Global Pediatric Care Equipment Market Analysis with US$ 58.96 Billion Forecast by 2033

Technological innovation is transforming the global Pediatric Medical Devices Industry, with manufacturers developing specialized systems designed to accommodate the distinct anatomical and physiological characteristics of pediatric populations. Growing demand for accurate diagnostics, safer interventions, and improved patient monitoring is driving the adoption of child-focused medical technologies across healthcare facilities worldwide.

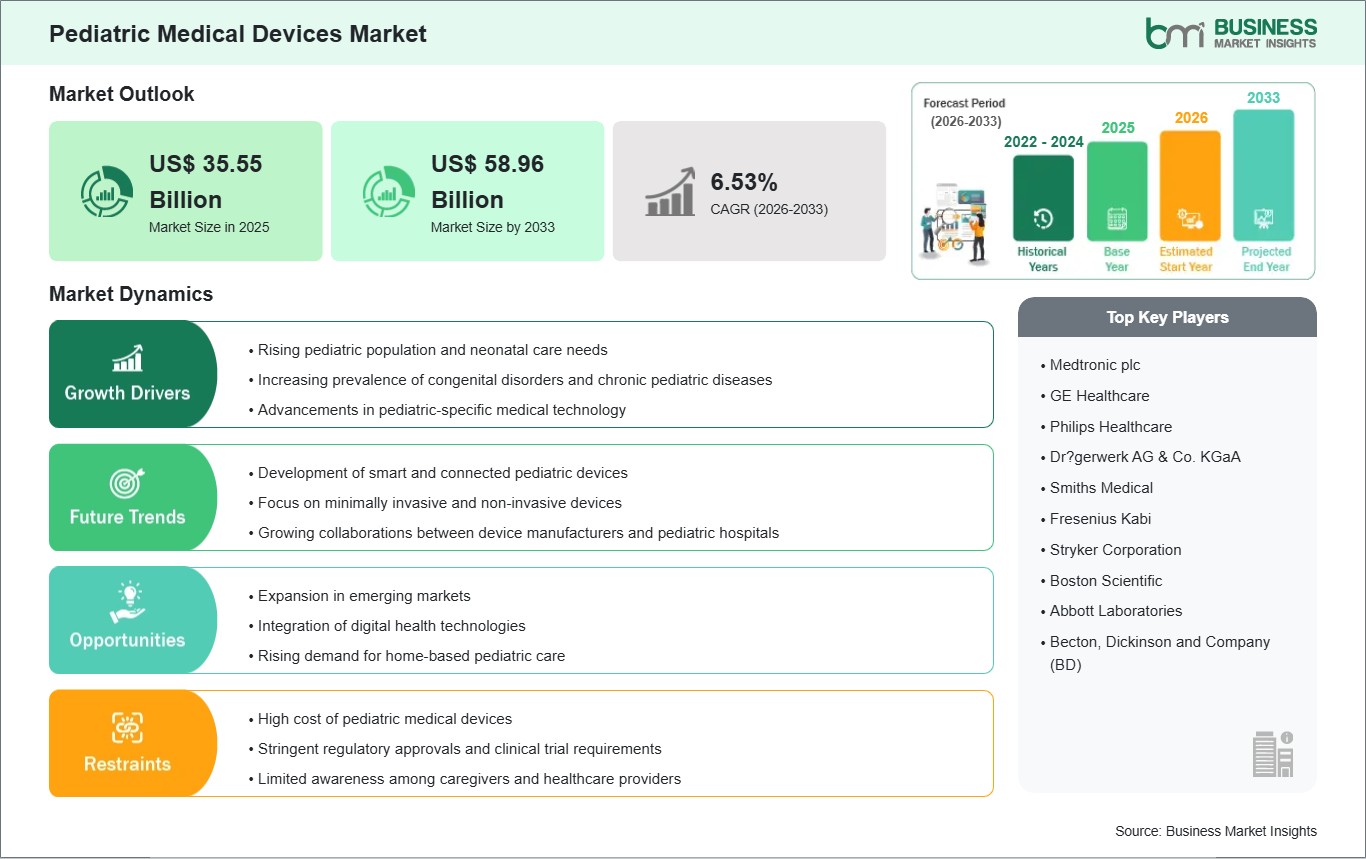

According to Business Market Insights, the global Pediatric

Medical Devices Market was valued at US$ 35.55 billion in 2025 and

is anticipated to reach US$ 58.96 billion by 2033. The market is projected to

grow at a CAGR of 6.53% during the forecast period from 2026 to 2033.

Advancements in microfluidic point-of-care testing, wireless

sensor telemetry, low-dose diagnostic imaging, and biocompatible

micro-materials are fundamentally reshaping the competitive landscape. Leading

medical technology firms are dedicating substantial R&D investments to

clear rigorous regulatory pathways, secure pediatric-specific label

indications, and integrate artificial intelligence into continuous monitoring

systems. These innovations are engineered to eliminate the stress of invasive

diagnostic protocols, provide real-time predictive health feeds in critical

care environments, and establish seamlessly scalable therapeutic solutions that

safely track a child’s physical development across critical early-life growth

cycles.

What Are Pediatric Medical Devices?

Pediatric medical devices are specialized instruments,

apparatuses, software, or reagents designed, manufactured, and clinically

validated to address the specific healthcare requirements of pediatric patient

populations. Far exceeding simple physical downsizing, these devices represent

entirely distinct engineering ecosystems. They are structurally optimized to

interact safely with delicate tissues, fragile vascular networks, and highly

sensitive respiratory tracts. These platforms incorporate unique clinical

parameters such as micro-dose pharmaceutical delivery systems, ultra-soft

non-adhesive biosensors, and specialized algorithmic baselines that accurately

account for the naturally elevated heart and respiratory rates characteristic

of young children.

These mobility, monitoring, and therapeutic platforms

operate across highly specialized product categories to support diverse

pediatric specialties. In Vitro Diagnostic (IVD) systems utilize microfluidic

"lab-on-a-chip" architectures to perform comprehensive genetic and

infectious screenings from minute blood volumes, preserving infant blood volume

integrity. Concurrently, advanced Neonatal Intensive Care Unit (NICU) systems,

including closed-loop microclimate incubators and high-frequency oscillatory

ventilators, work in tandem with non-invasive wearable telemetry patches to

stabilize premature newborns without causing dermal or airway barotrauma,

granting complete clinical security in high-acuity environments.

Download Sample Report: https://www.businessmarketinsights.com/sample/BMIPUB00032654

Market Drivers

A primary driver accelerating the global Pediatric Medical

Devices Industry is the Rising Incidence of Chronic and Congenital Pediatric

Ailments Worldwide. The global clinical landscape is recording a sustained

uptick in childhood chronic conditions, including congenital heart defects,

type-1 juvenile diabetes, severe childhood asthma, and early-life oncological

malignancies. Managing these complex patient profiles across multi-year

developmental horizons demands highly specialized, long-term diagnostic tools,

specialized insulin delivery networks, and miniature cardiology interventions,

creating a continuous and expanding commercial baseline of demand for

pediatric-specific devices.

The Surging Global Preterm Birth Rates and Subsequent

Expansion of NICU Infrastructure represent another structural driver. Clinical

data indicates that approximately 10% to 15% of all newborns globally require

specialized medical intervention or direct admission into critical care

neonatal bays. To combat infant mortality rates and optimize neurodevelopmental

outcomes, healthcare networks particularly across rapidly developing

nations are heavily funding the construction and technological modernization

of NICUs and Pediatric Intensive Care Units (PICUs), translating into

long-term, high-volume procurement contracts for specialized warming,

respiratory, and tracking gear.

Additionally, the integration of Technological Innovation

and AI-Driven Patient Telemetry acts as a powerful catalyst. The steady

integration of artificial intelligence and machine learning into wireless,

wearable pediatric monitors has revolutionized pediatric clinical workflows.

These advanced systems seamlessly extract and analyze continuous vital data

streams, using predictive modeling to alert care teams to acute physiological

degradation hours before visible symptoms manifest. By transitioning pediatric

wards from episodic, stressful manual checking to automated, non-invasive, and

predictive tracking models, healthcare providers can drastically reduce

hospital stay durations and improve recovery metrics.

Market Segmentation

By Product Type

- In

Vitro Diagnostic (IVD) Devices (Dominating the revenue matrix with an

estimated 24% market share, driven by a critical clinical reliance on

rapid infectious screening and infant metabolic profiling)

- Anesthetic

and Respiratory Care Devices (Expanding at a fast-paced 8.8% CAGR due to

escalating RSV caseloads and widespread pediatric asthma management

requirements)

- Monitoring

Devices (Experiencing rapid adoption via wireless wearable patches and

smart non-invasive pulse oximetry arrays)

- Neonatal

ICU Devices (A foundational institutional segment including precision

controlled incubators, warming therapies, and phototherapy equipment)

- Cardiology

Devices (Encompassing miniature transcatheter closing modules and custom

pediatric pacing configurations)

- Other

Instruments and Software (Including specialized low-dose pediatric

radiology systems and custom surgical instrumentation)

By End User

- Hospitals

(Commanding the leading institutional purchasing position with a 60%

market share, supported by high-complexity surgical suites and

comprehensive NICU/PICU installations)

- Pediatric

Clinics (Exhibiting a lucrative forward growth path of 8.4% to 8.5% CAGR,

driven by a shifting parental preference toward localized, specialized

outpatient tracking)

- Diagnostic

Laboratories (Utilizing specialized high-throughput pediatric IVD

equipment for rapid metabolic and genetic testing)

- Homecare

and Outpatient Settings (Expanding via lightweight, portable, and

parent-friendly monitoring and respiratory assistive designs)

Regional Insights

- North

America holds the premier position in the global landscape,

securing a commanding 46% revenue share. This market dominance is anchored

by exceptional healthcare expenditure, comprehensive medical insurance

coverage frameworks that accommodate specialized pediatric technology, and

intense R&D activities conducted by major medical technology clusters

clustered throughout the United States.

- Europe exhibits

a highly structured, substantial market presence, heavily supported by

well-funded universal public health infrastructure and centralized

research networks focused on micro-manufacturing. European clinical

networks prioritize strict ergonomic certifications and low-dose imaging

solutions to align with strict pediatric radiation safety directives.

- Asia-Pacific represents

the fastest-growing geographic block, recording an exceptional forward

growth path with a projected CAGR of 8.7%. This rapid expansion is

propelled by massive healthcare modernization campaigns, expanding public

health coverage, and aggressive investments in modern maternal and child

health centers across China and India.

- Rest

of the World is displaying steady, progressive growth patterns,

driven by targeted improvements in urban private clinic networks,

expanding international humanitarian distribution programs delivering

basic neonatal equipment, and regional public health mandates designed to

enhance infant survival rates.

Top Players in the Industry

The competitive ecosystem displays a sophisticated matrix of

diversified medical equipment conglomerates expanding their pediatric

indications and highly specialized niche innovators managing custom

developmental lines.

- Medtronic

plc

- GE

HealthCare (General Electric Company)

- Abbott

Laboratories

- Koninklijke

Philips N.V.

- Cardinal

Health Inc.

- Hamilton

Medical AG

- Atom

Medical Corporation

- Fritz

Stephan GmbH

- TSE

Medical

- Phoenix

Medical Systems Pvt. Ltd.

Technological Innovations

The implementation of Microfluidic "Lab-on-a-Chip"

Technology and Precision Low-Volume Diagnostics represents a monumental

clinical breakthrough for pediatric medicine. Historically, traditional

in-vitro diagnostic workflows required substantial blood draw volumes, a

practice that frequently induced iatrogenic anemia in premature neonates or

required highly distressing, repetitive vascular access procedures.

Next-generation pediatric IVD platforms utilize microfluidic channels that

execute comprehensive metabolic, hematological, and genetic panels from a

single micro-drop of capillary blood. This extreme reduction in sample volume

preserves neonatal blood volume integrity, minimizes patient discomfort, and

delivers critical lab-grade diagnostics directly to the point-of-care within

minutes.

Concurrently, the transition toward Wireless, Continuous

Wearable Biosensors and Advanced AI Telemetry is completely modernizing

pediatric critical care. Modern pediatric monitoring has evolved past rigid,

wired configurations that restrict movement and damage fragile infant skin.

Next-generation biosensors utilize ultra-soft, biocompatible hydrogels and

flexible wireless transmitters that adhere gently to the patient’s body. These

devices continuously stream multi-parametric vital data including blood

oxygenation, heart rate variability, and respiratory metrics into

centralized AI algorithms. The system filters out movement artifacts common in

pediatric behavior and tracks subtle physiological trends, enabling care teams

to implement early, life-saving clinical interventions before an acute crisis

occurs.

Future Market Outlook

The long-term trajectory for the Pediatric Medical Devices

Market remains exceptionally robust. As international healthcare guidelines

permanently establish specialized, age-appropriate pediatric care as a core

standard of clinical excellence and global demographic factors continue to

expand the baseline population requiring precise neonatal and childhood medical

support, the universal demand for dedicated pediatric platforms will expand

continuously, defining modern hospital procurement strategies.

Future research and development capital will be heavily

directed toward the commercialization of fully personalized pediatric implants

utilizing advanced 3D biocompatible printing, the development of intelligent,

self-adjusting prosthetic and orthopedic structures that grow organically

alongside the child’s skeleton, and the expansion of smart homecare pediatric

monitors to support seamless outpatient hospital-at-home models. Technology

developers that successfully balance strict pediatric regulatory compliance

with non-invasive, ultra-ergonomic designs will comfortably secure long-term

global market leadership.

Frequently Asked Questions (FAQs)

What product category currently commands the highest

revenue share in the global pediatric medical devices market?

The In Vitro Diagnostic (IVD) Devices segment holds the

leading revenue share, contributing approximately 24% of total product revenues

due to the critical clinical need for rapid infectious disease screening,

neonatal genetic testing, and low-volume metabolic profiling.

Why do hospitals maintain a dominant market share among

end-users?

Hospitals secure a commanding 60% market share because they

manage high-complexity pediatric surgical procedures, hold integrated

institutional supply agreements, and possess the substantial capital budgets

required to outfit modern NICU and PICU critical care bays.

What makes designing medical devices for pediatric

populations more complex than designing for adults?

Pediatric device design must accommodate extreme

physiological heterogeneity and rapid physical growth across distinct

subpopulations (neonates, infants, toddlers, adolescents). Devices must handle

faster heart and respiratory rates, highly fragile skin, and minute blood

volumes while ensuring absolute long-term safety.

Which geographic territory is recording the fastest

compound growth rate for pediatric medical devices?

The Asia-Pacific region represents the fastest-growing

market block, tracking a projected CAGR of 8.7% due to massive hospital network

expansions, rising middle-class disposable income, and aggressive public health

campaigns to reduce infant mortality rates across China and India.

Browse More Reports:

Africa High Intensity Focused Ultrasound Market

About Us

Business Market Insights is a market research platform that

provides subscription service for industry and company reports. Our research

team has extensive professional expertise in domains such as Electronics &

Semiconductor; Aerospace & Defense; Automotive & Transportation; Energy

& Power; Healthcare; Manufacturing & Construction; Food &

Beverages; Chemicals & Materials; and Technology, Media, &

Telecommunications.

Contact Us

If you have any questions about this report or would like

further information, please contact us:

Contact person: Ankit Mathur

Email: sales@businessmarketinsights.com

Phone: +16467917070

Comments

Post a Comment