Surgical Lasers Market Projected to Achieve US$ 13.45 Billion by 2033

Technological innovation is transforming the Surgical Lasers Industry across global healthcare markets. The growing utilization of minimally invasive surgeries, increasing surgical procedure volumes, and ongoing advancements in laser wavelengths and delivery systems are driving the adoption of high-precision laser technologies in clinical settings.

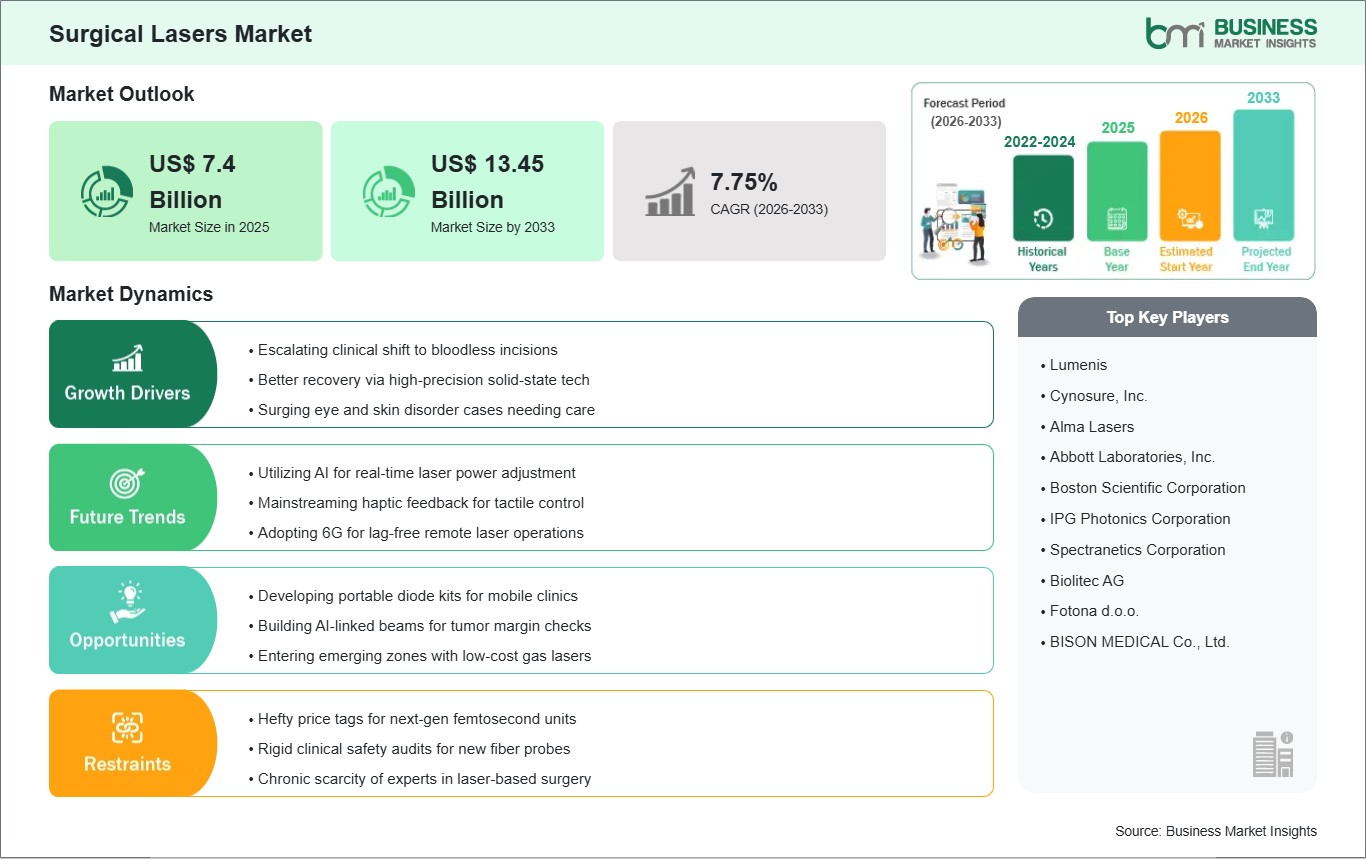

According to Business Market Insights, the global Surgical

Lasers Market was valued at US$ 7.4 billion in 2025 and is anticipated to

reach US$ 13.45 billion by 2033. The market is projected to grow at a CAGR of

7.75% during the forecast period from 2026 to 2033.

Advancements in fiber-optic delivery configurations, the

integration of robotic-assisted laser scanning arms, and the deployment of

multi-wavelength platforms within single console units are fundamentally

altering the competitive landscape. Global medical device manufacturers are

heavily prioritizing advanced pulse-modulation technologies, intelligent

real-time tissue depth feedback sensors, and ergonomic waveguide designs to

ensure absolute safety, reduced intraoperative bleeding, and accelerated recovery

times across diverse surgical specialties.

What Are Surgical Lasers?

Surgical lasers encompass a highly specialized class of

advanced medical hardware units engineered to emit high-intensity, coherent,

and monochromatic beams of light used to slice, vaporize, coagulate, or alter

human biological tissue. Operating under the biophysical principle of selective

photothermolysis, a surgical laser delivers concentrated energy to a specific

target tissue component (chromophore) such as water, hemoglobin, or melanin,

converting light energy into localized thermal energy instantly.

Unlike traditional mechanical scalpels or standard

electrosurgical loops, a surgical laser seals blood vessels and nerve endings

simultaneously as it cuts, drastically minimizing blood loss, post-operative

swelling, and the risk of localized bacterial infections. These medical

instruments utilize distinct lasing mediums including gas chambers

($CO_2$), solid-state crystals (Nd:YAG, Er:YAG), or semiconductor

diodes each emitting specific wavelengths calibrated precisely to execute

varied depths of tissue interaction from superficial dermal resurfacing to deep

internal endoscopic tumor resections.

Download Sample Report: https://www.businessmarketinsights.com/sample/BMIPUB00032479

Market Drivers

A primary driver for the Surgical Lasers Industry is the

accelerating global demand for Minimally Invasive Surgeries (MIS). Modern

patient populations and hospital networks heavily favor surgical approaches

that bypass large open incisions. Surgical lasers, when threaded through narrow

flexible endoscopes, allow surgeons to perform complex internal dissections,

fragmentation of urinary stones, and ocular adjustments through microscopic

entry ports, reducing total inpatient hospital stays and overall healthcare

delivery costs.

The rising global volume of ophthalmic disorders,

particularly age-related cataracts, diabetic retinopathy, and refractive

errors, acts as another critical growth factor. Advanced laser

protocols such as Femtosecond and Excimer systems have become the

global gold standard for refractive corneal reshaping and automated cataract

fragmentation, executing high-repetition, automated microsurgery steps with

micron-level precision that human hands cannot replicate manually.

Furthermore, the soaring volume of elective aesthetic,

dermatological, and plastic surgery procedures is driving high capital hardware

procurement. The widespread clinical adoption of fractional $CO_2$ lasers and

specialized Q-switched systems for non-invasive skin rejuvenation, vascular

lesion clearance, and deep scar revisions creates a highly lucrative, recurring

revenue stream for medical device suppliers worldwide.

Market Segmentation

By Product / Laser Type

- Carbon

Dioxide ($CO_2$) Lasers

- Argon

Lasers

- Nd:YAG

Lasers

- Diode

Lasers

- Excimer

Lasers

- Holmium:YAG

(Ho:YAG) and Thulium Lasers

By Application

- Ophthalmology

(LASIK, Cataract, Retinal Procedures)

- Dermatology

& Aesthetics

- Urology

(BPH Treatment, Lithotripsy)

- Gynecology

& Surgical Oncology

- Cardiovascular

Surgeries

- Dentistry

& Otolaryngology (ENT)

By End-User

- Hospitals

& Specialty Surgical Centers

- Ambulatory

Surgical Centers (ASCs)

- Dermatology

Clinics & Medical Spas

The solid-state lasers division (encompassing Nd:YAG and

Holmium systems) captures a dominant portion of the overall market volume,

fueled by their versatile multi-disciplinary applications in urology for kidney

stone blasting (lithotripsy) and oncology for precise soft-tissue margins.

Concurrently, the ambulatory surgical centers (ASCs) end-user segment

represents the fastest-growing division by value, propelled by rapid

transitions toward outpatient settings that heavily prioritize rapid-recovery,

low-complication laser technologies.

Regional Insights

- North

America commands the largest share of the global surgical lasers

market revenue, heavily anchored by a highly sophisticated healthcare

infrastructure, high healthcare expenditure per capita, rapid adoption of

robotic-integrated medical platforms, and high demand for cosmetic and

elective ophthalmic procedures.

- Asia-Pacific registers

the fastest compound annual growth rate over the projected forecast

horizon, propelled by massive state-backed healthcare infrastructure

modernizations, expanding medical tourism networks across India and

Thailand, and a surging geriatric population demanding non-invasive

urological and cataract interventions throughout China and Japan.

- Europe maintains

a highly substantial, high-value market footprint, strictly catalyzed by

strict CE-mark safety certifications, robust clinical research programs,

and clear regulatory guidelines supporting the integration of energy-based

surgical tools in modern public utility hospitals.

- Middle

East & Africa and South & Central America are

demonstrating steady incremental volume growth, led by targeted

investments in private specialty care clinics and the gradual expansion of

advanced clinical training programs for laser-safe operating rooms.

Top Players in the Surgical Lasers Industry

The competitive landscape exhibits intense technological

competition among established global medical device conglomerates and

hyper-focused optical physics innovators, with top players prioritizing

multi-wavelength consolidations and smart software user interfaces.

- Lumenis

Be Ltd. (Boston Scientific Corporation)

- Cynosure,

Inc.

- Alma

Lasers Ltd. (Sisram Medical Ltd)

- Coherent,

Inc.

- IPG

Photonics Corporation

- Biolase,

Inc.

- El.En.

S.p.A.

- Topcon

Corporation

- Carl

Zeiss Meditec AG

- Cutera,

Inc.

Technological Innovations

The integration of Thulium Fiber Laser (TFL) technology is

fundamentally transforming modern endourology. For decades, Holmium: YAG lasers

served as the core baseline for breaking down urinary calculi. Next-generation

TFL devices emit at an ultra-precise wavelength ($1,940\text{ nm}$) that

perfectly matches the peak absorption spectrum of liquid water inside stones

and tissue, allowing for a "dusting" effect that disintegrates stones

into microscopic sand-like particles rapidly while generating minimal

retropulsion (pushing the stone away from the laser tip).

Concurrently, the medical device architecture is pivoting

toward AI-Guided Robotic Laser Delivery platforms. Traditional manual laser

handpieces require highly precise steadiness to avoid stray thermal injury to

adjacent healthy organs. Modern integrated configurations link the surgical

laser beam directly with real-time optical coherence tomography (OCT) scanning

loops. The system's machine learning software dynamically measures tissue

boundaries at the sub-millimeter level, automatically cutting off laser power

instantly if a patient moves or if the laser encounters a vital blood vessel

boundary.

Future Market Outlook

The future outlook for the Surgical Lasers Industry remains

exceptionally robust. As global healthcare grids adapt to manage an aging

population with high chronic disease rates, the push to reduce bed-occupancy

cycles will shift standard surgical protocols permanently toward light-based,

outpatient interventions.

Future development will be deeply concentrated in

ultra-miniaturized flexible fiber waveguides that can negotiate tortuous

vascular networks, eco-friendly systems featuring low standby electrical draws,

and completely automated, multi-spectral consoles that shift their active

output parameters dynamically based on real-time spectrometer readings of the

target organ. Medical technology developers that master seamless

hardware-software integration while providing intuitive safety profiles for

operating room personnel will successfully secure long-term global market

dominance.

Frequently Asked Questions (FAQs)

Why is the $CO_2$ laser wavelength uniquely suited for

soft-tissue oral and ENT surgeries?

The Carbon Dioxide ($CO_2$) laser operates at a wavelength

of $10,600\text{ nm}$, which is heavily absorbed by water molecules the

primary constituent of soft human tissue. This high absorption rate allows the

$CO_2$ laser beam to vaporize cellular structure cleanly with minimal

penetration depth (typically less than $0.1\text{ mm}$), enabling incredibly

clean incisions with a microscopic thermal zone that preserves delicate

adjacent vocal or oral structures.

What is the significance of "retropulsion" in

laser lithotripsy, and how do new lasers mitigate it?

Retropulsion occurs when the blast energy from a laser pulse

pushes a kidney stone away from the surgeon's viewing scope, forcing them to

chase the stone deeper into the kidney, which risks internal tissue scraping.

Advanced Thulium and high-frequency Holmium lasers mitigate this issue by

emitting ultra-short pulses at high repetitions, transforming the stone into

fine dust through gentle continuous ablation rather than forceful physical

fragmentation.

How do medical teams maintain safety protocols in an

active surgical laser operating theater?

Surgical lasers operate using high energy that can reflect

off shiny surgical instruments, creating eye hazards or fire risks. Operating

theaters enforce strict safety zones, including the mandatory use of

wavelength-specific protective eyewear for all staff, the deployment of

specialized matte-finish (non-reflective) surgical tools, and the continuous

use of high-volume smoke evacuators to filter out hazardous bio-aerosols

generated during tissue vaporization.

What is the operational difference between continuous

wave (CW) and pulsed laser delivery?

Continuous wave delivery emits a steady, uninterrupted

stream of laser light, which is useful for rapid coagulation but can cause heat

to build up in surrounding tissues. Pulsed laser delivery releases energy in

rapid, high-peak-power bursts measured in milliseconds or femtoseconds. This

allows target tissues to cool down between pulses (thermal relaxation time),

preventing unwanted heat propagation to surrounding structures.

Browse More Reports:

Nuclear Medicine Equipment Market

About Us

Business Market Insights is a market research platform that

provides subscription service for industry and company reports. Our research

team has extensive professional expertise in domains such as Electronics &

Semiconductor; Aerospace & Defense; Automotive & Transportation; Energy

& Power; Healthcare; Manufacturing & Construction; Food &

Beverages; Chemicals & Materials; and Technology, Media, &

Telecommunications.

Contact Us

If you have any questions about this report or would like

further information, please contact us:

Contact person: Ankit Mathur

Email: sales@businessmarketinsights.com

Phone: +16467917070

Comments

Post a Comment