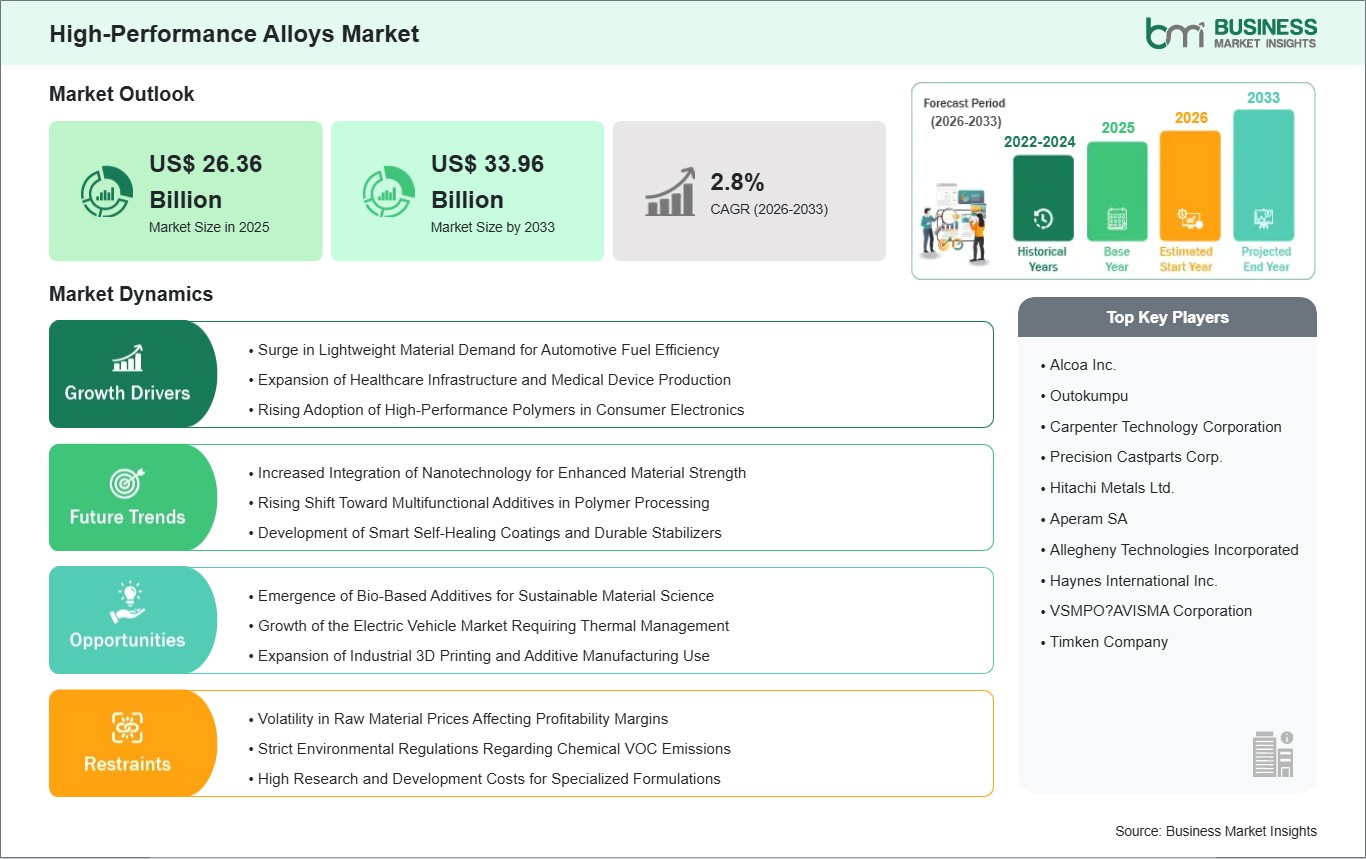

High-Performance Alloys Market Size Worth US$ 33.96 Billion by 2033 from US$ 26.36 Billion in 2025

Technological innovation is

reshaping the global High-Performance Alloys Industry, with advancements in

metallurgical engineering enabling the development of materials that offer

enhanced durability, fatigue resistance, and operational efficiency. Growing

demand for high-performance components in aerospace engines, power generation

systems, and industrial processing equipment continues to support market growth

worldwide.

According to comprehensive

market intelligence, the global High-Performance

Alloys Market was valued at US$ 26.36 billion in 2025 and is

anticipated to reach US$ 33.96 billion by 2033. The market is projected to grow

at a CAGR of 3.22% during the forecast period from 2026 to 2033.

As the global economy prioritizes

carbon-neutral operations and unparalleled fuel efficiency, heavy capital is

flowing into the research and development of recyclable alloy formulations,

high-entropy alloys (HEAs), and advanced additive manufacturing (3D printing)

capabilities. By significantly improving the strength-to-weight ratio of

critical components, high-performance alloys are enabling original equipment

manufacturers (OEMs) to radically lower fuel consumption and lifecycle

emissions across aviation, automotive, and power generation sectors.

What Are High-Performance

Alloys?

High-performance alloys also

broadly referred to as superalloys or specialty alloys are advanced metal

formulations engineered to operate seamlessly under extreme mechanical stress,

intense pressure, and highly corrosive or high-temperature environments (often

exceeding 1,200°C). Unlike conventional steel or standard aluminum, these

alloys undergo complex metallurgical processes, such as vacuum induction

melting (VIM), to ensure absolute material purity.

The base metals typically include

nickel, cobalt, titanium, or iron, which are heavily alloyed with elements like

chromium, molybdenum, or tungsten. These materials are heavily utilized in the

"hot sections" of jet engines, industrial gas turbines, nuclear

reactors, and deep-water oil drilling equipment. Their unique ability to retain

their structural integrity (creep resistance) and resist oxidation at

melting-point temperatures makes them completely indispensable to modern heavy

industry and high-tech manufacturing.

Download Sample Report: https://www.businessmarketinsights.com/sample/BMIPUB00033328

Market Drivers

The most prominent driver fueling

the market is the Aggressive Expansion of the Aerospace and Aviation

Industry. As global air travel surpasses pre-pandemic levels, commercial

airline manufacturers are facing multi-decade production backlogs. To meet

stringent environmental standards, aerospace engineers are increasingly relying

on titanium and nickel-based superalloys to build high-bypass turbofan engines

and lighter airframes. By utilizing these alloys, companies like GE Aviation

and Rolls-Royce can reduce aircraft fuel consumption by up to 25%.

Another major catalyst is

the Global Transition Toward High-Efficiency Renewable Energy Systems.

High-performance alloys are not limited to fossil fuels; they are deeply

integrated into the green energy transition. The expansion of small modular

reactors (SMRs) in the nuclear sector relies on refractory alloys that can

endure extreme radiation. Furthermore, the burgeoning hydrogen economy heavily

utilizes high-entropy alloys for solid-state hydrogen storage due to their

superior resistance to hydrogen embrittlement.

Additionally, the demand for Advanced

Defense and Military Platforms ensures steady market growth.

Modernization initiatives, such as fifth-generation fighter jet programs (e.g.,

the F-35), hypersonic missile systems, and advanced naval fleets, demand

continuous, high-volume supplies of highly specialized, heat-resistant alloys

to maintain strategic operational superiority.

Market Segmentation

By Metal Type

- Titanium

Alloys (Highly valued for their exceptional strength-to-weight ratio;

heavily dominant in aerospace airframes and medical implants).

- Aluminum

Alloys (Crucial for automotive lightweighting and general aviation).

- Iron-based

Alloys (Widely used in industrial applications requiring high durability

and moderate heat resistance).

- Magnesium

& Others (Experiencing growth due to ultra-lightweight applications in

consumer electronics and specialized automotive parts).

By Product

- Superalloys

(The dominant product segment, particularly nickel-based and cobalt-based

variants, vital for jet engines and gas turbines).

- Refractory

Alloys (Utilized in applications requiring resistance to extraordinarily

high heat, such as nuclear reactors and space exploration).

- Non-Ferrous

Alloys (Widely used across chemical processing and marine engineering for

their corrosion resistance).

- Platinum

Group (Used in specialized electronics and catalytic applications).

By Application

- Aerospace

& Defense (The absolute dominant end-user, consuming the vast majority

of premium high-performance alloys).

- Industrial

Gas Turbines (IGT) (Critical for the modernization of power grids and

efficient electricity generation).

- Oil

& Gas (Essential for deep-sea drilling equipment exposed to corrosive

saline and hydrogen sulfide environments).

- Automotive

(Growing rapidly due to the shift toward electric vehicles (EVs) requiring

lightweight materials for extended battery range).

Regional Insights

- North

America holds the dominant position in the global market,

accounting for a massive share of the revenue. This is driven by an

established aerospace manufacturing duopoly (Boeing), massive defense

budgets funding advanced fighter programs, and a robust energy sector

demanding high-performance materials.

- Asia-Pacific is

projected to be the fastest-growing region. Driven by rampant

industrialization, massive infrastructure projects, and the expansion of

domestic aerospace programs (such as China's COMAC), countries like China,

India, and Japan are heavily investing in advanced metallurgy. The

presence of major electronics manufacturing hubs in Taiwan and South Korea

further accelerates regional demand.

- Europe maintains

a highly strategic market share, heavily supported by stringent

environmental regulations driving the automotive sector toward extreme

lightweighting, alongside the massive production footprint of Airbus and

regional gas turbine manufacturers.

- Rest

of the World plays an expanding role as regions in the Middle

East invest heavily in downstream energy infrastructure, desalinization

plants, and localized aerospace repair and overhaul capabilities.

Top Players in the Industry

The market is highly consolidated,

characterized by capital-intensive operations and long-term supply contracts

with major aerospace and defense contractors.

- ATI

Inc.

- Precision

Castparts Corp. (Berkshire Hathaway)

- voestalpine

High Performance Metals

- Haynes

International, Inc.

- Alleima

- Alcoa

Corporation

- Carpenter

Technology Corporation

- Outokumpu

- Hitachi

Metals Ltd.

- Aperam

SA

Strategic Industry Challenges

Despite the critical nature of the

product, the market faces notable challenges. The primary restraint is

the High Cost of Production and Volatile Raw Material Prices.

Producing these alloys requires highly specialized vacuum melting equipment,

immense energy consumption, and skilled labor. Furthermore, the industry is

highly vulnerable to geopolitical supply chain disruptions that cause extreme

price volatility in base metals like nickel, titanium, and copper. Ensuring a

consistent, ethically sourced supply of these critical minerals remains a

pressing concern for global manufacturers.

Future Market Outlook

The long-term trajectory for the

High-Performance Alloys Market remains structurally sound and highly

optimistic. As the limits of engineering are pushed further by space

exploration, hypersonic flight, and advanced clean energy generation, the

reliance on high-performance metallurgy will only deepen. The integration of

artificial intelligence in alloy discovery and the mainstream adoption of metal

3D printing (additive manufacturing) will drastically reduce material waste and

allow for the creation of complex geometries previously thought impossible,

driving the next golden age of materials science.

Frequently Asked Questions

(FAQs)

What is the projected size of

the high-performance alloys market by 2033?

The market is projected to reach

an estimated valuation of USD 33.96 Billion by 2033, growing from a base of USD

26.36 Billion in 2025.

Why are superalloys heavily

used in the aerospace industry?

Superalloys, particularly

nickel-based ones, are used in jet engines because they retain their mechanical

strength and resist creeping and corrosion even when operating at temperatures

that approach their melting points.

How is 3D printing impacting

this market?

Additive manufacturing (3D

printing) allows engineers to print high-performance alloy components with

intricate internal cooling channels that cannot be created through traditional

casting. This reduces material waste and dramatically improves component efficiency.

Browse More Reports:

Thermal Interface Material Market

Thermo Compression Forming Market

About Us

Business Market Insights is a

market research platform that provides subscription service for industry and

company reports. Our research team has extensive professional expertise in

domains such as Aerospace & Defense; Automotive & Transportation;

Electronics & Semiconductor; Energy & Power; Healthcare; Manufacturing

& Construction; Food & Beverages; Chemicals & Materials; and

Technology, Media, & Telecommunications.

Contact Us

If you have any questions about

this report or would like further information, please contact us:

Contact person: Ankit Mathur

Email: sales@businessmarketinsights.com

Phone: +16467917070

Comments

Post a Comment