Interventional Neurology Market Future Outlook and 7.22% CAGR Trends

The Interventional Neurology Industry is undergoing accelerated development globally, supported by the rising incidence of stroke and neurovascular disorders, increasing establishment of comprehensive stroke centers, and growing demand for minimally invasive treatment solutions. Advanced endovascular technologies are playing a critical role in improving procedural precision and patient recovery outcomes.

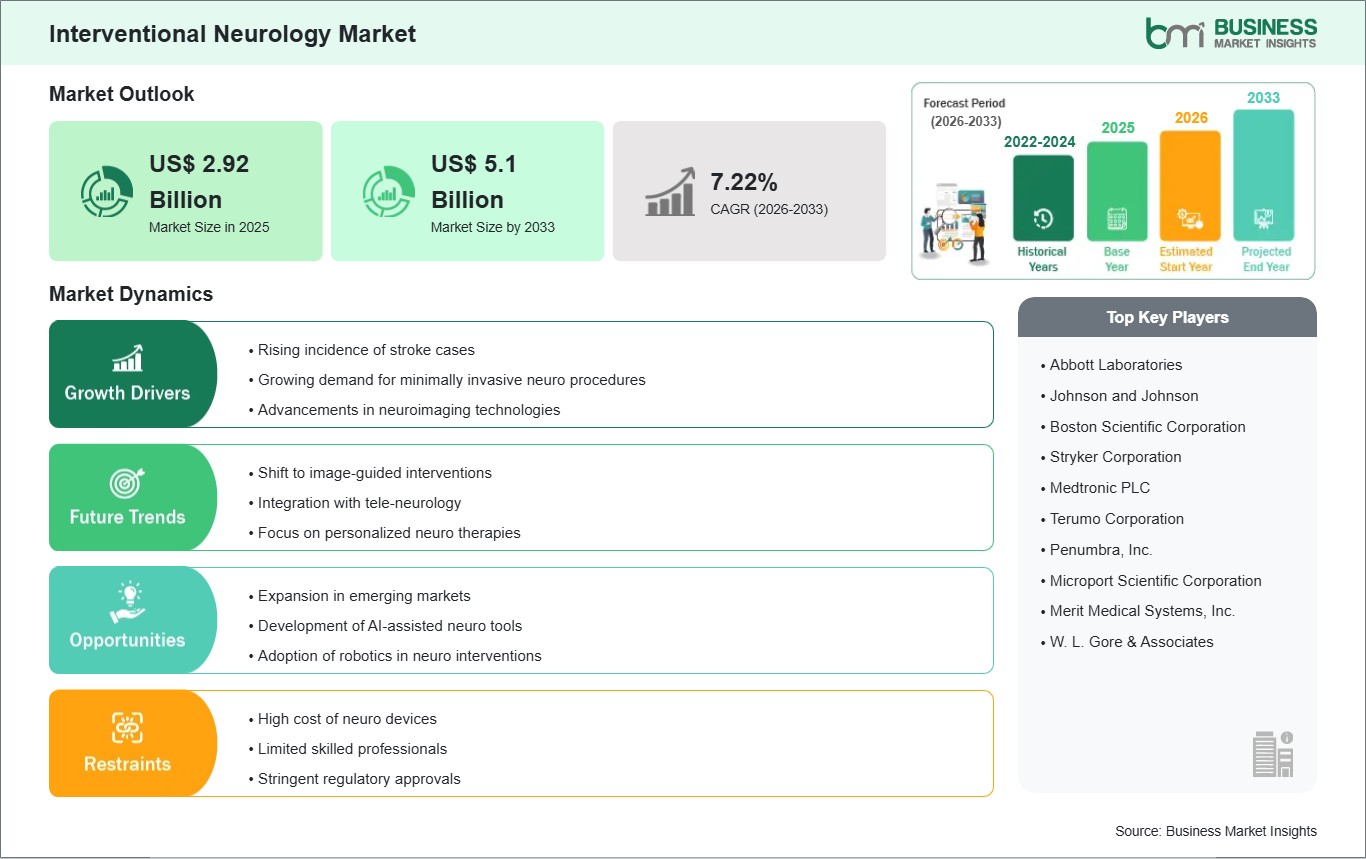

As per Business Market Insights, the global Interventional

Neurology Market is expected to increase from US$ 2.92 billion in

2025 to US$ 5.1 billion by 2033. This growth reflects a projected CAGR of 7.22%

throughout the forecast period of 2026–2033.

Advancements in microcatheter trackability, bioresorbable

flow-diverter meshes, and AI-powered real-time clot detection imaging software

are fundamentally transforming the competitive environment. Leading medical

engineering firms and specialized neuro-radiological laboratories are

prioritizing the refinement of steerable microguidewires and high-volume

aspiration systems to maximize clot clearance efficiency and significantly

expand the therapeutic window for acute stroke interventions.

What Is Interventional Neurology?

Interventional neurology also known as endovascular surgical

neuroradiology is a highly specialized medical subspecialty that utilizes

minimally invasive, image-guided techniques to diagnose and treat

life-threatening vascular diseases of the central nervous system, brain, and

spinal cord. Operating within advanced hybrid angiography suites,

neurointerventionalists utilize high-resolution fluoroscopic imaging to guide

ultra-thin, flexible microcatheters through the femoral or radial artery

directly into the cerebral vasculature.

The primary biophysical objective of these procedures is to

either restore cerebral blood flow or safely isolate vascular defects from

normal circulation. This is achieved through mechanical thrombectomy

(physically extracting obstructive blood clots using stent retrievers or

aspiration pumps), endovascular coiling (packing aneurysms with detachable

embolic coils to induce localized thrombosis), or intracranial stenting to

remodel narrowed arterial walls. By avoiding the trauma of a classic open

craniotomy, these techniques provide exceptional precision, dramatically lower

post-operative infection rates, and accelerate functional patient recovery.

Download Sample Report: https://www.businessmarketinsights.com/sample/BMIPUB00032570

Market Drivers

A primary driver accelerating the global Interventional

Neurology Industry is the Escalating Worldwide Burden of Cerebrovascular

Diseases and Acute Ischemic Strokes. Shifting global demographic patterns,

aging populations, and the rising prevalence of metabolic risk factors such as

hypertension, hyperlipidemia, and diabetes have led to a continuous influx of

stroke patients requiring emergency medical interventions. Because mechanical

thrombectomy has become the clinical standard of care for large vessel occlusions,

institutional demand for high-performance clot-retrieval devices and large-bore

aspiration catheters remains highly robust and non-cyclical.

The rapid institutional pivot toward Minimally Invasive

Endovascular Care serves as another vital market driver. Modern healthcare

systems are actively optimizing operational efficiencies by shortening

intensive care unit (ICU) lengths of stay and reducing long-term disability

rehabilitation costs. Compared to conventional open neurosurgery, endovascular

interventions drastically minimize systemic tissue trauma and lower

complication rates, prompting hospital procurement departments to aggressively

allocate capital budgets toward upgrading interventional suites and securing

advanced neurovascular support devices.

Additionally, breakthrough innovations in Steerable

Micro-Access Technologies and Hydrophilic Coatings act as major volume drivers.

Historically, navigating the highly tortuous and delicate blood vessels of the

brain posed severe risks of arterial perforation or vasospasm. The

commercialization of nitinol-based, shape-memory microguidewires paired with

advanced friction-reducing hydrophilic coatings enables specialists to safely

traverse complex intracranial loops, expanding the eligible patient pool to include

those with deep-seated or previously inaccessible neurovascular anomalies.

Market Segmentation

By Product Type

- Aneurysm

Coiling and Embolization Devices (Including Bare Detachable Coils, Coated

Detachable Coils, Flow Diversion Devices, and Liquid Embolics)

- Neurothrombectomy

Devices (Clot Retrievers/Stent Retrievers, Suction/Aspiration Devices, and

Surgical Snares)

- Cerebral

Balloon Angioplasty and Stenting Systems (Carotid Artery Stents,

Intracranial Stents, and Balloon Catheters)

- Support

Devices (Microcatheters, Microguidewires, and Guidance Access Sheaths)

By Application

- Ischemic

Strokes

- Brain

Aneurysms

- Artery

Stenosis

- Vein

Stenosis

- Others

By End User

- Hospitals

& Specialized Clinics (The foundational and highest-volume care

setting for endovascular surgeries)

- Ambulatory

Surgical Centers (ASCs)

- Dedicated

Stroke Treatment and Diagnostic Centers

The Aneurysm Coiling and Embolization Devices segment

commanded a major share of the global market matrix in 2024, supported by the

steady volume of prophylactic interventions aimed at preventing hemorrhagic

ruptures in unruptured intracranial aneurysms. Concurrently, the

Neurothrombectomy Devices vertical is registering the fastest segment-specific

compound growth, driven by mandatory global stroke management protocols that

mandate immediate mechanical clot retrieval for large vessel occlusions.

Get More Insights: https://www.businessmarketinsights.com/buy/BMIPUB00032570

Regional Insights

- North

America commands the premier share of the global interventional

neurology market, sustained by an exceptionally mature digital healthcare

infrastructure, high healthcare spending per capita, and an extensive

network of specialized, comprehensive stroke centers across the United

States and Canada. Growth is further propelled by early clinical adoption

of premium FDA-approved intrasaccular devices and robust reimbursement

frameworks covering endovascular thrombectomies.

- Europe maintains

a highly stable, premium market presence, governed by the stringent

compliance standards of the European Medical Device Regulation (MDR).

Regional market growth is heavily supported by widespread public health

initiatives aimed at optimizing acute stroke triage times and extensive

clinical trial registries validating the long-term efficacy of local

neurovascular stent technologies.

- Asia-Pacific represents

the fastest-growing regional market over the forecast timeline, driven by

extensive state-backed hospital modernization initiatives across China and

India, expanding private multi-specialty healthcare networks, and a

rapidly aging demographic highly susceptible to cerebrovascular events.

- Rest

of the World (Middle East & Africa and South America) is

exhibiting steady incremental volume expansion, fueled by targeted

public-private investments to establish advanced angiography hybrid suites

in major urban hubs like Dubai and São Paulo, alongside rising regional

clinical training initiatives for endovascular specialists.

Top Players in the Interventional Neurology Industry

The competitive marketplace features a moderately

consolidated ecosystem of multi-national medical engineering giants and

specialized med-tech developers continuously expanding their geographical

footprints through advanced micro-braiding patents and strategic clinic

training networks.

- Medtronic

plc

- Stryker

Corporation

- Johnson

& Johnson Services, Inc. (DePuy Synthes)

- Terumo

Corporation

- Penumbra,

Inc.

- MicroPort

Scientific Corporation

- Asahi

Intecc Co., Ltd.

- Integer

Holdings Corporation

Technological Innovations

The clinical integration of Artificial Intelligence (AI) and

Automated Stroke Triage Telemetry is radically modernizing interventional

workflow efficiency. Historically, the time elapsed between a patient's arrival

and the initiation of mechanical thrombectomy ("door-to-puncture

time") was hindered by manual image interpretation delays. Next-generation

platforms leverage machine-learning algorithms to instantly analyze CT

angiograms or perfusion maps, auto-detecting large vessel occlusions within

seconds and streaming automated alerts directly to the neurointerventionalist’s

mobile device, ensuring immediate preparation of the angio suite and maximizing

brain tissue salvage.

Concurrently, the development of Advanced Intrasaccular

Aneurysm Disruption Systems represents a massive technological leap in managing

wide-necked bifurcated aneurysms. While traditional coiling techniques often

require the concurrent placement of permanent intracranial stents or balloons

to keep coils within the aneurysm sac, next-generation intrasaccular implants

feature self-expanding, highly dense nitinol mesh structures. Placed directly

inside the aneurysm body, these devices instantly disrupt internal blood flow

and create a stable scaffold for endothelial remodeling across the neck,

eliminating the need for long-term dual antiplatelet therapy and significantly

reducing procedural risks.

Future Market Outlook

The future trajectory for the Interventional Neurology

Market remains exceptionally positive. As global clinical guidelines

continuously emphasize rapid, minimally invasive endovascular intervention over

conservative pharmaceutical management for acute cerebrovascular events, the

global utilization of dedicated micro-access systems will steadily scale,

transforming standard emergency stroke response protocols.

Future research and development capital will be highly

concentrated in the commercialization of remote robotic-assisted neurovascular

intervention platforms to allow off-site specialists to perform

micro-catheterization via telestroke frameworks, the synthesis of bioresorbable

intracranial stents that safely degrade after structural arterial remodeling is

complete, and the integration of optical coherence tomography (OCT) sensors

directly onto microcatheter tips for real-time, high-resolution intravascular tissue

mapping. Organizations that successfully deliver highly flexible,

multi-compatible platforms maximizing recanalization rates while maintaining

superior safety profiles will comfortably secure long-term global market

dominance.

Frequently Asked Questions (FAQs)

What product type currently dominates the global

interventional neurology market?

The Aneurysm Coiling and Embolization Devices segment held

the leading market share in 2024, driven by the expanding clinical volume of

preventative endovascular treatments for intracranial aneurysms and the

commercial availability of high-density detachable microcoils.

Why is the neurothrombectomy devices segment exhibiting

the fastest compound growth?

This segment is expanding rapidly due to updated global

clinical guidelines declaring mechanical thrombectomy as the gold-standard

front-line intervention for acute ischemic strokes involving large vessel

occlusions, which has exponentially boosted hospital procurement volumes for

stent retrievers and aspiration systems.

How do advanced hydrophilic coatings improve the safety

of neurointerventional support devices?

Hydrophilic coatings drastically reduce surface friction

when microcatheters and microguidewires contact sensitive vascular walls. This

allows interventionalists to smoothly navigate highly tortuous intracranial

pathways, mitigating the risks of accidental arterial vasospasms or

perforations.

What major advantage do intrasaccular disruption devices

offer over classic embolic coiling?

Intrasaccular disruption devices utilize a single braided

mesh structure that fills the aneurysm neck to instantly divert blood flow,

eliminating the need to pack multiple individual coils or deploy adjunctive

intracranial stents, thereby shortening procedure times and minimizing the

long-term need for complex antiplatelet medications.

Browse More Reports:

Western Europe Laparoscopic Energy Systems Market

ASEAN Laparoscopic Insufflation Devices Market

Latin America Laparoscopic Suction Devices Market

About Us

Business Market Insights is a market research platform that

provides subscription service for industry and company reports. Our research

team has extensive professional expertise in domains such as Electronics &

Semiconductor; Aerospace & Defense; Automotive & Transportation; Energy

& Power; Healthcare; Manufacturing & Construction; Food &

Beverages; Chemicals & Materials; and Technology, Media, &

Telecommunications.

Contact Us

If you have any questions about this report or would like

further information, please contact us:

Contact person: Ankit Mathur

Email: sales@businessmarketinsights.com

Phone: +16467917070

Comments

Post a Comment