HVAC System Market Future Outlook and 6.70% CAGR Trends

The HVAC (Heating, Ventilation, and Air Conditioning) System Industry is experiencing a profound infrastructural evolution worldwide, driven by the expanding global construction sector, rapid urbanization in developing economies, and strict regulatory alignments favoring sustainable, low-carbon building frameworks and high-efficiency thermal control environments.

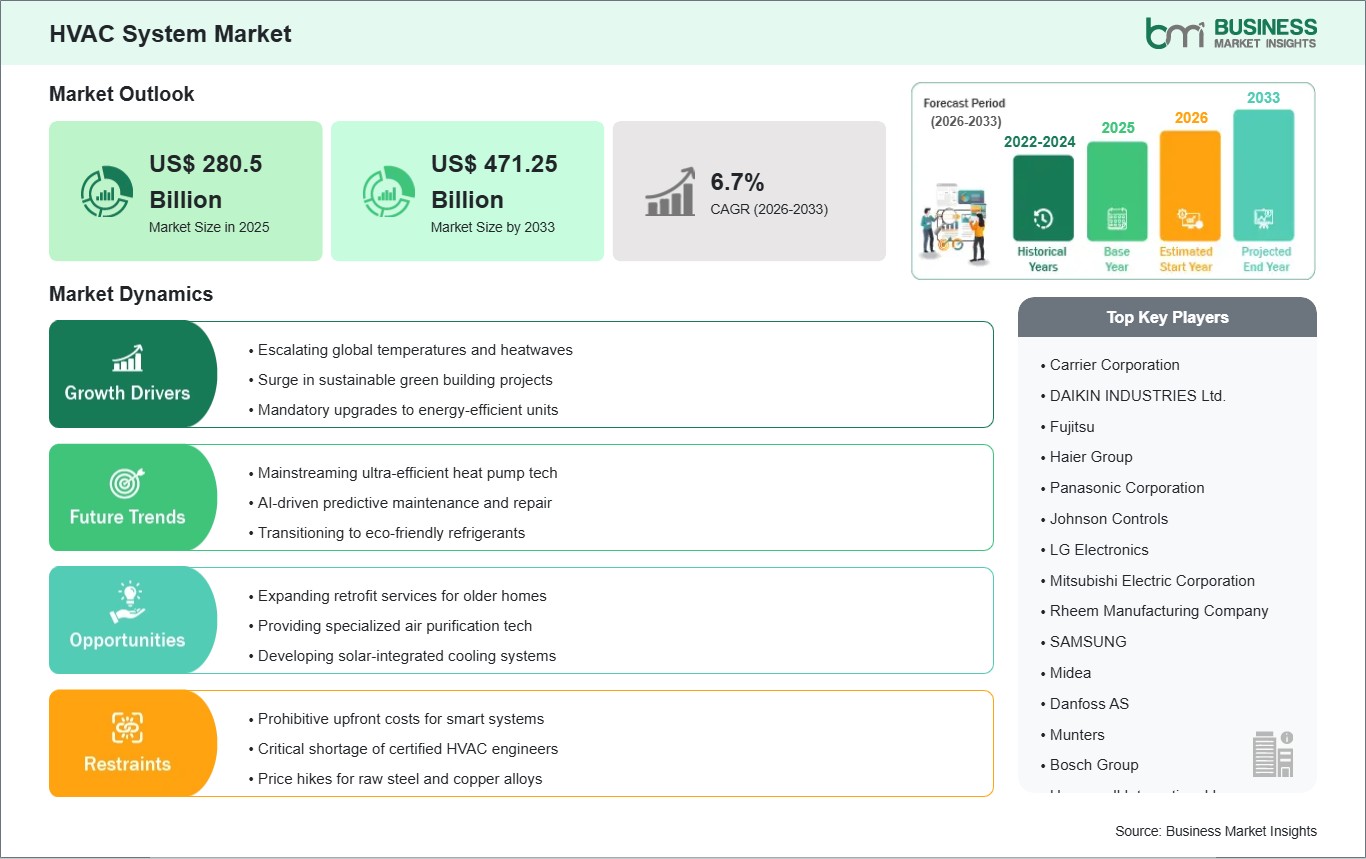

According to Business Market Insights, the global HVAC

System Market Size is expected to reach US$ 471.25 Billion by 2033

from US$ 280.5 Billion in 2025. The market is estimated to record a CAGR of

6.70% from 2026 to 2033.

Accelerating integration of smart building automation

layers, Internet of Things (IoT) sensors, and the structural migration toward

high-performance heat pumps and low-GWP (Global Warming Potential) alternatives

are fundamentally restructuring the competitive terrain. Global manufacturers

are heavily emphasizing localized climate-adaptive equipment configurations,

advanced variable refrigerant flow (VRF) delivery mechanisms, and unified

indoor air quality (IAQ) filtering systems to effectively comply with tightening

regional energy performance certificates and green building standards.

Download Sample Report: https://www.businessmarketinsights.com/sample/BMIPUB00032451

What Are HVAC Systems?

HVAC systems represent a unified, highly engineered category

of environmental control technologies designed to manage temperature, humidity

levels, air purity, and interior airflow velocities within residential,

commercial, industrial, and institutional infrastructures. Their primary

technical objective is to maintain exceptional human thermal comfort and secure

strict indoor air quality baselines while lowering localized energy footprint

metrics.

Modern HVAC ecosystems have transitioned from isolated,

electromechanical appliances into intelligent, fully network-integrated

systems. Traditional installations relied upon basic fixed-speed compressors

and manual thermostatic relays that were highly vulnerable to energy spikes and

broad ambient temperature fluctuations. Today's advanced configurations employ

sophisticated variable-speed inverter compressors, multi-stage air handling

units (AHUs), high-efficiency particulate air (HEPA) filtration arrays, and

intelligent digital controllers capable of responding dynamically to localized

occupancy variations and real-time environment metrics.

Market Drivers

A primary catalyst pushing the HVAC System Industry is the

rapid implementation of strict government policies and global energy transition

mandates, such as the U.S. Department of Energy's SEER2 efficiency standards

and European decarbonization goals. These regulations penalize non-compliant,

low-efficiency systems, driving an unprecedented surge in comprehensive

retrofitting projects across premium corporate real estate networks and older

residential complexes.

The widespread commercialization and lowering physical

hardware costs of IoT-enabled building automation software also act as a

powerful market driver. By deploying interconnected smart thermostats,

real-time tracking sensors, and localized motion-triggered cooling vents,

commercial property operators can realize substantial energy consumption

reductions, successfully lowering facility operational overhead while

mitigating carbon footprints.

Furthermore, heightened public and corporate awareness

regarding indoor air quality and airborne contaminant mitigation remains

structurally vital. This trend has established high-volume demand for

multi-layered mechanical ventilation, advanced dehumidifiers, and sophisticated

UV-C disinfection arrays built directly into new commercial and institutional

building specifications.

Market Segmentation

By Offering

- Equipment

(Heating Systems, Ventilation Systems, and Cooling Systems)

- Services

(Installation Services, Maintenance & Repair, Upgradation/Replacement,

and Consulting)

By Category

- Ductless

HVAC Systems (Duct-Free Mini-Splits, Hydronic Heating, Portable Spot

Coolers, and Others)

- Ducted

Systems (Split Systems, Packaged Heating & Air Systems, Hybrid

Systems, and Others)

By Implementation

- New

Construction

- Retrofit

Buildings

By Application

- Residential

- Commercial

(Offices, Retail Spaces, Hotels & Restaurants, and Data Centers)

- Industrial

(Manufacturing Plants, Warehouses, and Chemical Processing Facilities)

- Institutional

(Hospitals, Educational Institutes, and Government Buildings)

The cooling equipment segment captures a dominant portion of

the global market share, highly catalyzed by rising summer ambient temperatures

and intensifying heatwave cycles across the Northern Hemisphere. Meanwhile, the

industrial application segment represents the fastest-growing operational

division, requiring specialized cleanroom HVAC matrices and precise

humidity-temperature balances to safeguard automated lines across

pharmaceutical and electronics assembly fields.

Regional Insights

- Asia-Pacific maintains

an undisputed dominance in the global HVAC market share, powered by

extensive infrastructure programs, rapid urbanization throughout tier-2

cities in India and China, and highly concentrated localized components

manufacturing hubs.

- North

America represents an exceptionally high-value market hub,

anchored by extensive commercial retrofitting projects, mandatory upgrades

to higher SEER ratings, and soaring consumer demand for premium

IoT-enabled smart home ecosystems.

- Europe registers

highly progressive growth, strictly dictated by the European Commission's

net-zero mandates, accelerating the phase-out of traditional fossil-fuel

boilers in favor of residential and commercial air-to-water heat pump

systems.

- Middle

East & Africa and South & Central America are

demonstrating steady incremental volume growth, led by expanding

commercial tourism complexes, the rapid setup of critical data center

infrastructure, and targeted grid modernization efforts.

Top Players in the HVAC Industry

The global marketplace features a mix of massive

consolidation and deep technology differentiation, with leading OEMs executing

aggressive strategic partnerships and cloud-based software acquisitions to

provide unified "Climate-as-a-Service" products.

- Carrier

Global Corporation

- Daikin

Industries, Ltd.

- Trane

Technologies plc

- Johnson

Controls International plc

- Mitsubishi

Electric Corporation

- LG

Electronics Inc.

- Honeywell

International Inc.

- Lennox

International Inc.

- Panasonic

Holdings Corporation

- Samsung

Electronics Co., Ltd.

Technological Innovations

The structural integration of cloud-based Artificial

Intelligence (AI) and edge computing platforms is fundamentally altering

long-term system life cycles. Modern HVAC networks now leverage advanced

predictive maintenance algorithms that analyze real-time compressor vibration

data, refrigerant flow velocities, and ambient pressure levels to diagnose

internal line faults weeks before a physical hardware breakdown occurs,

eliminating costly downtime.

Concurrently, the manufacturing landscape is pivoting

rapidly toward eco-friendly refrigerants. Driven by strict global regulations,

chemical engineers and hardware developers have redesigned heat exchangers to

utilize propane (R-290) and R-32 blends, effectively slashing global warming

potential parameters without sacrificing raw heat transfer efficiency metrics.

Finally, the deployment of comprehensive "Digital

Twin" simulation systems is enabling architectural and HVAC design teams

to build exact thermal models of planned high-rise complexes. This software

layer allows engineers to stress-test complex airflow patterns, fluid dynamics,

and seasonal energy utilization virtually, ensuring maximum operational

performance configuration prior to physical material installation.

Future Market Outlook

The future outlook for the HVAC System Industry is

exceptionally robust. As international urban planning frameworks increasingly

enforce strict zero-emission baselines, structural thermal control will

transition from generic building utilities into highly optimized, adaptive

components of green city grids.

Future growth will be heavily concentrated in modular,

inverter-driven decentralized units, hybrid solar-assisted heat pump

technologies, and micro-zoned variable refrigerant setups. System builders that

prioritize seamless integration into open-protocol building management

networks, low-GWP chemical compliance, and superior, audited energy-efficiency

ratings will successfully command long-term global market dominance.

Frequently Asked Questions (FAQs)

What is the technical significance of the transition to

inverter compressor technology in HVAC systems?

Traditional non-inverter compressors operate on a rigid

on-and-off power cycle, causing substantial energy spikes, temperature

fluctuations, and accelerated mechanical wear. Inverter technology uses

variable-frequency drives to modulate motor speed continuously, enabling the

system to match the precise real-time thermal load of the building, which

achieves up to 40% lifecycle electricity savings.

Why are low-GWP refrigerants like R-32 and Propane

(R-290) gaining mandatory status?

Legacy hydrofluorocarbon (HFC) refrigerants possess

exceptionally high global warming potentials if leaked into the atmosphere. New

environmental regulations mandate a rapid phase-down of these compounds,

pushing the industry to adopt low-GWP alternatives like R-32 and eco-friendly

Propane, which degrade safely and offer superior thermodynamic performance.

How does an HVAC digital twin optimize building

operational expenditures?

An HVAC digital twin is a dynamic virtual replica of a

building's entire climate control system. By continuously feeding physical

sensor data into the model, facility managers can virtually simulate load

changes, identify airflow bottlenecks, and pre-test efficiency configurations,

removing the risk of localized system strains and reducing total energy waste.

What factors are accelerating the adoption of ductless

HVAC systems in commercial retrofits?

Ductless options, such as VRF mini-splits, bypass the need

for extensive, space-consuming structural ductwork installation within older

buildings. They provide highly pinpointed, single-room zoning capabilities,

require lower installation labor, and eliminate the systemic convective thermal

losses frequently associated with traditional duct pathways.

Browse More Reports:

About Us

Business Market Insights is a market research platform that

provides subscription service for industry and company reports. Our research

team has extensive professional expertise in domains such as Electronics &

Semiconductor; Aerospace & Defense; Automotive & Transportation; Energy

& Power; Healthcare; Manufacturing & Construction; Food &

Beverages; Chemicals & Materials; and Technology, Media, &

Telecommunications.

Contact Us

If you have any questions about this report or would like

further information, please contact us:

Contact person: Ankit Mathur

Email: sales@businessmarketinsights.com

Phone: +16467917070

Comments

Post a Comment