Refrigerant Market Projected to Achieve US$ 66.54 Billion by 2033

The Refrigerant Industry is undergoing accelerated evolution globally, supported by expanding refrigeration and air-conditioning infrastructure, rising standards of living, and increasing urbanization in developing regions. At the same time, stricter environmental regulations are encouraging the adoption of next-generation refrigerants with lower environmental impact.

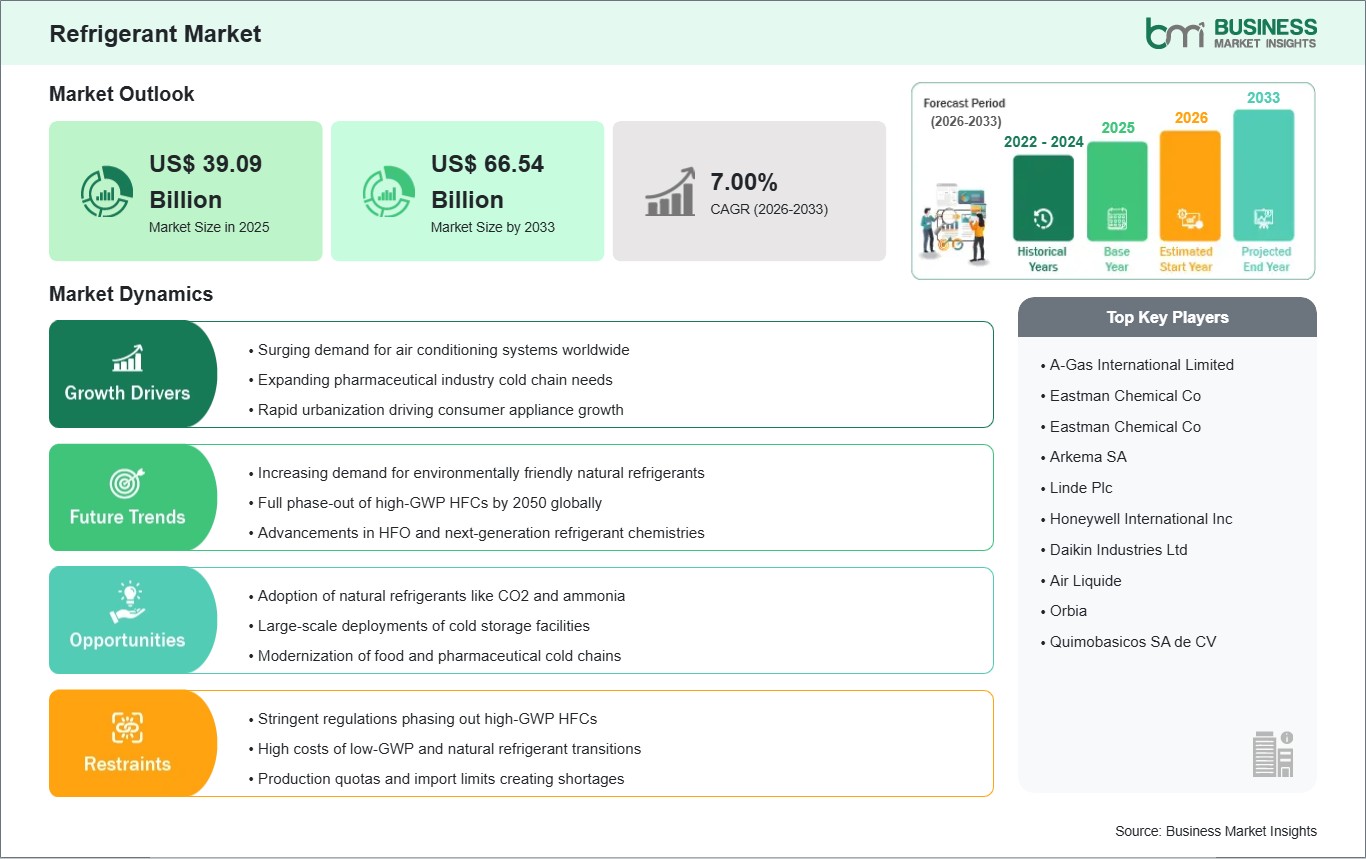

As per Business Market Insights, the global Refrigerant

Market is expected to increase from US$ 39.09 billion in 2025 to US$

66.54 billion by 2033. This growth reflects a projected CAGR of 6.88%

throughout the forecast period of 2026–2033.

Advancements in low-GWP (Global Warming Potential)

compounds, advanced reclamation systems, and commercial deployments of highly

efficient HFO blends are fundamentally reshaping the competitive landscape.

Global chemical enterprises and HVACR equipment manufacturers are prioritizing

strategic production partnerships and capacity expansions to accommodate the

strict phasedown of legacy hydrofluorocarbons (HFCs) while ensuring reliable

thermal management across high-demand industrial and commercial end-uses.

What Is a Refrigerant?

A refrigerant is a specialized chemical compound or working

fluid engineered to absorb heat from one environment and dissipate it into

another through a structured thermodynamic cycle of evaporation and

condensation. Operating inside heating, ventilation, air conditioning, and

refrigeration (HVACR) hardware, these substances undergo continuous phase

transitions alternating between liquid and gaseous states to enable precise

temperature control, climate comfort, food preservation, and industrial

processing operations.

Modern commercial refrigerants are classified into multiple

distinct generations based on their chemical composition and ecological

footprints. While traditional architectures relied heavily on synthetic

fluorocarbons due to their superior safety, non-flammability, and optimal

thermodynamic performance, the modern landscape increasingly integrates natural

alternatives and next-generation synthetic mixtures. These contemporary

formulations are designed to offer high latent heat of vaporization, excellent

thermal conductivity, and chemical stability while minimizing atmospheric

degradation and ensuring mechanical hardware compatibility.

Download Sample Report: https://www.businessmarketinsights.com/sample/BMIPUB00032542

Market Drivers

A primary driver accelerating the global Refrigerant

Industry is the massive Expansion of Cold Chain Infrastructure. The expanding

globalization of food supply networks, combined with an increasing consumer

consumption of packaged and frozen foods, has forced a major upgrade in

temperature-controlled logistics. Industrial processing facilities, cold

storage warehouses, and specialized refrigerated transit fleets are

continuously scaling up, driving huge volume demand for highly dependable,

heavy-duty cooling agents to eliminate food spoilage and optimize supply chain

tracking metrics.

The global shift toward the Adoption of Low-GWP and Natural

Refrigerants serves as another critical market driver. International

environmental frameworks such as the Kigali Amendment to the Montreal Protocol

legally mandate the systematic phasedown of high-GWP hydrofluorocarbons (HFCs)

to mitigate greenhouse gas footprints. This top-down regulatory pressure is

compelling commercial HVAC developers and manufacturing conglomerates to

rapidly convert their existing mechanical designs to utilize eco-friendly alternatives

like carbon dioxide, ammonia, and hydrocarbons to avoid long-term

non-compliance penalties.

Furthermore, rising disposable incomes and rapid

urbanization across emerging economies are continuously boosting the

procurement of residential and commercial appliances. Elevated living

standards, escalating middle-class purchasing power, and a rising frequency of

nuclear family units are stimulating massive sales of domestic refrigerators,

split air conditioners, and automotive mobile air conditioning (MAC) systems.

This expanding global asset base creates an immense, non-cyclical baseline

demand for both initial factory-fill refrigerants and post-sale aftermarket

maintenance servicing volumes.

Market Segmentation

By Type

- HFCs

(Hydrofluorocarbons; dominated the market in 2025 due to established

infrastructure and zero ozone depletion potential)

- HFO

(Hydrofluoroolefins; next-generation synthetic fluids offering ultra-low

GWP profiles)

- Ammonia

(Highly favored in industrial refrigeration due to exceptional

thermodynamic efficiency)

- Carbon

Dioxide (Expanding rapidly in commercial supermarket refrigeration

applications)

- Propane

& Isobutane (Hydrocarbon solutions widely adopted in small-charge

domestic cooling equipment)

- Others

(Including legacy HCFCs undergoing structural phase-outs)

By Application

- Refrigeration

Systems (Domestic, Commercial, and Industrial Cold Storage)

- Air

Conditioning Systems (Residential, Split, and Commercial HVAC Units)

- Chillers

- MACs

(Mobile Air Conditioning Systems for Automotive and Transport Verticals)

- Others

By End Use

- Industrial

(Petrochemicals, Pharmaceutical Storage, and Heavy Food Processing Hubs)

- Commercial

(Supermarkets, Hypermarkets, Hotels, and Corporate Offices)

- Residential

(Household Fridges and Residential Air Conditioning Units)

- Others

The Industrial end-use vertical captured the absolute

largest share of the global market in 2025, driven by the massive cooling

volumes and strict safety requirements necessary inside large-scale chemical

processing plants and pharmaceutical manufacturing lines. Concurrently, the

Refrigeration Systems application segment held the dominant position by volume

and value in 2025, sustained by the explosive development of worldwide

temperature-controlled logistical systems, while the HFCs chemical segment maintained

the largest revenue block due to deep integration with legacy heating and

cooling components.

Regional Insights

- Asia-Pacific commands

the largest and fastest-growing share of the global refrigerant market,

anchored by China's status as the world's leading consumer and producer of

refrigerants due to competitive local manufacturing costs and extensive

export-oriented assembly plants. Growth across the region is further

driven by massive state infrastructure outlays, accelerating urbanization,

and heavy investments in cold-chain logistics across India and Southeast

Asia.

- North

America represents an exceptionally high-value,

specification-driven market footprint. The region is heavily shaped by

strict EPA (Environmental Protection Agency) regulations mandating an

accelerated shift to reclaimed alternatives, driving heavy corporate

investments into high-capacity local separation and reclamation

facilities.

- Europe maintains

a highly stable, premium market presence, strictly regulated by aggressive

European Union F-Gas regulations and mobile air conditioning directives.

These strict legal boundaries compel regional chemical networks and HVAC

original equipment manufacturers to completely transition toward

ultra-low-GWP synthetic blends and natural refrigerant hardware

alternatives.

- Middle

East & Africa and South America are

experiencing steady incremental volume growth, led by expanding commercial

food retail chains, urbanization in cost-sensitive economies, and extreme

regional climatic conditions that necessitate a continuous, non-negotiable

reliance on high-capacity commercial climate control infrastructure.

Top Players in the Refrigerant Industry

The competitive marketplace features a dynamic mix of

diversified international chemical conglomerates, specialized refrigerant

management firms, and prominent industrial gas suppliers operating via

multi-regional distribution networks.

- The

Chemours Company

- Honeywell

International Inc.

- Arkema

SA

- Daikin

Industries, Ltd.

- Dongyue

Group

- AGC

Inc.

- AIR

LIQUIDE SA

- LINDE

plc

- Sinochem

Group Co. Ltd.

- A-Gas

International Limited

Technological Innovations

The commercial rollout of Low-GWP A2L Refrigerants is

fundamentally transforming modern commercial and residential air conditioning

portfolios. Historically, transitioning away from high-GWP HFCs like R-410A

presented significant engineering challenges due to the strict safety balances

required between flammability and operating pressures. Next-generation A2L

alternatives deliver a highly optimized compromise, offering exceptionally low

global warming impacts alongside mild flammability profiles, enabling HVAC

original equipment manufacturers to comfortably satisfy new environmental

metrics without sacrificing cooling capacities.

Concurrently, industry leaders are successfully executing

the Expansion of Refrigerant Reclaiming and Separation Capacities. To comply

with strict national production quotas on virgin chemical blends, specialized

material facilities are deploying advanced fractional distillation and

multi-stage separation architectures. This technical framework allows operators

to collect mixed, contaminated post-use refrigerants, separate them back into

pure chemical components, and re-certify them to factory-grade specifications,

creating a highly sustainable, circular chemical economy that mitigates virgin

carbon tax liabilities.

Future Market Outlook

The future outlook for the Refrigerant Market remains highly

robust. As international industrial sectors commit to zero-emission and

climate-smart operational frameworks, the demand for highly efficient,

sustainable thermal fluids will intensify, shifting from legacy synthetic

chemical bases toward advanced hydrofluoroolefin (HFO) blends and zero-GWP

natural refrigerant architectures.

Future research and development capital will be heavily

concentrated in the optimization of advanced multi-component HFO mixtures

tailored for extreme high-ambient temperatures, the engineering of specialized

synthetic compressor oils that ensure seamless chemical compatibility with

natural refrigerants like carbon dioxide, and the integration of

blockchain-verified molecular tracking to validate the compliance and origin of

reclaimed refrigerant lines. Organizations that successfully secure extensive regional

recycling networks while pioneering safe, hardware-compatible low-GWP chemical

alternatives will seamlessly command long-term global market dominance.

Frequently Asked Questions (FAQs)

What chemical segment currently dominates the global

refrigerant market by type?

The Hydrofluorocarbons (HFCs) segment dominated the global

market landscape in 2025. This leading market position is attributed to their

excellent thermodynamic properties, non-flammable characteristics, high

operational safety profiles, and widespread compatibility with the massive

installed base of legacy residential and commercial HVACR equipment.

Why is the industrial end-use segment experiencing such a

high volume of refrigerant adoption?

The industrial sector demands exceptionally massive and

uninterrupted cooling capacities to support highly complex processes, including

petrochemical refining, pharmaceutical storage, and large-scale food

processing. To comply with tightening international environmental rules like

the Kigali Amendment, these facilities are leading the market in adopting

highly efficient, low-GWP natural refrigerants like ammonia.

What role does expanding cold chain infrastructure play

in driving market growth?

The rapid globalization of food distribution and a

substantial increase in the consumption of frozen and packaged foods have

forced massive investments into temperature-controlled logistics. This

continuous growth in cold storage warehouses, retail supermarkets, and

long-haul refrigerated transport containers directly translates into massive

volume demand for high-performance refrigerants.

How does a commercial partnership like the one between

Arkema and Honeywell impact the industry?

Strategic commercial alliances focused on low-GWP offerings

dramatically strengthen global supply chains. By collaborating on the

development and distribution of advanced Hydrofluoroolefin (HFO) blends, major

players can accelerate the commercial availability of sustainable cooling

alternatives, allowing HVACR operators to seamlessly adjust to ongoing HFC

production phase-outs.

Browse More Reports:

Ceramic Matrix Composites Market

Chlorinated Polyethylene Market

About Us

Business Market Insights is a market research platform that

provides subscription service for industry and company reports. Our research

team has extensive professional expertise in domains such as Electronics &

Semiconductor; Aerospace & Defense; Automotive & Transportation; Energy

& Power; Healthcare; Manufacturing & Construction; Food &

Beverages; Chemicals & Materials; and Technology, Media, &

Telecommunications.

Contact Us

If you have any questions about this report or would like

further information, please contact us:

Contact person: Ankit Mathur

Email: sales@businessmarketinsights.com

Phone: +16467917070

Comments

Post a Comment