Sensors Market Projected to Achieve US$ 564.69 Billion by 2033

Global digital transformation initiatives are driving the advancement of the Sensors Industry. Key growth factors include the rapid expansion of IoT networks, increasing adoption of Industry 4.0 technologies, and the rising penetration of electric, connected, and autonomous vehicles that depend on highly accurate and reliable sensor systems.

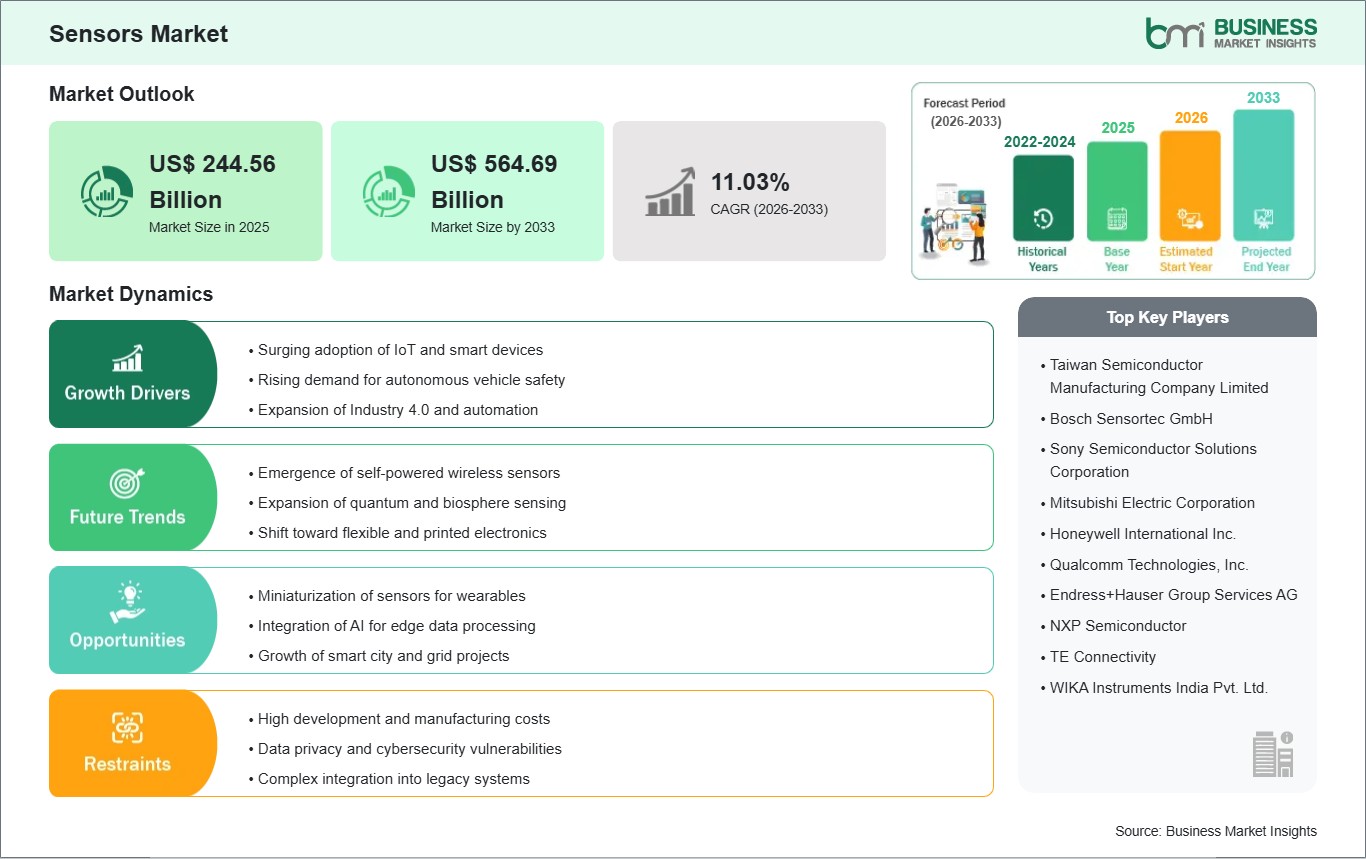

Business Market Insights projects the global Sensors

Market to grow substantially, reaching US$ 564.69 billion by 2033 from US$

244.56 billion in 2025. The market is expected to record a CAGR of 11.03% over

the forecast period spanning 2026 to 2033.

Advancements in Micro-Electro-Mechanical Systems (MEMS), the

deployment of nano-electromechanical systems (NEMS), and the integration of

edge-computing microcontrollers directly onto sensing substrates are

fundamentally altering the competitive landscape. Global component

manufacturers and semiconductor design firms are heavily prioritizing

multi-sensor fusion, ultra-low power continuous-monitoring profiles, and

wireless connectivity to meet the high-density data demands of smart

infrastructure, digital healthcare, and next-generation industrial facilities.

What Are Sensors?

Sensors encompass a comprehensive, mission-critical class of

electronic hardware elements engineered to detect, measure, and record

physical, chemical, or biological changes in an ambient environment, converting

these phenomena into readable electrical signals. Modern sensing architectures

have advanced from simple analog transducers into highly integrated intelligent

nodes capable of cleaning, filtering, and processing raw environmental data at

the network edge before transmitting it to the cloud.

The operational framework of a modern sensor system involves

converting physical stimuli such as temperature, pressure, linear

acceleration, or gas concentrations into digital telemetry. By deploying

complex array matrices utilizing technologies like Complementary

Metal-Oxide-Semiconductor (CMOS) image arrays, piezoelectric crystals, or

optical waveguides, sensors provide the foundational data infrastructure

required for automated logic controllers, safety overrides, and predictive

maintenance algorithms across millions of connected endpoints.

Download Sample Report: https://www.businessmarketinsights.com/sample/BMIPUB00032472

Market Drivers

A primary driver for the Sensors Industry is the rapid

scaling of Industry 4.0 and Smart Manufacturing initiatives. Modern production

facilities are aggressively retrofitting traditional machinery with vibration,

pressure, acoustic emission, and thermal sensors to build comprehensive

condition-based monitoring networks. These deployments allow facility

operations to anticipate mechanical degradation, preventing catastrophic asset

breakdowns and cutting unplanned manufacturing downtime significantly.

The high-volume transition toward Advanced Driver Assistance

Systems (ADAS) and Electric Vehicle (EV) architectures acts as another critical

growth vector. Modern automotive drivetrains and safety platforms demand an

intricate, multi-layered mesh of radar, LiDAR, ultrasonic, and inertial sensors

to accurately map environments, monitor battery thermal states, and execute

automated braking operations safely, transforming sensors from premium add-ons

to mandatory grid requirements.

Furthermore, the explosive growth of the digital healthcare

sector and portable wearable electronics is expanding the hardware market

footprint. Continuous patient tracking demands including non-invasive

glucose patches, smart health bands, and wearable ECG monitors rely

heavily on miniaturized, high-precision biosensors. These components must

deliver reliable clinical analytics while drawing minimal power to guarantee

extended battery lifespans in everyday consumer environments.

Market Segmentation

By Parameter Measured

- Temperature

& Humidity Sensors

- Pressure

& Flow Sensors

- Inertial

& Motion Sensors

- Chemical

& Gas Sensors

- Position

& Proximity Sensors

- Image

& Optical Sensors

By Technology

- Micro-Electro-Mechanical

Systems (MEMS)

- Complementary

Metal-Oxide-Semiconductor (CMOS)

- Nano-Electro-Mechanical

Systems (NEMS)

- Quantum

Sensing & Others

By End-User Industry

- Automotive

& Transportation

- Industrial

Automation & Manufacturing

- Consumer

Electronics & Smart Home

- Healthcare

& Medical Devices

- Aerospace,

Defense, & Marine

- IT

& Telecommunications

The MEMS technology division captures a dominant portion of

the overall market volume, fueled by decades of manufacturing refinement,

excellent yield efficiencies, and their ubiquitous deployment inside billions

of mobile devices and vehicle electronic control units. Concurrently, the

chemical and gas sensing parameter block represents the fastest-growing

technology division by value, accelerated by strict workplace safety rules and

tightening global emission verification standards.

Regional Insights

- North

America commands a highly commanding share of the global sensors

market revenue, heavily anchored by intensive defense and aerospace

innovation, multi-billion dollar capital investments in smart logistics

networks, and high concentrations of leading industrial automation

software developers.

- Asia-Pacific registers

the fastest compound annual growth rate over the projected forecast

horizon, propelled by massive semiconductor assembly capacity expansions,

government-backed smart factory blueprints across China and India, and

intense consumer electronics and EV manufacturing dominance throughout

Japan and South Korea.

- Europe maintains

a highly stable, high-value market footprint, strictly catalyzed by strict

European Union safety regulations and regional carbon reduction mandates.

European automakers are pioneering the integration of standardized

multi-sensor safety layers across commercial vehicle segments to conform

to updating grid safety guidelines.

- Middle

East & Africa and South & Central America are

demonstrating steady incremental volume growth, led by targeted smart

utility infrastructure investments, computerized mining automation

pipelines, and localized environmental tracking initiatives in expanding

urban sectors.

Top Players in the Sensors Industry

The competitive marketplace features an intersection of

global semiconductor heavyweights, specialized industrial engineering

corporations, and electronic component design specialists prioritizing

miniaturization and integrated software libraries.

- Texas

Instruments Incorporated

- Robert

Bosch Sensortec GmbH

- STMicroelectronics

N.V.

- Honeywell

International Inc.

- NXP

Semiconductors N.V.

- Infineon

Technologies AG

- Analog

Devices, Inc.

- TE

Connectivity Ltd.

- Panasonic

Holdings Corporation

- Omron

Corporation

Technological Innovations

The integration of Advanced Sensor Fusion Algorithms is

fundamentally changing modern data management paradigms. Historically,

individual sensors operated in relative isolation, passing raw independent data

lines to a central processing unit. Next-generation smart sensor hubs combine

inputs from multiple disparate elements such as combining IMU

accelerometers, gyroscopes, and pressure sensors onto a single chip

architecture to clean, validate, and compute unified spatial metrics

locally, minimizing network latency and offloading complex tasks from main

system processors.

Concurrently, the manufacturing landscape is moving toward

the commercialization of Quantum Sensors for high-precision applications.

Traditional inertial and magnetic sensors suffer from subtle measurement drifts

across prolonged operational cycles, requiring frequent manual recalibrations.

Quantum sensors utilize the highly stable, predictable properties of atoms or

subatomic particles to deliver completely drift-free positioning tracking and

ultra-high-resolution subsurface imaging, providing a critical breakthrough for

GPS-denied navigation environments and advanced medical mapping.

Future Market Outlook

The future outlook for the Sensors Industry remains

exceptionally favorable. As global commercial, urban, and industrial

infrastructures transition completely toward autonomous, software-defined

ecosystems, legacy standalone components will rapidly phase out, replaced by

fully integrated, self-calibrating edge sensor nodes that communicate

seamlessly over 5G and satellite IoT networks.

Future development will be deeply concentrated in flexible,

biocompatible substrate printings for clinical health monitoring, eco-friendly

sensor housings manufactured from sustainable polymer blends, and self-powered

sensor units harvesting ambient thermal or vibrational energy to eliminate

battery dependencies entirely. Technological innovators that deliver robust,

open-protocol hardware frameworks pairing ultra-low power consumption with

native, chip-level security keys will successfully secure long-term global

market dominance.

Frequently Asked Questions (FAQs)

What is the main operational benefit of moving from

traditional sensors to Smart Sensors?

Traditional sensors simply capture analog data and pass it

along, leaving data cleaning, signal amplification, and fault validation to a

centralized computer. Smart sensors incorporate dedicated onboard

microprocessors and digital signal processing (DSP) layers directly onto the

sensor assembly, allowing the device to perform self-diagnostics, filter out

background noise, and broadcast actionable, structured telemetry instantly.

How does MEMS technology allow for high-volume, low-cost

sensor manufacturing?

Micro-Electro-Mechanical Systems (MEMS) technology utilizes

advanced semiconductor fabrication techniques to print microscopic mechanical

structures, gears, and electrical circuits directly onto silicon wafers. This

allows complex inertial, pressure, and acoustic sensors to be mass-produced by

the millions on single silicon sheets, delivering incredible spatial

miniaturization alongside excellent performance reliability and low cost per

unit.

What specific role do sensors play in vehicle

electrification and battery management systems (BMS)?

Within an electric vehicle battery pack, thousands of

lithium-ion cells operate under tight thermal boundaries. Precise temperature

and current sensors are distributed throughout the pack to continuously

feedback thermal states to the central BMS. If a cell exhibits abnormal

heating, the sensors trigger early warning safety systems or adjust cooling

loops to prevent thermal runaway situations and maximize driving ranges.

Why is sensor cross-sensitivity considered a critical

challenge in chemical and gas tracking?

Sensor cross-sensitivity occurs when a chemical or gas

sensor reacts to a background compound other than the target gas it was

calibrated to measure (for instance, a carbon monoxide sensor throwing an

altered reading due to ambient hydrogen gas). Modern sensor manufacturers

mitigate this by embedding dedicated chemical filtering membranes over sensor

intakes or implementing multi-channel sensor arrays governed by machine

learning lookup tables to isolate the true gas profile.

Browse More Reports:

About Us

Business Market Insights is a market research platform that

provides subscription service for industry and company reports. Our research

team has extensive professional expertise in domains such as Electronics &

Semiconductor; Aerospace & Defense; Automotive & Transportation; Energy

& Power; Healthcare; Manufacturing & Construction; Food &

Beverages; Chemicals & Materials; and Technology, Media, &

Telecommunications.

Contact Us

If you have any questions about this report or would like

further information, please contact us:

Contact person: Ankit Mathur

Email: sales@businessmarketinsights.com

Phone: +16467917070

Comments

Post a Comment