Power Electronics Market Investment Opportunities Amid 6.32% CAGR Growth

Technological innovation is

transforming the global Power Electronics Industry, with manufacturers

increasingly adopting advanced semiconductor materials such as silicon carbide

(SiC) and gallium nitride (GaN) to improve energy efficiency and performance.

These technologies are enabling more effective power control and conversion

across automotive, industrial, consumer electronics, and energy infrastructure

applications.

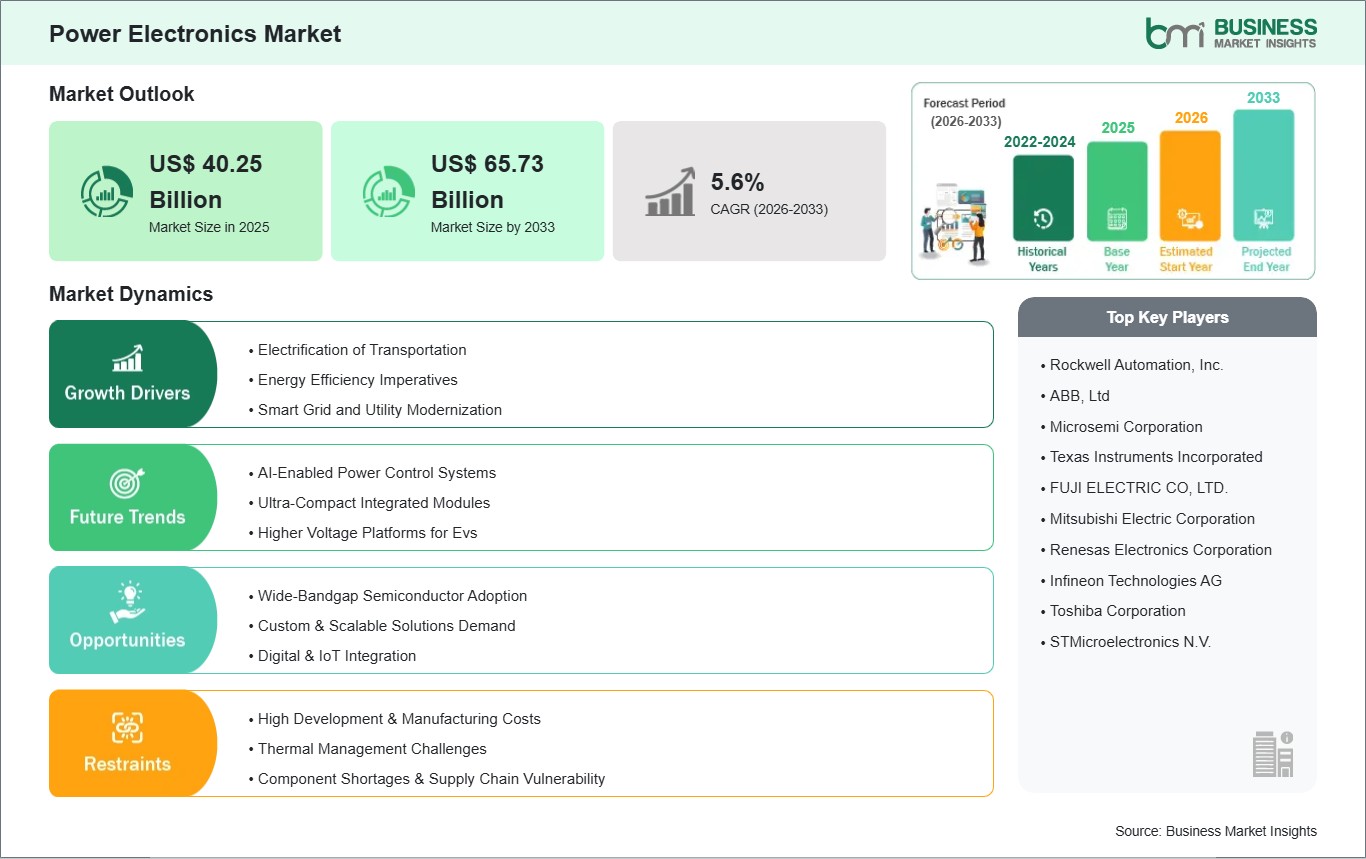

According to Business Market

Insights, the global Power

Electronics Market was valued at US$ 40.25 billion in 2025 and is

anticipated to reach US$ 65.73 billion by 2033. The market is projected to grow

at a CAGR of 6.32% during the forecast period from 2026 to 2033.

Advancements in wide-bandgap (WBG)

substrate materials like Silicon Carbide (SiC) and Gallium Nitride (GaN),

intelligent power modules (IPMs), high-density MOSFETs, Insulated-Gate Bipolar

Transistors (IGBTs), and advanced 3D packaging technologies are rapidly

shifting the competitive environment. Leading electronic component developers

are funneling substantial capital into consolidating individual switching

components into compact modular arrays, introducing intelligent gate-driver

features, and embedding automated thermal sensing configurations directly into

discrete setups. These investments are specifically engineered to eliminate

high-power dissipation losses, reduce overall system footprints, and provide an

exceptionally reliable power management grid that seamlessly integrates with

modern electrified powertrains, green power grids, and automated factory

robotics.

What Is Power Electronics?

Power electronics refers to a

highly specialized field of electrical engineering and semiconductor technology

that deals with the conversion and control of electrical energy using

solid-state electronics. Far exceeding traditional stationary transformation

equipment, these modernized devices operate as dynamic, intelligent switches

within interconnected electric networks. They incorporate sophisticated

structural layers such as high-efficiency power ICs, discrete diodes,

thyristors, and transistors that capture raw electrical inputs at the

source and instantly modify their waveform parameters (such as changing AC to

DC, modifying voltage magnitudes, or adjusting frequency boundaries) for

precise application delivery, localized power safety, and system-wide

efficiency optimization.

These advanced energy management

frameworks utilize highly distinct device classifications to handle complex

voltage loads. At the device level, power discrete transistors like

Metal-Oxide-Semiconductor Field-Effect Transistors (MOSFETs) and Insulated-Gate

Bipolar Transistors (IGBTs) act as critical building blocks between energy

generation sources and end-user hardware systems, managing high-frequency

switching cycles and executing current variations smoothly. These digitized

power streams travel safely through tightly packed power modules, which bundle

multiple solid-state components together to handle extreme electrical

capacities, allowing operators to manage intense load dynamics and isolate

thermal faults within microseconds, guaranteeing complete hardware longevity

without localized degradation.

Download Sample Report: https://www.businessmarketinsights.com/sample/BMIPUB00032690

Market Drivers

A primary driver accelerating the

global Power Electronics Industry is the rapid shift toward Electric Mobility

and Vehicle Powertrain Electrification. Conventional internal combustion

engines are being swiftly replaced by battery electric vehicles (EVs) that

demand ultra-efficient power conversion architectures to maximize driving range

and accelerate battery charging intervals. Power electronics address this vital

requirement by establishing high-performance main traction inverters, onboard

chargers (OBCs), and bi-directional DC-DC converters across automotive systems.

The implementation of advanced wide-bandgap materials allows automotive OEMs to

safely implement 800V and 1000V vehicle architectures, cutting structural

thermal loss and delivering exceptionally stable vehicle propulsion systems.

The global push for Renewable

Energy Grid Integration and Smart Infrastructure Efficiency represents another

core market driver. As utility systems worldwide transition toward wind-farm

networks, commercial solar arrays, and utility-scale battery storage

facilities, managing intermittent, decentralized power flows has become

intensely strict. Power electronics utilize high-power converters and

intelligent inverters to dynamically stabilize voltage fluctuations before

transferring green power into main transmission corridors. This limits overall

transmission energy loss, removes structural grid overload risks, and optimizes

capital returns for energy companies running high-throughput distribution

lines.

Additionally, the universal

transition toward Industry 4.0 and High-Efficiency Industrial Automation acts

as a powerful catalyst. To satisfy strict international industrial energy

compliance policies and cut overarching factory operation costs, automated

production facilities are extensively integrating variable-frequency drives

(VFDs), industrial robotic control systems, and localized server power

matrices. Power electronic modules supply the precise current regulation and

extreme fast-switching responses necessary to handle complex, automated robotic

operations, safely insulating sensitive factory automation setups from severe

voltage disruptions.

Market Segmentation

By Device Type

- Power

Discrete (Commanding a massive market share driven by widespread usage in

entry-level consumer appliances, computing accessories, and localized

low-power switching applications)

- Power

Module (Exhibiting high-growth trends as high-power integrators transition

to factory-tested integrated packages that blend gate-drivers and thermal

monitoring layouts for electric vehicles and heavy industrial motor

controllers)

- Power

IC (Expanding steadily due to the ongoing miniaturization of mobile

consumer electronics, wireless communication systems, and smart IoT device

networks requiring compact form-factors)

By Material

- Silicon

(The dominant baseline material segment, preferred for its cost-effective

manufacturing metrics, established global supply chains, and extensive use

across low-frequency, standard-power applications)

- Silicon

Carbide (SiC) (Tracking exponential growth across heavy-duty automotive

inverters and high-voltage energy infrastructures due to its ability to

operate at 10X higher voltage thresholds without excessive cooling

requirements)

- Gallium

Nitride (GaN) (Capturing rapid market momentum within consumer electronics

ultra-fast chargers and telecom RF power amplifiers because of its

superior high-frequency switching capabilities and ultra-compact

structural profile)

By End-User Industry

- Consumer

Electronics (A historically massive volume segment, encompassing

smartphones, smart home appliances, wearable products, and computing

systems focused on energy efficiency)

- Automotive

& Transportation (The fastest-growing vertical segment, heavily

propelled by the global electrification of passenger cars, heavy electric

transport fleets, and rail traction networks)

- Industrial

(Utilizing heavy-duty power electronics to drive variable-frequency

industrial motor drives, automated factory assembly systems, and advanced

robotics arrays)

- Energy

& Power (Capturing significant revenue share driven by state-backed

smart grid updates, utility-scale solar/wind inverters, and bi-directional

battery storage systems)

- ICT

(Information and Communications Technology) (Expanding via high-efficiency

server power supplies, cloud data center infrastructures, and telecom base

station networks requiring reliable operational uptimes)

- Others

(Including medical diagnostic equipment, aerospace power architectures,

and marine defense grid systems requiring custom ruggedized hardware

configurations)

Regional Insights

- Asia-Pacific holds

the premier position in the global landscape, securing a dominant market

share of over 44%. This regional leadership is anchored by massive

consumer electronics assembly ecosystems, the rapid expansion of electric

vehicle manufacturing hubs across China, Japan, and India, and enormous

capital outlays directed toward national smart grid transmission

corridors.

- North

America exhibits a highly robust, technologically advanced market

presence, propelled by extensive automotive electrification lines, heavy

defense infrastructure upgrades, and massive private-sector R&D

investments in next-generation wide-bandgap fabs across the United States

and Canada.

- Europe maintains

a highly structured, substantial market presence, characterized by

aggressive environmental sustainability targets, strict industrial energy

efficiency regulations, and a powerful automotive manufacturing sector

accelerating the shift toward high-efficiency SiC-based powertrain

components.

- Rest

of the World is displaying steady, progressive growth patterns,

driven by ongoing grid electrification programs in the Middle East,

telecommunication infrastructure expansion across Latin American hubs, and

target mining/industrial facility modernization deployments in Africa.

Top Players in the Industry

The competitive ecosystem displays

a sophisticated matrix of diversified semiconductor manufacturers and global

electrical engineering firms executing long-term framework component agreements

with automotive OEMs and industrial automation integrators.

- Infineon

Technologies AG

- STMicroelectronics

N.V.

- Texas

Instruments Incorporated

- ON

Semiconductor Corporation (onsemi)

- Mitsubishi

Electric Corporation

- Fuji

Electric Co., Ltd.

- Toshiba

Electronic Devices & Storage Corporation

- NXP

Semiconductors N.V.

- ROHM

Co., Ltd.

- Renesas

Electronics Corporation

Technological Innovations

The commercial implementation of

advanced Wide-Bandgap (WBG) Silicon Carbide (SiC) and Gallium Nitride (GaN)

structures represents a monumental technological breakthrough for the power

electronics sector. Historically, traditional silicon-based transistors hit a

hard physical limit where handling extreme voltage frequencies resulted in

massive thermal losses, necessitating extensive, heavy aluminum heat sinks and

auxiliary liquid cooling lines. Next-generation WBG semiconductors allow power

devices to switch at significantly higher speeds and withstand extreme

operating temperatures while shrinking overall energy losses by up to 60%. This

structural reduction in component mass lets engineering groups craft lighter,

incredibly compact power converters, completely revolutionizing the design

layout of vehicle powertrains and fast-charging hardware systems.

Concurrently, the integration of

3D Semiconductor Packaging and Intelligent Power Modules (IPMs) is completely

modernizing the operational hardware landscape. Modern high-power

configurations face intense structural space limitations and electromagnetic interference

(EMI) challenges when combining separate discrete elements. To resolve this

bottleneck, leading component firms are stacking gate-drivers, current sensors,

and power transistors directly on top of each other using advanced

silver-sintering and direct copper bonding methods. These integrated modules

utilize localized machine learning algorithms at the edge to continuously

monitor internal device temperature and dynamically adjust switching

thresholds, guaranteeing bulletproof protection against electrical overstress

without adding bulk to the final package design.

Future Market Outlook

The long-term trajectory for the

Power Electronics Market remains exceptionally robust. As national regulatory

frameworks permanently establish stringent energy conservation standards across

heavy industries and international electric vehicle infrastructures scale out

globally, the universal reliance on power electronic architectures will expand

continuously, defining core operational efficiency protocols across all major

technology platforms.

Future research and development

capital will be heavily directed toward the commercialization of large-scale

300 mm wide-bandgap wafer manufacturing lines to cut down module fabrication

expenses, the implementation of advanced gallium oxide alternative substrates

to target ultra-high-voltage utility transmissions, and the deployment of

smart, self-healing diagnostic software layers. Hardware developers that

successfully balance premium wide-bandgap product availability with highly

competitive packaging price structures will comfortably secure long-term global

market leadership.

Frequently Asked Questions

(FAQs)

What is the projected valuation

of the global power electronics market by 2034?

The global power electronics

market is projected to reach a valuation of US$ 49.04 Billion by 2034,

expanding significantly from its established baseline value of US$ 27.23

Billion in 2025.

What is the expected compound

annual growth rate (CAGR) of the market over the forecast window?

The market is anticipated to

expand at a steady Compound Annual Growth Rate (CAGR) of 6.84% during the

forecast timeline spanning from 2026 through 2034.

Which regional market segment

commands the dominant revenue share globally?

The Asia-Pacific region holds the

leading market share, capturing over 44% of global revenues due to its

extensive consumer electronics manufacturing ecosystems, aggressive electric

vehicle deployment, and major grid modernization programs.

How do wide-bandgap materials

like SiC and GaN improve power electronics compared to traditional silicon?

Wide-bandgap materials operate

under significantly higher thermal tolerances, support faster switching

frequencies, and substantially reduce electrical conduction losses, allowing

the development of smaller, highly efficient power delivery packages.

Browse More Reports:

Chemical Mechanical Planarization Market

Chip-on-Board Light Emitting Diode (LED) Market

About Us

Business Market Insights is a

market research platform that provides subscription service for industry and

company reports. Our research team has extensive professional expertise in

domains such as Electronics & Semiconductor; Aerospace & Defense;

Automotive & Transportation; Energy & Power; Healthcare; Manufacturing

& Construction; Food & Beverages; Chemicals & Materials; and

Technology, Media, & Telecommunications.

Contact Us

If you have any questions about

this report or would like further information, please contact us:

Contact person: Ankit Mathur

Email: sales@businessmarketinsights.com

Phone: +16467917070

Comments

Post a Comment