Remote Patient Monitoring Market Projected to Achieve US$ 60.14 Billion by 2033

The Remote Patient Monitoring Industry is undergoing accelerated digital transformation, supported by advancements in connected healthcare technologies, growing penetration of mobile and broadband networks, and increasing pressure on healthcare systems to improve efficiency while reducing treatment costs. These factors are fostering widespread adoption of remote care solutions.

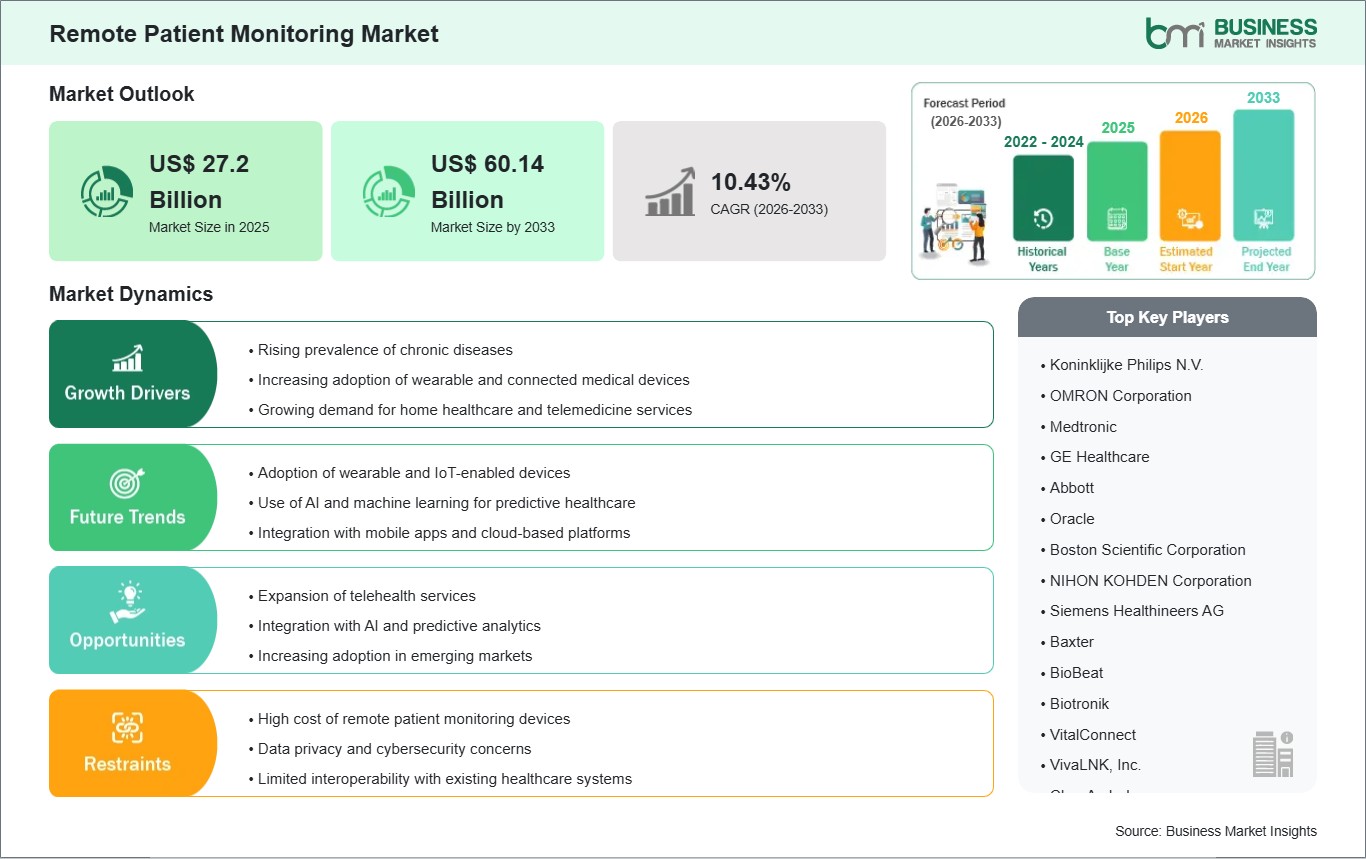

As per Business Market Insights, the global Remote

Patient Monitoring Market is expected to increase from US$ 27.2

billion in 2025 to US$ 60.14 billion by 2033. This growth reflects a projected

CAGR of 10.43% throughout the forecast period of 2026–2033.

Advancements in continuous biosensing arrays,

cloud-integrated diagnostic engines, and decentralized data ecosystems are

fundamentally reshaping the competitive landscape. Global medical technology

conglomerates and healthcare software developers are prioritizing real-time

multiparameter tracking, machine learning behavioral analytics, and

edge-connected alert systems to allow medical professionals to efficiently

manage patient health from within residential settings, preventing unnecessary

hospital readmissions and optimizing inpatient bed capacity.

Download Sample Report: https://www.businessmarketinsights.com/sample/BMIPUB00032514

What Is Remote Patient Monitoring?

Remote Patient Monitoring (RPM) encompasses a comprehensive

framework of connected medical hardware, smart wearable sensors, and

cloud-based software platforms engineered to capture, securely transmit, and

analyze patient physiological telemetry outside of traditional clinical

environments. By establishing a continuous digital link between a patient's

residence and the primary healthcare provider, RPM shifts the medical paradigm

from reactive, episodic treatment to proactive, continuous care management.

Modern RPM architectures integrate a diverse tier of

specialized diagnostic sensors including wireless electrocardiogram (ECG)

patches, digital spirometers, continuous glucose monitors (CGMs), and smart

pulse oximeters. The physiological data collected by these endpoints is

encrypted and routed via local hubs or cellular connections to a centralized

healthcare dashboard. Advanced analytics software parses this stream,

establishing baseline thresholds and instantly triggering localized alerts for

clinical teams if a patient's vital signs deviate into critical zones.

Market Drivers

A primary driver for the Remote Patient Monitoring Industry

is the rapidly expanding global geriatric population. According to data from

the United Nations, the population aged 60 and over is growing at an annual

rate of 3%, creating an immense structural strain on legacy medical facilities.

Elderly individuals present with higher rates of age-related systemic

deterioration and multi-morbidity, making automated, continuous home tracking

an absolute clinical necessity to manage health without overflowing physical

hospital wards.

The rising global prevalence of complex chronic

diseases such as coronary artery disease, Type 2 diabetes, and chronic

obstructive pulmonary disease (COPD) acts as another vital growth vector.

Managing these lifecycle-long conditions requires constant therapeutic

adjustments. RPM tools significantly lower long-term disease management costs

and treatment durations by identifying minor physiological instabilities before

they escalate into acute, expensive medical emergencies requiring intensive care

intervention.

Furthermore, the systemic impact of the COVID-19 pandemic

permanently altered the healthcare regulatory and operational landscape. The

strict necessity to monitor highly infectious patients safely inside

negative-pressure rooms or residential isolation zones forced a massive

acceleration in the procurement of remote vital sign monitors. This operational

shift dismantled historical institutional resistance, paving the way for

streamlined regulatory approvals and robust public insurance reimbursement frameworks

for virtual care pathways globally.

Market Segmentation

By Type

- Devices: (Cardiac

Monitoring Devices, Neurological Monitoring Devices, Respiratory

Monitoring Devices, Multiparameter Monitoring Devices, Blood Glucose

Monitoring Devices, Fetal & Neonatal Monitoring Devices, Weight

Monitoring Devices)

- Software: (Cloud-Based,

On-Premise)

- Services

By Application

- Cardiovascular

Diseases Treatment

- Cancer

Treatment

- Sleep

Disorder Treatment

- Diabetes

Treatment

- Weight

Management & Fitness Monitoring

By End User

- Hospitals

& Clinics

- Ambulatory

Care Centers

- Home

Healthcare Settings

The Devices segment captures a dominant portion of the

overall market volume across major geographies, driven by the continuous demand

for hardware upgrades and the non-negotiable procurement of single-patient

multi-parameter monitors. Concurrently, the hospital and clinical provider

framework represents the largest end-user infrastructure block, as major

hospital networks integrate centralized remote-command centers directly into

their core care-delivery models.

Regional Insights

- North

America commands the largest market share globally, with the

regional market projected to expand from US$ 11,540.64 Million in 2021 to

US$ 76,657.92 Million by 2028, tracking at a CAGR of 31.1%. This

hyper-growth is anchored by early legislative actions like the Meaningful

Use Act, a high concentration of dominant medical tech developers, and

aggressive institutional adoption across U.S. hospital networks.

- Europe exhibits

an exceptionally robust market footprint, expected to scale from US$

9,442.34 Million in 2021 to US$ 59,123.15 Million by 2028 at a CAGR of

30.0%. Growth is catalyzed by advanced regional telemedicine initiatives,

such as the UK's long-standing NHS integration tracks which project annual

savings of up to US$ 1.35 Billion through reduced hospital visits,

alongside cross-border research projects like MEDIWARN in Italy.

- Middle

East & Africa is tracking substantial expansion, projected to

grow from US$ 1,464.74 Million in 2021 to US$ 8,975.23 Million by 2028,

reflecting a CAGR of 29.6%. The region is heavily led by Saudi Arabia,

where rising public health awareness and structural investments in

healthcare modernization are driving a multi-billion dollar medical device

import market.

- South

America displays steady incremental value acceleration, expected

to rise from US$ 1,217.71 Million in 2021 to US$ 7,085.71 Million by 2028,

registering a solid CAGR of 28.6%, fueled by expanding regional telecom

infrastructure and efforts to bridge the rural-urban medical accessibility

gap.

Top Players in the Remote Patient Monitoring Industry

The competitive ecosystem features an intense consolidation

among multi-national medical instrument conglomerates and diversified digital

healthcare platforms pushing advanced cloud-connectivity standards.

- Medtronic

plc

- Koninklijke

Philips N.V.

- Boston

Scientific Corporation

- Abbott

Laboratories

- OMRON

Corporation (Omron Healthcare)

- Siemens

Healthineers AG

- Nihon

Kohden Corporation

- General

Electric Company (GE Healthcare)

- Cerner

Corporation

- VitalConnect,

Inc.

Technological Innovations

The integration of advanced IoT Interoperability and

low-power communication standards is fundamentally transforming the scalability

of remote care. Next-generation tracking systems leverage seamless Bluetooth

Low Energy (BLE) and cellular IoT (eMTC/NB-IoT) connectivity, allowing medical

devices to activate and safely stream encrypted vital signs automatically right

out of the box, completely independent of complex home Wi-Fi configurations.

Concurrently, clinical software developers are making

significant breakthroughs by integrating predictive AI analytics into

centralized monitoring dashboards. Instead of simply displaying static

historical charts, modern cloud-based systems employ advanced machine learning

algorithms to evaluate complex, multi-parameter trends over time. By

correlating subtle changes in a patient's sleep quality, heart rate

variability, and respiratory rate simultaneously, the system can predict

oncoming clinical deteriorations hours before visible symptoms manifest,

enabling preventative physician intervention.

Future Market Outlook

The future outlook for the Remote Patient Monitoring

Industry remains exceptionally strong. As international healthcare frameworks

complete their structural pivot away from fee-for-service models and fully

embrace value-based care, continuous home-based monitoring will become the

non-negotiable standard for managing post-operative recovery and chronic

illnesses.

Future development will be deeply concentrated in the

commercialization of non-invasive continuous chemical sensing arrays (such as

needle-free multi-analyte tracking patches), the integration of advanced

edge-computing microprocessors directly onto wearable medical bands to handle

immediate anomaly identification without relying on cloud uplinks, and the

deployment of zero-trust biometric encryption systems to maximize patient data

security. Providers that combine clinical-grade sensor accuracy with highly

secure, automated software interfaces will successfully command long-term

global market dominance.

Frequently Asked Questions (FAQs)

How did the COVID-19 pandemic influence the development

of remote patient monitoring systems?

The pandemic acted as a major catalyst by forcing hospital

systems to limit in-person contact with highly infectious patients. To protect

medical staff and preserve personal protective equipment (PPE), facilities

deployed advanced remote vital sign monitors that allowed clinicians to track

heart rates, oxygen levels, and body temperatures accurately from entirely

separate rooms or isolated home environments, accelerating long-term market

adoption.

What is the primary factor restraining the widespread

expansion of the RPM market?

Despite clear technological and economic advantages, the

primary market constraint stems from a lingering reluctance and behavioral

resistance among certain veteran healthcare industry professionals and

institutional providers. Overcoming entrenched clinical workflows and

establishing universal comfort with virtual diagnostics remains an ongoing

evolutionary challenge across specific medical sectors.

What types of diagnostic devices represent the largest

market value within the sector?

The devices segment represents the largest overall share of

the market, driven heavily by specialized hardware categories including cardiac

monitoring systems (wireless Holter monitors/ECG patches), continuous blood

glucose monitors, and multi-parameter vital sign monitors which require

continuous institutional procurement and device lifecycle management.

How do remote patient monitoring systems help lower

global public healthcare costs?

RPM systems lower overall costs by shifting intensive

medical observation out of expensive inpatient hospital beds and into the

patient's home. By providing physicians with real-time, continuous data, the

system helps identify minor health issues early, preventing costly emergency

room visits, lowering hospital readmission rates, and shortening post-surgical

hospital stays.

Browse More Reports:

Pediatric Medical Devices Market

Middle East and Africa Blood Pressure Monitors Market

About Us

Business Market Insights is a market research platform that

provides subscription service for industry and company reports. Our research

team has extensive professional expertise in domains such as Electronics &

Semiconductor; Aerospace & Defense; Automotive & Transportation; Energy

& Power; Healthcare; Manufacturing & Construction; Food &

Beverages; Chemicals & Materials; and Technology, Media, &

Telecommunications.

Contact Us

If you have any questions about this report or would like

further information, please contact us:

Contact person: Ankit Mathur

Email: sales@businessmarketinsights.com

Phone: +16467917070

Comments

Post a Comment