Global Non-Volatile Memory Market Analysis with US$ 59.29 Billion Forecast by 2033

The Next-Generation Memory Industry is experiencing steady growth worldwide, driven by the escalating adoption of high-performance computing platforms across diverse technology sectors, a rising global focus on data processing velocity and real-time computing precision, and the pressing need to mitigate power consumption and data transfer bottlenecks in modern enterprise infrastructures.

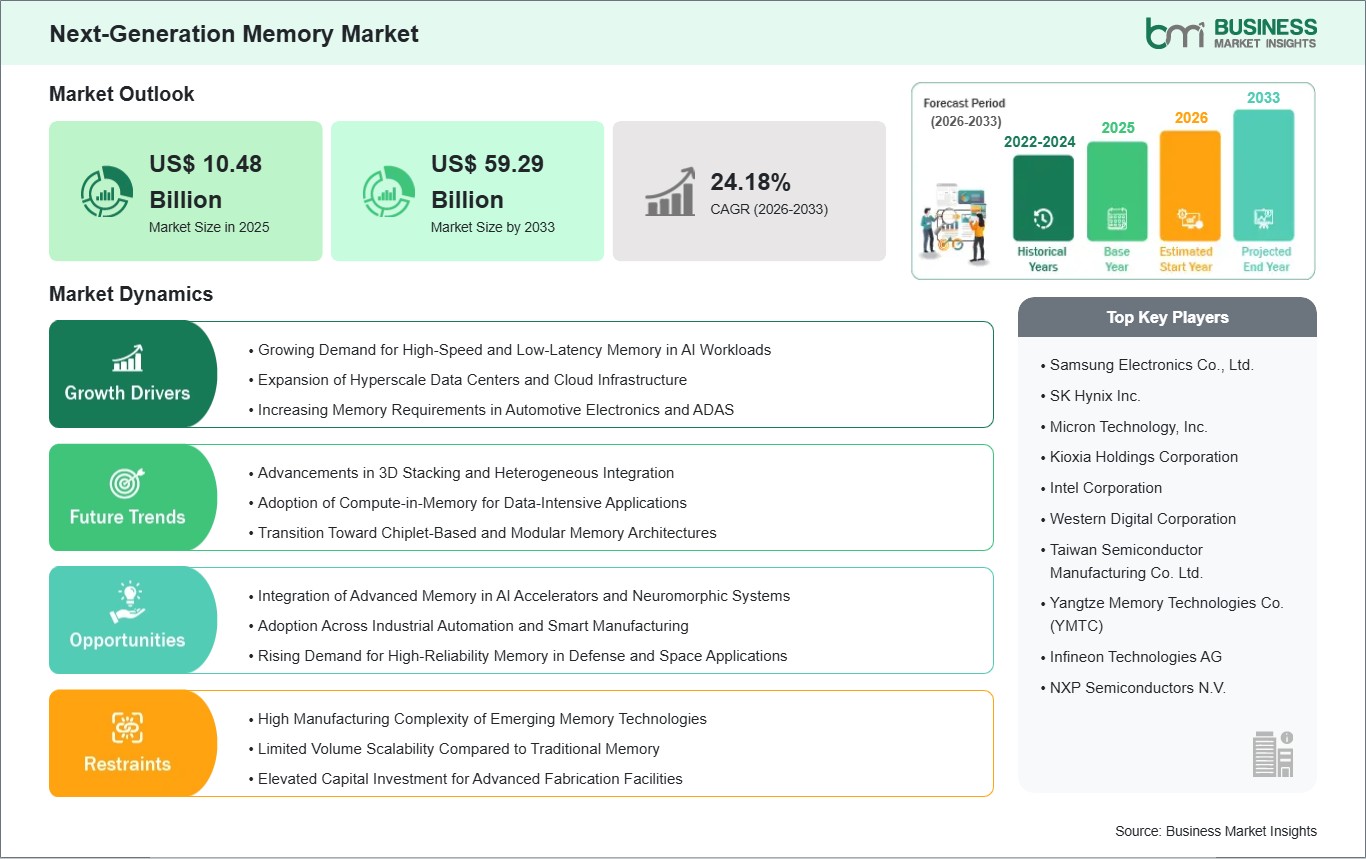

According to Business Market Insights, the global Next-Generation

Memory Market size is expected to reach US$ 59.29 Billion by 2033 from

US$ 10.48 Billion in 2025. The market is estimated to record a CAGR of 24.19%

from 2026 to 2033.

Advancements in three-dimensional (3D) memory architectures,

artificial intelligence (AI) integration in predictive heavy-workload

management, and advanced process node lithography technologies, along with the

rising deployment of high-density storage systems in secondary industries like

automotive telematics and automated industrial manufacturing hubs, are

significantly transforming the market landscape. Semiconductor fabrication

facilities are increasingly prioritizing extreme thermal resistance, flexible

ultra-low latency interfaces, and cloud-connected chiplet diagnostics to meet

shifting regulatory preferences for energy-efficient data storage frameworks

and zero-error processing turnaround.

What Is Next-Generation Memory?

Next-generation memory encompasses a comprehensive range of

advanced, high-speed, multipurpose electronic storage architectures

programmable across computing hardware networks, designed for heavy-duty system

automation and data tracking applications. Their primary objective is to

execute highly continuous, precise, and power-efficient recording of complex

data arrays and machine instructions at high speeds without manual hardware

reconfiguration bottlenecks.

Because modern digital management demands continuous

operational transparency and zero-defect data transmission control,

next-generation memory frameworks are extensively deployed across consumer

devices, cloud enterprise servers, and automated vehicle electronics.

Traditional computing configurations relied strictly on rigid, legacy volatile

storage components enclosed in localized motherboard slots. In contrast,

advanced next-generation memory configurations integrate sophisticated

non-volatile solid-state materials, deep-learning memory controller algorithms,

and advanced interface standards tailored to handle delicate peak-data

processing surges and dynamic, variable processing grids.

Download Sample Report: https://www.businessmarketinsights.com/sample/BMIPUB00032364

Market Drivers

A primary driver for the Next-Generation Memory Industry is

the rapid automation and digital transformation of the global cloud computing

and high-performance data processing sectors, particularly in the production of

hyper-scale server clusters and complex artificial intelligence training

networks. These high-tech computing fields require sub-nanosecond precision in

read/write operations and real-time cache optimization that traditional silicon

tracking methods cannot consistently achieve.

The rising operational overhead and widening skilled

engineer shortages across major microelectronics fabrication divisions also act

as a vital growth factor. Implementing automated 3D memory architectures allows

manufacturing fabs to run continuous, optimized production cycles, helping

companies maintain high chip yields while shielding their operational overhead

from global materials supply chain market volatility.

Furthermore, stringent environmental protection regulations

and corporate sustainability initiatives aimed at reducing data center

electricity consumption significantly contribute to market demand. The growing

transition toward deploying specialized low-power chips for eco-conscious

setups such as green data center infrastructures, smart grid monitoring

nodes, and electric vehicle ADAS computing boards is heavily driving market

volume.

Additionally, the increasing financial accessibility of

advanced process node wafers and standardized plug-and-play memory controller

components is prompting small and medium-sized semiconductor design houses to

adopt innovation, removing the historical barrier of high upfront capital

design investments and further propelling sustained market growth.

Market Segmentation

By Technology

- Non-Volatile

Memory

- Volatile

Memory

By Memory Interface

- DDR/LPDDR

- PCIe/NVMe

- SATA

- Others

(CXL, UCIe)

By End-Use Device

- Consumer

Electronics

- Enterprise

Storage and Data Centers

- Automotive

Electronics and ADAS

- Industrial

IoT and Manufacturing Automation

- Aerospace

and Defense

- Healthcare

and Medical Devices

The non-volatile memory segment dominates the market due to

its high flexibility, extensive historical enterprise integration, and

established track record of handling diverse data persistence requirements in

cloud servers and consumer electronics sectors. The enterprise storage and data

centers segment is witnessing the fastest growth, heavily supported by its ease

of high-capacity array programming, lower energy dissipation profiles, and

ability to operate safely alongside complex artificial intelligence infrastructure

networks without computational performance barriers.

Regional Insights

- Asia-Pacific dominates

the Next-Generation Memory Industry, driven by rapid industrial

development, massive semiconductor production projects in Taiwan, South

Korea, and China, and heavy government subsidization of local

microelectronics manufacturing initiatives.

- Europe exhibits

steady growth, heavily regulated by strict digital infrastructure

efficiency mandates and a strong regional focus on macro-level energy

conservation goals that encourage the deployment of certified low-power

and integrated memory chipsets.

- North

America accounts for a substantial market share, supported by

high capital investments in artificial intelligence data center

replacement, the accelerating implementation of high-performance edge

computing ecosystems, and strong demand for advanced computing cyber-security

solutions.

- Middle

East & Africa and South & Central America are

gradually expanding due to escalating investments in modernizing urban

digital communication hubs, reducing transmission latencies and data

center power losses, and concentrated efforts to upgrade regional

enterprise IT infrastructure.

Top Players in the Next-Generation Memory Industry

The market is highly competitive, with leading manufacturers

focusing on R&D investments, strategic embedded memory IP developer

acquisitions, and expanding their global foundry maintenance networks to

optimize long-term wafer manufacturing lifecycle stability.

- Samsung

Electronics Co., Ltd.

- Micron

Technology, Inc.

- SK

Hynix Inc.

- Kioxia

Holdings Corporation

- Infineon

Technologies AG

- Intel

Corporation

- Western

Digital Corporation

- Fujitsu

Ltd.

- Everspin

Technologies Inc.

- Avalanche

Technology Inc.

These companies continue to invest heavily in advanced

electronic engineering and hardware-software integration systems to produce

tailored computing solutions that meet the exact data retention, physical

reliability, and software interface interoperability requirements of their

global enterprise and consumer electronics clientele.

Technological Innovations

Technological advancements in chiplet architectures and

materials science are significantly transforming the Next-Generation Memory

Market. Manufacturers are optimizing modern storage arrays by integrating novel

resistive and magnetoresistive materials capable of high-density integration,

enabling systems to dynamically execute edge computing logic and correct

bit-flip errors in real time.

Furthermore, innovations in Compute Express Link (CXL) and

universal chiplet interconnect tracking are gaining traction. Memory design

houses are increasingly commercializing high-efficiency interface layouts that

allow memory blocks to orient, identify, and transmit critical telemetry

signals across heterogeneous processing units, completely removing the need for

structured localized motherboard bus positioning.

The development of integrated digital twin fabrication lines

is also opening new frontiers, allowing semiconductor engineers to completely

simulate, test, and debug entire silicon wafer manufacturing flows virtually

before deploying physical lithography masks to the fab floor, minimizing costly

production disruption downtime.

Future Market Outlook

The future outlook for the Next-Generation Memory Industry

remains highly positive. As global supply chains increasingly prioritize

high-performance computing resilience, operational agility, and sustainable

energy management, the electronics sector will continue to transition away from

legacy volatile architectures toward highly adaptive, modular next-generation

memory layers.

The ongoing expansion of subscription-based

"Storage-as-a-Service" (SaaS) business models, alongside the rising

integration of Compute Express Link protocols for ultra-low latency server

cluster coordination, is expected to create substantial growth opportunities.

Manufacturers that prioritize seamless chiplet plug-and-play analytics, robust

hardware-level security firmware encryption, and lightweight, low-power

processing-in-memory architectures will be best positioned to capture market

share in the coming years.

Frequently Asked Questions (FAQs)

What is the difference between next-generation

non-volatile memory and traditional NAND flash memory?

Traditional NAND flash memory relies on trapped electrical

charges that degrade over time and suffer from high write latencies. Advanced

next-generation non-volatile memory options, such as MRAM or ReRAM, utilize

physical state alterations (like magnetic orientation or resistive filaments)

to deliver significantly faster write speeds, near-infinite operational

endurance, and a drastically reduced energy usage profile.

What is a high-bandwidth memory (HBM) chip best used for?

High-bandwidth memory chips feature vertically stacked DRAM

dies connected via through-silicon vias (TSVs), making them highly efficient

for rapid artificial intelligence model training, high-performance

supercomputing, and complex graphics rendering operations across high-density

enterprise data center networks.

How does a digital twin help in next-generation memory

manufacturing?

A digital twin is a virtual replica of a physical

semiconductor fabrication line and its lithography parameters. It allows

microelectronics engineers to program, optimize, and stress-test chip yield

curves and process node variation limits in a digital space, ensuring zero

structural defects and saving significant time during actual physical silicon

production rollout phases.

Can next-generation memory modules operate in extreme

weather conditions?

Yes, many manufacturers produce specialized ruggedized

next-generation memory modules. These systems feature fully sealed,

high-temperature tolerant materials and robust solid-state architectures

designed to prevent thermal breakdown and heavy radiation-induced bit flips,

making them suitable for harsh aerospace deployments or sub-zero automotive

applications.

Browse More Reports:

About Us

Business Market Insights is a market research platform that

provides subscription service for industry and company reports. Our research

team has extensive professional expertise in domains such as Electronics &

Semiconductor; Aerospace & Defense; Automotive & Transportation; Energy

& Power; Healthcare; Manufacturing & Construction; Food &

Beverages; Chemicals & Materials; and Technology, Media, &

Telecommunications.

Contact Us

If you have any questions about this report or would like

further information, please contact us:

Contact person: Ankit Mathur

Email: sales@businessmarketinsights.com

Phone: +16467917070

Comments

Post a Comment