable backrests, and

ergonomic armrests and footrests designed to maintain skin integrity and

skeletal alignment across long-term indwelling cycles.

These mobility platforms operate

across highly distinct technological and drive configurations to suit various

clinical profiles. Manual wheelchairs utilize lightweight aluminum or

carbon-fiber architectures propelled entirely by the user's upper-body strength

via specialized handrims, or managed by a clinical attendant using

ergonomically balanced push handles. Conversely, Powered or Electric

Wheelchairs (EPWs) integrate sophisticated electric drivetrains, modular

suspension gear, and electronic steering modules driven by sensitive joysticks,

chin controls, or head arrays. This empowers individuals with profound physical

impairments such as high-level quadriplegia or advanced muscular

dystrophy to achieve complete spatial autonomy without physical

exhaustion.

Download Sample Report: https://www.businessmarketinsights.com/sample/BMIPUB00032640

Market Drivers

A primary driver accelerating the

global Wheelchair Industry is the Inexorable Shift in Global Geriatric

Demographics and Age-Related Physical Disabilites. The global population aged

60 years and older is scaling at an unprecedented rate, naturally resulting in

a higher baseline prevalence of chronic musculoskeletal conditions like severe

osteoarthritis, advanced osteoporosis, and age-related balance disorders.

Because restricted independent mobility severely limits an elderly individual's

ability to engage in activities of daily living (ADLs), domestic families and

managed-care networks are systematically investing in ergonomically optimized

manual and powered wheelchair fleets to ensure safe, continuous senior mobility

and minimize secondary falling risks.

The rising global incidence of

Spinal Cord Injuries (SCIs), Traumatic Brain Injuries, and Progressive

Neurological Disorders represents another structural driver. Motor vehicle

accidents, industrial workplace trauma, and debilitating neurological conditions

such as cerebrovascular strokes, multiple sclerosis, and cerebral palsy leave

millions of individuals globally with severe, permanent mobility deficits.

Managing these complex patient profiles requires specialized, complex

rehabilitation technologies (CRT), including standing electric wheelchairs and

tilt-in-space configurations. These specialized units allow for localized

pressure relief, assist in proper bladder and circulatory function, and support

active post-trauma physical therapy regimens.

Additionally, the rigorous

enforcement of Stringent Accessibility Mandates and Hospital Infrastructure

Modernizations acts as a powerful catalyst. Municipal regulatory bodies and

global public health watchdogs have instituted strict accessibility criteria

across commercial environments, public transportation grids, and clinical care

facilities. Hospitals, rehabilitation centers, and ambulatory clinics are

compelled to regularly update and expand their institutional transit equipment

to safely manage fluctuating patient loads and transport bariatric or disabled

patients securely between diagnostic rooms and surgical suites, generating

non-cyclical, volume-based institutional procurement contracts.

Market Segmentation

By Product

- Manual

Wheelchairs (Dominating the volume baseline due to structural durability,

low maintenance costs, and high accessibility across emerging economies)

- Powered

/ Electric Wheelchairs (Expanding swiftly via sophisticated center-wheel

drive modules and high-capacity lithium battery integration)

- Smart

Wheelchairs (An emerging high-tech frontier incorporating terrain sensors,

obstacle-avoidance arrays, and IoT telemetry links)

By Type

- Center

Wheel Drive (Leading structural maneuverability due to an exceptionally

tight turning radius ideal for confined indoor tracking)

- Front

Wheel Drive (Optimized for robust outdoor performance, overcoming physical

curbs, and managing uneven terrain traction)

- Rear

Wheel Drive (A classic powered layout offering high directional stability

and aggressive high-speed tracking)

- Standing

Electric Wheelchairs (Specialized dynamic configurations that transition

users into fully upright positions to assist physiological circulation)

By Application

- Neurologically

Impaired (The primary application vertical driven by intensive customized

support needs for stroke, trauma, and neuromuscular patients)

- Handicap

Patients (Catering to congenital anomalies, lower-limb amputations, and

permanent structural orthopedic constraints)

- Others

(Including temporary post-surgical recovery, bariatric transport support,

and general geriatric frailty management)

By Usage

- Adult

(The clear volume-leading user demographic, deeply intertwined with global

senior population booms and adult lifestyle illnesses)

- Paediatric

(Highly specialized micro-scaled architectures engineered with

growth-adaptable frames to track childhood physical development)

By End-User

- Rehabilitation

Centers (The premier institutional purchasing tier demanding

high-performance, resilient chairs for active physical therapy)

- Hospitals

and Clinics (Utilizing standard, heavy-duty manual fleets for daily

patient transfer and emergency department reception)

- Homecare

Settings (Expanding steadily via lightweight foldable structures and

highly intuitive residential powered chairs)

- Ambulatory

Surgical Centers (ASCs) (Requiring agile, easy-to-sanitize transport

models to streamline same-day outpatient discharge flows)

By Distribution Channel

- Retail

(The dominant revenue generation pathway, heavily sustained by

professional clinical fittings, custom scripting, and insurance

verification loops)

- E-Commerce

(The fastest-growing direct-to-consumer channel, driven by baseline manual

chairs, lightweight transport travel models, and digital price transparent

purchasing)

Regional Insights

- North

America holds a commanding revenue share of the global wheelchair

market, supported by a highly developed healthcare system, expansive

private and public insurance reimbursement frameworks (such as Medicare

and Medicaid), and swift adoption of premium powered mobility units.

Strict enforcement of the Americans with Disabilities Act (ADA) ensures a

continuous baseline demand across commercial and clinical facilities.

- Europe exhibits

a highly structured, substantial market presence, backed by comprehensive

universal health infrastructure and state-subsidized assistive technology

pipelines across Germany, the UK, and France. European clinical networks

prioritize strict ergonomic certifications and eco-compliant, lightweight

manufacturing processes to align with strict workplace safety and

sustainability directives.

- Asia-Pacific represents

the fastest-growing geographic block, recording an exceptional forward

growth path. This expansion is heavily propelled by massive healthcare

modernization initiatives, rising disposable incomes, expanding public

insurance accessibility, and a rapidly aging population profile across

China, India, and Japan. The localization of mass-production hubs is

significantly driving down costs, enabling extensive volume penetration

across emerging rural and urban communities.

- Rest

of the World (Middle East & Africa and South America) is

displaying steady, progressive growth patterns. Market expansion across

these sectors is driven by targeted improvements in urban private clinic

networks, expanding humanitarian distribution programs delivering basic

pediatric care, and regional public health mandates designed to enhance

community accessibility.

Top Players in the Industry

The competitive ecosystem displays

a focused framework, with specialized medical equipment conglomerates and

high-tech mobility firms maintaining clear leadership through long-term group

purchasing organization (GPO) contracts and extensive engineering patents.

- Invacare

Corporation

- Medline

Industries, Inc.

- Ottobock

- Meyra

GmbH

- Karman

Healthcare, Inc.

- Sunrise

Medical

- Hoveround

Corporation

- LEVO

AG

- Permobil

- Smile

Smart Technology

- Carex

Health Brands, Inc.

- Drive

DeVilbiss Healthcare

- Hoggi

GmbH

- Karma

Medical Products Co., Ltd.

- Ostrich

Mobility Instruments Pvt. Ltd.

Technological Innovations

The industrial integration of

Advanced Carbon-Fiber and Aerospace-Grade Alloy Matrices represents a

monumental structural breakthrough for manual wheelchair design. Historically,

conventional steel-framed wheelchairs were incredibly heavy, requiring strenuous

physical effort to propel over extended durations and putting users at high

risk for repetitive-strain shoulder injuries and rotator cuff degradation.

Next-generation custom manual chairs utilize monocoque carbon-fiber frames that

weigh under 15 pounds while matching or exceeding the structural rigidity of

steel. This extreme weight reduction minimizes rolling resistance, allows for

easy folding and vehicle transport for independent users, and significantly

reduces long-term physical fatigue for both patients and caregiving assistants.

Concurrently, the transition

toward Intelligent Smart Control Algorithms, Terrain Sensing, and IoT Connected

Telemetry is completely modernizing the powered wheelchair sector.

Next-generation electric mobility devices incorporate sophisticated gyroscopic

modules and micro-radar arrays that actively scan upcoming pathways,

automatically adjusting torque distribution to prevent tipping on steep

inclines or stabilizing steering over uneven outdoor surfaces like gravel or

grass. Furthermore, onboard IoT sensors track daily usage metrics, battery

health cycles, and positioning analytics in real time. This allows care teams

and clinicians to remotely monitor patient activity levels, optimize seating

alignment to prevent pressure injuries, and schedule preventative mechanical

maintenance before an operational component experiences field failure.

Future Market Outlook

The long-term trajectory for the

Wheelchair Market remains exceptionally strong. As international healthcare

models permanently establish independent patient mobility as a foundational

pillar of overall wellness and demographic trends continue to expand the global

base population requiring reliable movement assistance, the universal market

demand for both manual and advanced electric mobility systems will scale

continuously, defining point-of-care efficiency protocols.

Future research and development

capital will be heavily directed toward the commercialization of fully

autonomous self-navigating smart wheelchairs equipped with gaze-tracking or

brain-computer interfaces (BCIs) for patients with total paralysis, the integration

of advanced biometric health-monitoring sensors inside armrest modules to track

vitals continuously, and the further optimization of ultra-compact,

travel-friendly folding electronic solutions. Equipment developers that

successfully balance premium ergonomic seat customization with lightweight

structures and competitive pricing will comfortably secure long-term global

market leadership.

Frequently Asked Questions

(FAQs)

What product category currently

commands the dominant revenue share in the global wheelchair market?

The Manual Wheelchairs segment

holds the largest share of the market matrix, driven by their unmatched

economic affordability, zero reliance on charging infrastructure, lightweight

structural profiles, and ubiquitous deployment across domestic and professional

clinical settings globally.

Why is the Center Wheel Drive

layout preferred for indoor powered wheelchairs?

Center Wheel Drive configurations

place the primary drive wheels directly beneath the user's center of gravity,

allowing the wheelchair to turn tightly on its own axis. This unique mechanical

alignment creates the smallest possible turning radius, making it highly

optimal for navigating narrow residential hallways and compact indoor clinical

rooms.

How do carbon-fiber frames

enhance the patient or caregiver experience?

Carbon-fiber frames dramatically

lower the total physical weight of manual wheelchairs without compromising

structural integrity. This minimized weight substantially decreases upper-body

user propulsion fatigue, mitigates chronic shoulder strain, and allows

caregivers to lift and stow the device easily.

Which regional market is

recording the fastest compound growth rate for wheelchairs?

The Asia-Pacific region is

tracking the fastest projected compound annual growth rate (CAGR), propelled by

massive public and private healthcare modernizations, extensive hospital

construction campaigns, rising middle-class disposable capital, and rapidly

aging populations across China and India.

Browse More Reports:

Nuclear Medicine Equipment Market

About Us

Business Market Insights is a

market research platform that provides subscription service for industry and

company reports. Our research team has extensive professional expertise in

domains such as Electronics & Semiconductor; Aerospace & Defense;

Automotive & Transportation; Energy & Power; Healthcare; Manufacturing

& Construction; Food & Beverages; Chemicals & Materials; and

Technology, Media, & Telecommunications.

Contact Us

If you have any questions about

this report or would like further information, please contact us:

Contact person: Ankit Mathur

Email: sales@businessmarketinsights.com

Phone: +16467917070

Comments

Post a Comment