Mega Data Center Market Future Outlook and 5.25% CAGR Trends

Rapid advancements in artificial intelligence, cloud computing, and big data analytics are transforming the Mega Data Center Industry across global markets. The increasing need for hyperscale infrastructure, enhanced storage capacity, and real-time processing of massive datasets continues to drive market growth and technological innovation.

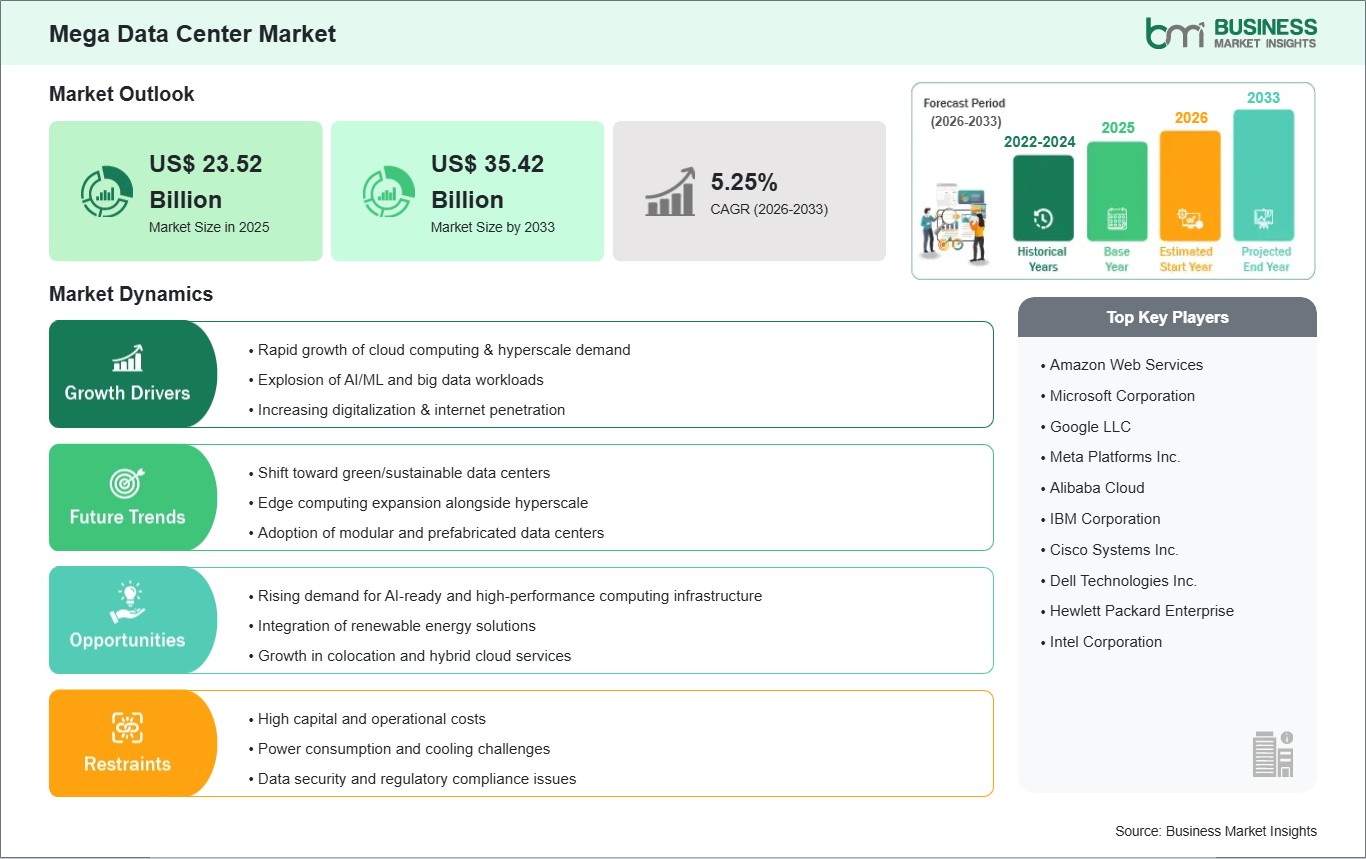

According to Business Market Insights, the global Mega

Data Center Market was valued at US$ 23.52 billion in 2025 and is forecast

to reach US$ 35.42 billion by 2033. The market is projected to expand at a CAGR

of 5.25% between 2026 and 2033.

Advancements in direct-to-chip liquid cooling, the

integration of on-site renewable energy generation, and the deployment of

purpose-built AI server clusters are fundamentally reshaping the competitive

landscape. Global hyperscale operators and colocation providers are heavily

prioritizing sustainable infrastructure, optimized Power Usage Effectiveness

(PUE) metrics, and robust zero-trust security frameworks to manage immense IT

loads while complying with increasingly stringent regional energy efficiency mandates

and zoning reforms.

What Are Mega Data Centers?

Mega data centers are colossal, highly engineered

centralized facilities specifically designed to house tens of thousands of

servers alongside massive arrays of storage and networking equipment. Unlike

traditional on-premise enterprise data centers, these hyperscale environments

typically span hundreds of thousands of square feet and are built from the

ground up to handle immense volumes of digital information. Their primary

technical objective is to deliver extreme scalability, robust fault tolerance, and

massive computing power to support global internet infrastructure.

These facilities serve as the foundational backbone for

major cloud service providers, large-scale content delivery networks (CDNs),

and global social media platforms. By concentrating infrastructure on a massive

scale, operators achieve profound economies of scale, allowing them to deploy

custom-designed server racks, highly efficient power distribution hubs, and

advanced cooling topologies that drastically reduce the overall cost of compute

per kilowatt-hour.

Download Sample Report: https://www.businessmarketinsights.com/sample/BMIPUB00035104

Market Drivers

A primary catalyst pushing the Mega Data Center Industry is

the accelerating integration of Artificial Intelligence (AI) and Machine

Learning (ML) workloads. Generative AI, predictive analytics, and large

language model (LLM) training require incredibly high-performance computing

(HPC) infrastructure. The deployment of power-dense GPU clusters generates

localized rack power requirements frequently approaching or exceeding 100kW,

making purpose-built mega facilities the only environments capable of structurally

and thermally supporting these next-generation applications.

The continuous migration of enterprise operations to public

and hybrid cloud models serves as another vital market driver. As businesses

globally decommission legacy in-house server rooms to reduce capital

expenditures, they rely entirely on hyperscale cloud providers. This structural

shift necessitates the continuous construction of mega data centers to

guarantee uninterrupted global service availability, low-latency disaster

recovery, and seamless cross-border data replication.

Furthermore, the global proliferation of 5G

telecommunication networks and Internet of Things (IoT) devices is generating

unprecedented surges in daily data traffic. Supporting seamless 4K video

streaming, autonomous vehicle telemetry, and smart city grid management

requires centralized data hubs that feature extreme high-bandwidth optical

networking and massive storage density to act as the primary aggregation points

for decentralized edge computing nodes.

Market Segmentation

By Component

- IT

Infrastructure Solutions (Servers, Storage, Networking)

- Power

Management Solutions (UPS, Generators, PDUs)

- Cooling

Solutions (Air-Based, Liquid-Based, Immersion)

- Security

& Management Software

- Professional

& Managed Services

By Data Center Type

- Hyperscale

Self-Build

- Hyperscale

Colocation

By End-User

- Cloud

Service Providers (CSPs)

- Colocation

Providers

- Large

Enterprises (BFSI, Telecom & IT, Media & Entertainment)

- Government

& Public Sector

The IT infrastructure segment accounts for the majority of

market revenue, driven by the relentless procurement cycles for high-end AI

servers and high-speed optical switches. However, the cooling solutions segment

specifically liquid-based and immersion cooling represents the fastest-growing

technology division. This surge is dictated by the thermal limits of

traditional air-cooling architectures, which are no longer sufficient to

dissipate the intense heat generated by modern AI and supercomputing processors.

Regional Insights

- North

America commands an undisputed dominance in the global mega data

center market, anchored by heavy concentrations of top-tier hyperscale

operators across major hubs like Northern Virginia, Texas, and Silicon

Valley, alongside aggressive investments in AI-ready infrastructure.

- Asia-Pacific registers

the fastest compound annual growth rate over the projected forecast

horizon, powered by massive internet penetration, state-led digital

transformation initiatives, and enormous cloud infrastructure investments

unfolding rapidly across China, India, and Southeast Asia.

- Europe maintains

a highly substantial, high-value market footprint, strictly governed by

stringent data sovereignty laws (such as GDPR) that mandate localized data

storage. European operators are pioneering the shift toward sustainable

facilities, utilizing renewable energy purchase agreements and harnessing

excess server heat for local district heating.

- Middle

East & Africa and South & Central America are

demonstrating strong incremental capacity growth, led by strategic smart

city blueprints, expanding regional internet exchanges, and growing

enterprise cloud adoption in nations like the UAE, Saudi Arabia, and

Brazil.

Top Players in the Mega Data Center Industry

The competitive marketplace is characterized by massive

capital expenditures, fierce competition for prime land and grid access, and

deep strategic partnerships between hardware vendors and commercial

hyperscalers.

- Dell

Technologies Inc.

- Hewlett

Packard Enterprise (HPE)

- Cisco

Systems, Inc.

- Intel

Corporation

- NVIDIA

Corporation

- Schneider

Electric SE

- Equinix,

Inc.

- Digital

Realty Trust, Inc.

- Fujitsu

Limited

- Juniper

Networks, Inc.

Technological Innovations

The structural integration of direct-to-chip liquid cooling

and fully submerged immersion cooling is fundamentally altering thermal

management paradigms. By capturing heat directly at the silicon level using

dielectric fluids, operators can radically compress server footprints,

eliminate power-hungry traditional CRAH (Computer Room Air Handler) units, and

dramatically enhance overall compute efficiency without violating local energy

consumption caps.

Concurrently, the energy generation landscape surrounding

mega data centers is pivoting rapidly. Given the immense strain these

facilities place on local utility grids, operators are transitioning beyond

standard solar and wind agreements. Pioneers in the space are actively

exploring grid-independent operations, investing in massive Battery Energy

Storage Systems (BESS), advanced hydrogen fuel cells, and evaluating the

long-term feasibility of localized Small Modular Reactors (SMRs) to guarantee

continuous, zero-carbon baseload power.

Finally, the deployment of Artificial Intelligence for IT

Operations (AIOps) is transforming facility management. Software-defined data

centers now utilize machine learning algorithms to actively monitor millions of

telemetry points across the server floor. This AI layer predicts hardware

failures, automatically throttles non-essential workloads during peak power

grid pricing, and continuously optimizes cooling valve outputs in real time,

drastically reducing human operational intervention.

Future Market Outlook

The future outlook for the Mega Data Center Industry remains

exceptionally strong. As the global economy transitions entirely into an

AI-driven, cloud-first framework, these massive facilities will evolve from

mere data storage warehouses into highly intelligent, autonomous digital

factories processing the world's most critical workloads.

Future development will be heavily constrained by power

availability rather than computing demand, forcing operators to prioritize

Tier-2 and secondary markets where grid capacity is more favorable. Market

leaders that successfully execute next-generation liquid cooling architectures,

secure dedicated clean energy pipelines, and deploy sophisticated automated

security networks will firmly secure global infrastructural dominance over the

coming decade.

Frequently Asked Questions (FAQs)

What distinguishes a mega data center from a traditional

enterprise data center?

Scale and architectural design. Mega data centers (often

synonymous with hyperscale facilities) generally house upward of 10,000

servers, cover massive physical footprints, and feature stripped-down,

customized hardware designed exclusively for maximum compute density and

efficiency. Traditional enterprise data centers are smaller, utilize

off-the-shelf commercial hardware, and are primarily designed to support a

single company's internal IT operations.

Why is the transition to liquid cooling becoming

mandatory for new mega facilities?

The rapid adoption of high-performance GPUs for AI training

has pushed rack power densities beyond 50kW, and often closer to 100kW.

Traditional forced-air cooling simply cannot move enough air to physically

dissipate this level of heat without causing thermal throttling. Liquid cooling

whether direct-to-chip or full immersion transfers heat exponentially more

efficiently than air, making it mandatory for next-generation hardware.

How do mega data centers fit into broader corporate

sustainability goals?

Given their immense power requirements, mega data centers

are at the forefront of corporate sustainability efforts. Operators heavily

invest in Power Purchase Agreements (PPAs) for wind and solar energy, utilize

AI to drive their Power Usage Effectiveness (PUE) as close to 1.0 as possible,

and increasingly adopt waterless cooling systems to drastically reduce their

Water Usage Effectiveness (WUE) footprint in drought-prone regions.

What role does edge computing play alongside mega data

centers?

Edge computing and mega data centers operate in a symbiotic

relationship. Edge nodes process time-sensitive, low-latency data (like

autonomous driving reactions) locally, close to the user. The edge network then

funnels the heavy, non-urgent data back to the centralized mega data centers,

which are equipped to handle massive, long-term storage and complex backend

machine learning model training.

Browse More Reports:

Airborne Collision Avoidance System Market

About Us

Business Market Insights is a market research platform that

provides subscription service for industry and company reports. Our research

team has extensive professional expertise in domains such as Electronics &

Semiconductor; Aerospace & Defense; Automotive & Transportation; Energy

& Power; Healthcare; Manufacturing & Construction; Food &

Beverages; Chemicals & Materials; and Technology, Media, &

Telecommunications.

Contact Us

If you have any questions about this report or would like

further information, please contact us:

Contact person: Ankit Mathur

Email: sales@businessmarketinsights.com

Phone: +16467917070

Comments

Post a Comment