Ophthalmic Lasers Market Set for Steady Growth at 6.09% CAGR by 2033

Global advancements in eye care and surgical technologies are driving the evolution of the Ophthalmic Lasers Industry. Key growth factors include the expanding geriatric population, rising burden of age-related ocular disorders, and growing preference for minimally invasive laser-assisted procedures that improve precision, reduce complications, and enhance visual outcomes.

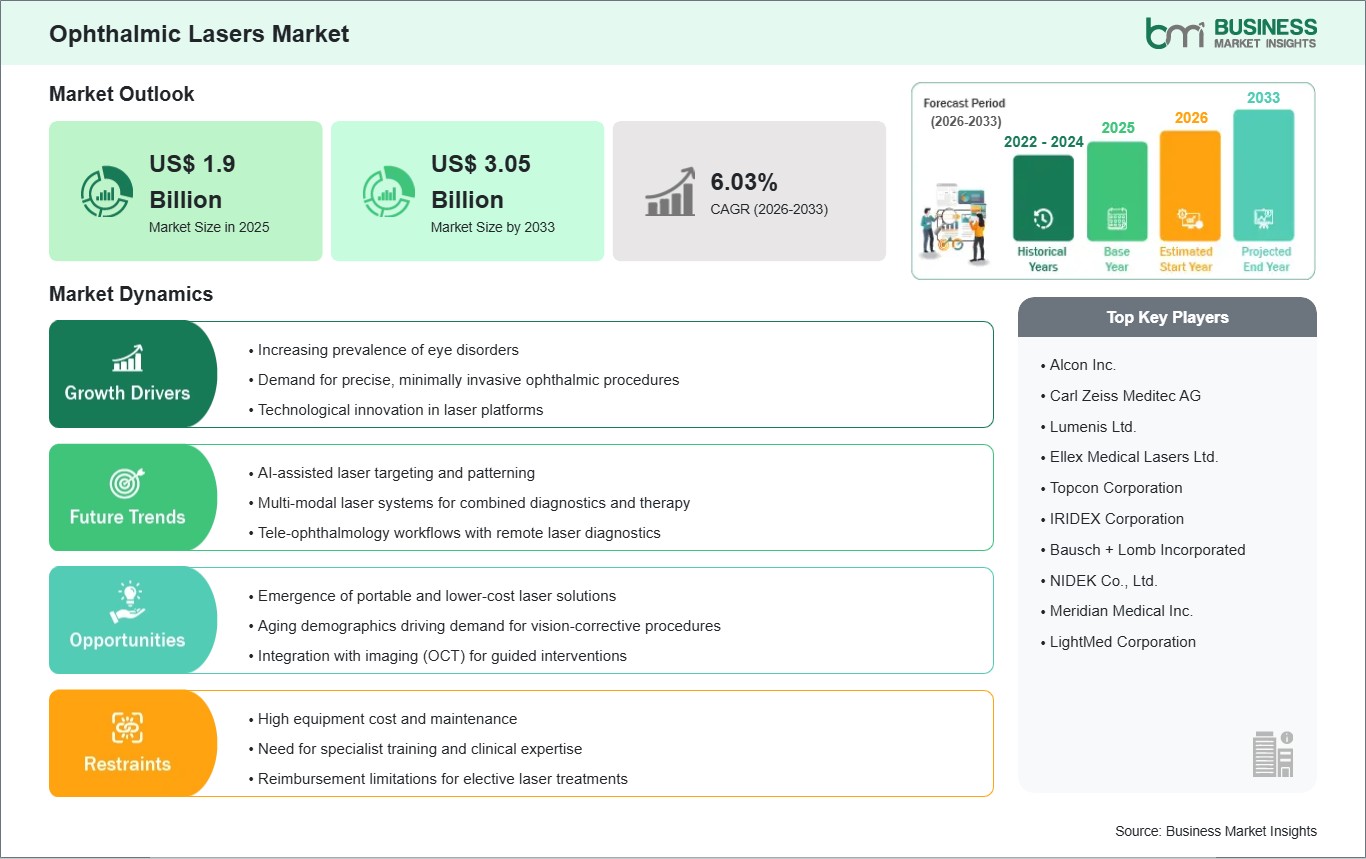

Business Market Insights projects the global Ophthalmic

Lasers Market to grow steadily, reaching US$ 3.05 billion by 2033

from US$ 1.9 billion in 2025. The market is expected to record a CAGR of 6.09%

over the forecast period spanning 2026 to 2033.

Advancements in solid-state laser matrices, intraoperative

optical coherence tomography (OCT) integration, automated tracking algorithms,

and multi-wavelength scanning configurations are rapidly shifting the

competitive environment. Leading medical engineering firms are funneling

substantial capital into optimizing pulse durations down to the femtosecond

level, improving real-time corneal mapping diagnostics, and refining automated

ablation patterns. These innovations are specifically engineered to mitigate

collateral thermal damage to surrounding ocular tissues, eliminate physical

incisional risks, and provide intuitive, customized surgical tracking control

for ophthalmic surgeons managing delicate intraocular structures.

What Is an Ophthalmic Laser?

An ophthalmic laser is a highly engineered medical optical

device designed to emit intense, highly focused beams of coherent monochromatic

light precisely calibrated to interact with specialized structural layers of

the human eye. Far exceeding standard surgical instruments, these platforms

function as non-contact micro-surgical tools capable of cutting, reshaping,

photo-disrupting, or photocoagulating ocular tissues at micron-level

tolerances. They feature advanced structural attributes such as high-definition

slit-lamp delivery optics, digitized multi-axis scanning mirrors, precision

aiming beams, and dynamic thermal management modules engineered to sustain

uniform energy delivery across rapid firing cycles.

These surgical platforms operate across highly distinct

wavelengths and pulse widths to suit specific clinical profiles. Excimer and

Femtosecond lasers operate in the ultraviolet and near-infrared spectrums using

ultra-short pulse delivery to execute non-thermal molecular bond disruptions,

making them highly optimal for precise corneal reshaping in refractive

procedures or creating seamless corneal incisions during cataract surgery.

Conversely, Nd:YAG and Diode laser systems generate specialized photothermal or

photodisruptive energy configurations to create structural openings in the

posterior capsule or perform targeted retinal photocoagulation, allowing

clinical care teams to effectively manage progressive glaucoma and advanced

diabetic retinopathy complications without structural eye trauma.

Download Sample Report: https://www.businessmarketinsights.com/sample/BMIPUB00032661

Market Drivers

A primary driver accelerating the global Ophthalmic Lasers

Industry is the Escalating Global Burden of Chronic Ocular Disorders and

Age-Related Vision Loss. The worldwide population aged 60 years and older is

expanding at an unprecedented rate, naturally correlating with a higher

clinical prevalence of severe cataracts, primary open-angle glaucoma, and

age-related macular degeneration (AMD). Because untreated visual impairment

profoundly restricts independent daily functioning and reduces overall patient

life quality, private medical facilities and public healthcare groups are

systematically investing in high-throughput ophthalmic laser systems to provide

rapid, vision-saving surgical interventions on an expanded scale.

The global surge in Metabolic Syndromes, Type-2 Diabetes,

and Subsequent Diabetic Retinopathy cases represents another core market

driver. Uncontrolled chronic hyperglycemia induces microvascular degradation

within the delicate retinal tissue bed, leading to diabetic retinopathy a

primary cause of preventable blindness among working-age populations. Managing

this expanding patient demographic requires widespread deployment of targeted

pan-retinal photocoagulation therapies. Specialized multi-spot green and yellow

laser systems are heavily procured by clinical networks to systematically seal

leaking retinal capillaries, inhibit abnormal neovascularization, and preserve

structural vision metrics for millions of diabetic patients globally.

Additionally, the paradigm shift toward Minimally Invasive

Elective Procedures and Ambulatory Healthcare Infrastructures acts as a

powerful catalyst. Modern consumers and healthcare payers increasingly reject

conventional mechanical blade-based surgeries due to risks of post-operative

structural infection, prolonged corneal inflammation, and extensive recovery

timelines. Ophthalmic laser platforms optimize surgical workflows by enabling

blade-free, bloodless procedures that achieve exceptional predictability. This

dynamic allows specialized eye clinics and ambulatory surgical centers (ASCs)

to drastically compress operational times, minimize complications, and maximize

daily patient throughput volumes.

Market Segmentation

By Product

- Femtosecond

Lasers (Dominating the technological landscape due to extreme precision in

blade-free cataract surgeries and advanced corneal flaps)

- Excimer

Lasers (Maintaining a strong market footprint tied directly to high-volume

refractive adjustments and surface ablation procedures)

- Diode

Lasers (Widely utilized for targeted retinal photocoagulation therapies

and localized transscleral cyclophotocoagulation)

- Nd:YAG

Lasers (A foundational clinical instrument preferred for posterior

capsulotomy and peripheral iridotomy procedures)

- SLT

Lasers (Expanding steadily as a premier non-invasive first-line

intervention for reducing elevated intraocular pressure in glaucoma)

- Other

Products (Including multi-wavelength gas lasers and emerging solid-state

therapeutic models)

By Application

- Refractive

Error Correction (Leading the commercial revenue matrix driven by massive

elective global demand for LASIK, PRK, and SMILE procedures)

- Cataract

Removal (Experiencing consistent high-volume expansion through

laser-assisted lens fragmentation and capsulorhexis automation)

- Glaucoma

(Tracking a steady upward path via non-invasive trabeculoplasty treatments

to optimize aqueous humor outflow)

- Diabetic

Retinopathy (Demanding consistent therapeutic procurement to address

progressive microvascular retinal damage)

- Age-related

Macular Degeneration (Utilizing specialized photodynamic laser therapies

to limit subretinal vascular leakage)

- Other

Applications (Encompassing localized ocular oncology treatments and

specialized vitreoretinal membrane alterations)

By End-User

- Outpatient

Facilities (The dominant revenue-generating end-user segment, powered by

the rapid proliferation of specialized ambulatory surgical centers and

private eye clinics)

- Inpatient

Facilities (Utilizing heavy-duty, multi-platform laser installations

within major public hospitals and academic medical institutions)

Regional Insights

- North

America holds the premier position in the global landscape,

securing a commanding revenue share. This market dominance is anchored by

high per-capita healthcare expenditure, comprehensive medical insurance

coverage frameworks that accommodate advanced laser optics, and a rapid

clinical adoption rate for newly approved premium solid-state

configurations across the United States and Canada.

- Europe exhibits

a highly regulated, substantial market presence, heavily supported by

well-funded public health networks and progressive universal diagnostic

screening frameworks across Germany, the UK, and France. European eye

clinics prioritize strict CE-marked ergonomic certifications and

integrated diagnostic pairings to optimize patient safety and clinical

outcome trackability.

- Asia-Pacific represents

the fastest-growing geographic block, recording an exceptional forward

growth path. This rapid expansion is propelled by massive healthcare

modernization campaigns, expanding public medical access, a high regional

baseline of myopia, and aggressive investments in specialized eye

hospitals across China, India, and Japan.

- Rest

of the World (Middle East & Africa and South America) is

displaying steady, progressive growth patterns, driven by the targeted

modernization of private specialty hospitals, expanding urban clinic

networks, and public-private healthcare initiatives designed to scale up

regional eye care capabilities.

Top Players in the Industry

The competitive ecosystem displays a focused framework, with

specialized medical optics conglomerates and high-tech laser engineering firms

maintaining clear leadership through long-term group purchasing organization

(GPO) contracts and extensive technical patents.

- Alcon

Inc.

- Carl

Zeiss Meditec AG

- Lumenis

Be Ltd.

- NIDEK

Co., Ltd.

- IRIDEX

Corporation

- Topcon

Corporation

- Lumibird

Group (Quantel Medical)

- Ellex

Medical Lasers

- Bausch

+ Lomb Corporation

- Ziemer

Ophthalmic Systems AG

Technological Innovations

The integration of Intraoperative Optical Coherence

Tomography (OCT) Guided Navigation represents a monumental structural

breakthrough for ophthalmic laser platforms. Historically, surgeons relied on

pre-operative static diagnostic images to map out surgical plans, which could

introduce alignment variances due to subtle patient movement or eye positioning

shifts on the operating table. Next-generation ophthalmic lasers combine

real-time cross-sectional OCT visualization directly into the laser delivery system.

This allows the laser to automatically adjust its focus and depth parameters

mid-procedure, ensuring micron-level ablation accuracy through changing corneal

structures and providing a level of safety and precision previously unavailable

in conventional mechanical techniques.

Concurrently, the transition toward Intelligent AI-Driven

Ablation Profiling and Automated Eye Tracking Systems is completely modernizing

the refractive sector. Next-generation excimer and femtosecond setups

incorporate sophisticated high-speed camera arrays that monitor involuntary

micro-saccadic eye movements thousands of times per second. If the patient's

eye shifts even a fraction of a millimeter, the integrated machine learning

algorithms instantly recalculate the laser path or pause energy delivery dynamically.

This eliminates the risk of decentered ablations, reduces surgical human error

factors, and delivers highly customized treatment paths tailored to the unique

topography of each patient's eye.

Future Market Outlook

The long-term trajectory for the Ophthalmic Lasers Market

remains exceptionally strong. As international healthcare guidelines

permanently establish minimally invasive optical intervention as a core metric

of clinical excellence and global demographic trends continue to expand the

baseline population requiring precise vision preservation, the universal demand

for both therapeutic and corrective laser systems will scale continuously,

defining point-of-care efficiency protocols.

Future research and development capital will be heavily

directed toward the commercialization of ultra-compact, multi-wavelength mobile

laser modules that facilitate remote clinical delivery, the integration of

advanced robotic-assisted alignment arms to optimize surgical docking

procedures, and the expansion of smart, non-thermal photo-disruptive solutions

for pre-presbyopic lens treatments. Equipment developers that successfully

balance premium real-time diagnostic integration with competitive, compact structural

profiles will comfortably secure long-term global market leadership.

Frequently Asked Questions (FAQs)

What product category currently commands the dominant

position in the global ophthalmic lasers market?

The Femtosecond Lasers segment holds the leading revenue and

technology share, driven by their unmatched micro-level incision accuracy,

non-thermal cutting mechanics, and ubiquitous deployment across advanced

cataract extractions and blade-free LASIK surgeries globally.

Why are outpatient facilities experiencing the fastest

procurement growth for ophthalmic lasers?

Outpatient facilities, such as ambulatory surgical centers

(ASCs), are leading procurement because ophthalmic laser procedures are highly

efficient, require zero overnight stays, and feature rapid patient recovery

profiles, making them perfectly suited for high-volume, same-day specialty

clinic workflows.

How does intraoperative OCT integration enhance patient

safety during laser procedures?

Intraoperative OCT integration provides the surgeon with

continuous, real-time cross-sectional visualizations of ocular tissue layers

during the actual procedure. This allows the laser platform to dynamically

verify structural depth, preventing accidental tissue over-penetration and

maximizing alignment safety.

Which geographic territory is recording the fastest

compound growth rate for ophthalmic solutions?

The Asia-Pacific region is tracking the fastest projected

compound annual growth rate (CAGR), propelled by massive healthcare

infrastructure modernizations, escalating regional myopia rates among younger

demographics, rising disposable income, and expanding medical tourism networks.

Browse More Reports:

Middle East and Africa Veterinary Computed Tomography (CT)

Scanners Market

About Us

Business Market Insights is a market research platform that

provides subscription service for industry and company reports. Our research

team has extensive professional expertise in domains such as Electronics &

Semiconductor; Aerospace & Defense; Automotive & Transportation; Energy

& Power; Healthcare; Manufacturing & Construction; Food &

Beverages; Chemicals & Materials; and Technology, Media, &

Telecommunications.

Contact Us

If you have any questions about this report or would like

further information, please contact us:

Contact person: Ankit Mathur

Email: sales@businessmarketinsights.com

Phone: +16467917070

Comments

Post a Comment