Urology Devices Market Projected to Achieve US$ 85.55 Billion by 2033

Technological innovation is transforming the global Urology Devices Industry, with healthcare systems increasingly adopting precision-based diagnostic and surgical technologies. The rising incidence of kidney disorders, urinary incontinence, benign prostatic hyperplasia, and other urological conditions is driving demand for advanced devices that enable safer and more effective treatment outcomes.

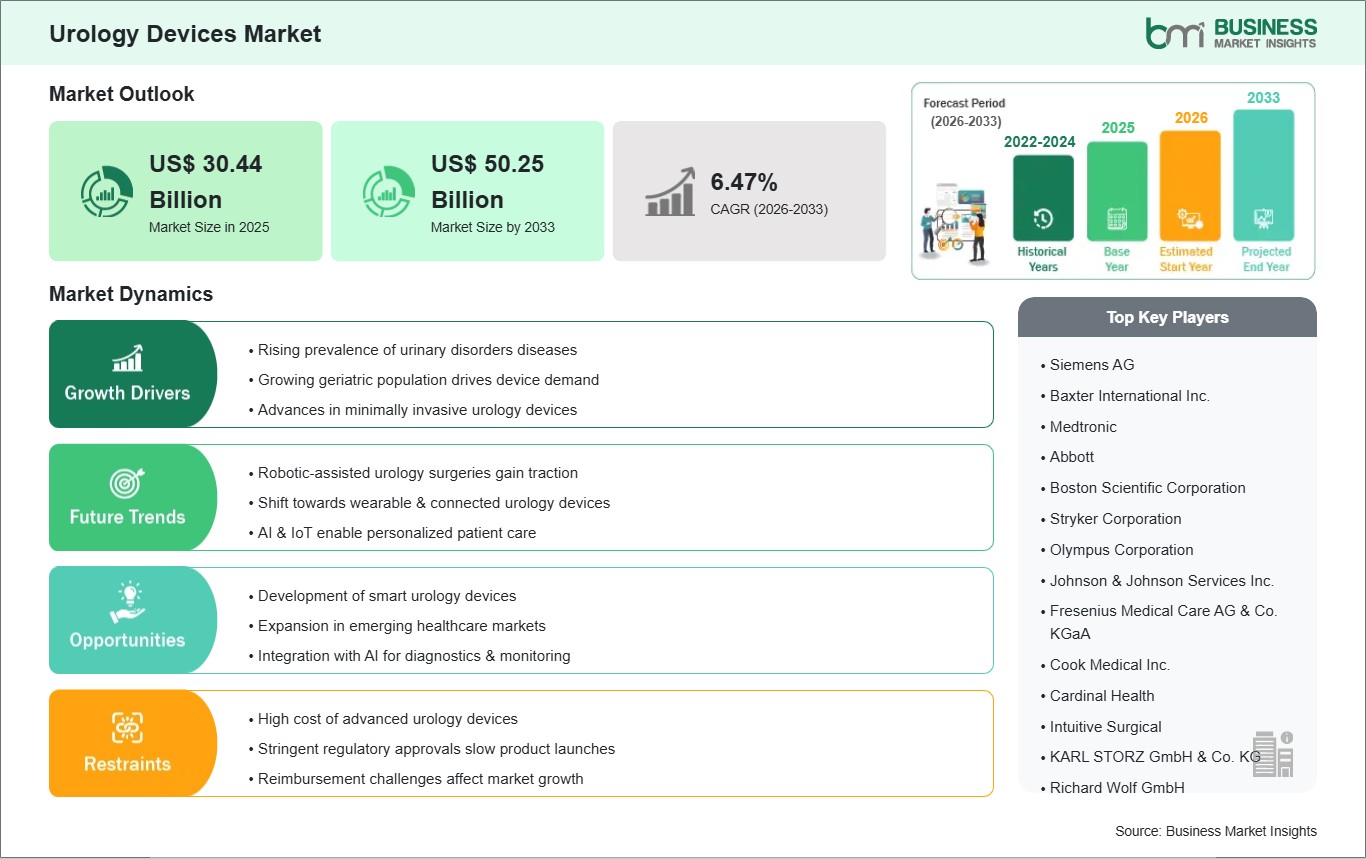

According to Business Market Insights, the global Urology

Devices Market was valued at US$ 51.25 billion in 2025 and is

anticipated to reach US$ 85.55 billion by 2033. The market is projected to grow

at a CAGR of 6.61% during the forecast period from 2026 to 2033.

Advancements in miniaturized digital visualization,

solid-state laser optics, artificial intelligence-driven navigation platforms,

and patient-specific biomaterial designs are fundamentally reshaping the

competitive sector. Leading medical technology syndicates are channeling

substantial capital into the development of highly specialized single-use

endoscopes and robotic-assisted surgical subsystems. These technological

enhancements are explicitly targeted at mitigating cross-contamination risks,

improving procedural throughput, and elevating tactile feedback mechanics for

specialized clinical operators across both consolidated acute care channels and

decentralized surgical settings.

What Is a Urology Device?

A urology device is any specialized medical instrument,

equipment, implant, or consumable item explicitly engineered for the diagnostic

evaluation, surgical intervention, or therapeutic management of structural and

functional anomalies within the urinary system and male genitourinary tracts.

This multi-tiered technology vertical spans from capital-intensive

infrastructure such as multi-arm robotic surgical suites, holmium/thulium laser

lithotripsy systems, and high-resolution digital cystoscopes to high-volume,

clinically critical consumables including specialized hydrophilic guidewires,

double-J ureteral stents, and advanced multi-lumen Foley catheters. Each system

configuration is meticulously calibrated to navigate complex, delicate

anatomical pathways while minimizing localized tissue trauma.

Operating within modern clinical environments, these systems

utilize diverse mechanical, optical, and thermal energy mechanisms to execute

precise therapies. For instance, in intracorporeal lithotripsy, advanced laser

devices deliver focused, high-frequency shockwaves through micro-optical fibers

directly to target urinary calculi, pulverizing dense mineral stones into

easily passable fragments without injuring surrounding mucosal tissue layers.

Similarly, modern urodynamic testing systems combine micro-differential

pressure sensors and electromyographic channels to map real-time bladder

compliance, providing clinicians with high-fidelity biometric data crucial for

engineering highly individualized therapeutic pathways for severe pelvic organ

prolapse or neuromuscular bladder dysfunction.

Download Sample Report: https://www.businessmarketinsights.com/sample/BMIPUB00032605

Market Drivers

A primary driver accelerating the global Urology Devices

Industry is the Escalating Global Prevalence of Chronic Urological Illnesses

and End-Stage Renal Disease. Changing lifestyle factors, rising systemic

metabolic disorders such as type-2 diabetes, and an expanding global geriatric

demographic have collectively driven a major increase in kidney stone

formations, severe urinary tract obstructions, and chronic kidney failure.

Because end-stage renal conditions necessitate continuous, high-volume therapeutic

interventions, the global demand for advanced hemodialysis equipment,

continuous renal replacement therapy (CRRT) systems, and specialized vascular

access consumables is experiencing sustained structural growth across all tiers

of global healthcare delivery.

The universal clinical paradigm shift toward Minimally

Invasive Urological Procedures and Single-Use Endoscopic Technologies serves as

another vital market driver. Traditional reusable endoscopes carry intense

long-term operational overheads, requiring meticulous, multi-stage chemical

reprocessing and posing persistent risks of hospital-acquired infections or

biofilm cross-contamination. Consequently, urologists and hospital procurement

networks are aggressively transitioning to high-definition, disposable,

single-use digital ureteroscopes and cystoscopes. These lightweight systems

deliver exceptional optical clarity and maximal deflection angles right out of

the sterile packaging, effectively eliminating reprocessing bottlenecks and

drastically reducing per-procedure clinical liabilities.

Additionally, the rising international adoption of Advanced

Robotic Surgical Systems and Micro-Invasive Prostatic Therapies acts as a

powerful driver. Structural anomalies such as Benign Prostatic Hyperplasia

(BPH) traditionally required aggressive transurethral resections with prolonged

recovery timelines. The commercial introduction of next-generation

robotic-assisted soft tissue enucleation setups and micro-invasive mechanical

implants has completely optimized these clinical workflows. These cutting-edge

systems provide multi-DOF articulation and structural stabilization, allowing

surgeons to preserve critical nerve structures, significantly minimize

intraoperative blood loss, and successfully transition complex urological

surgeries into rapid-recovery outpatient procedures.

Market Segmentation

By Product Type

- Urology

Instruments (Robotic surgical platforms, thulium/holmium lasers,

lithotripsy devices, rigid and flexible endoscopes, hemodialysis machines,

and advanced urodynamic diagnostics)

- Consumables

& Accessories (Hydrophilic guidewires, ureteral stents, disposable

ureteroscopes, biopsies, urinary catheters, drainage bags, and continence

care items)

By Application

- Kidney

Diseases & Renal Failure Management

- Benign

Prostatic Hyperplasia (BPH) & Urological Cancers

- Urinary

Calculi / Kidney Stones Therapy

- Urinary

Incontinence & Pelvic Organ Prolapse Restoration

- Others

By End-User

- Hospitals

& Specialty Clinics (Centralized hubs commanding high-volume, complex

capital installations)

- Dialysis

Centers & Nephrology Clinics (High-frequency, dedicated chronic care

processing networks)

- Ambulatory

Surgical Centers (ASCs) (The fastest-growing procedural tier focused on

cost-efficient, same-day surgical care)

- Homecare

Settings (Supporting decentralized peritoneal dialysis and continuous

urinary drainage management)

The Urology Instruments segment commanded the absolute

largest revenue share of the global market matrix in 2025, driven by continuous

capital infrastructure upgrades, widespread deployment of multi-arm robotic

interfaces, and the high initial acquisition costs of solid-state laser

installations. Concurrently, the Consumables & Accessories vertical led the

structural volume landscape due to non-cyclical, daily unit consumption across

acute care facilities, while the Ambulatory Surgical Centers (ASCs) end-user

vertical is tracking the fastest projected compound growth rate due to global

healthcare reforms favoring rapid-turnaround outpatient surgical models.

Regional Insights

- North

America holds the premier revenue share of the global urology

devices market, controlling roughly 40% of the total geographic matrix.

This leading presence is sustained by an ultra-mature digital healthcare

infrastructure, exceptionally high adoption rates for premium

robotic-assisted surgical platforms, and comprehensive universal insurance

coverage models that actively reimburse advanced minimally invasive

interventions for BPH and urinary calculi.

- Europe maintains

a highly sophisticated, value-driven market footprint, driven by strict

medical safety frameworks and well-funded public health programs across

Germany, France, and the UK. Market development across this regional block

focuses heavily on the institutional integration of single-use endoscopic

ecosystems to manage high-volume geriatric urological interventions while

minimizing cross-contamination overheads.

- Asia-Pacific is

recording the highest projected CAGR during the forecast period, fueled by

rapid hospital infrastructure modernization, expanding medical tourism

networks, and massive patient demographics across China, India, and Japan.

Strategic distribution expansions by multinational developers, alongside a

rising regional awareness of specialized prostate and renal care, are

driving immense volumetric demand for instruments and consumables alike.

- Rest

of the World (Middle East & Africa and South America) is

demonstrating steady incremental expansion, supported by targeted

investments from premium private healthcare groups within prominent

metropolitan zones, public water-quality remediation campaigns that reduce

stone disease incidence, and municipal infrastructure updates across

regional clinical diagnostic laboratories.

Top Players in the Industry

The competitive marketplace features a highly concentrated

structure dominated by multi-national medical device corporations that maintain

expansive patent portfolios, strict regulatory clearances, and comprehensive

international clinical training networks.

- Boston

Scientific Corporation

- Olympus

Corporation

- KARL

STORZ SE & Co. KG

- Teleflex

Incorporated

- Richard

Wolf GmbH

- BD

(Becton, Dickinson and Company)

- Cook

Medical LLC

- Coloplast

A/S

- Fresenius

Medical Care AG & Co. KGaA

- Intuitive

Surgical, Inc.

Technological Innovations

The industrial deployment of Next-Generation Moses

Technology and High-Power Thulium Fiber Laser (TFL) systems represents a

massive technological milestone for urological stone management. Conventional

holmium lasers often generate significant retropulsion, inadvertently pushing

kidney stones further up the ureter during ablation and extending overall

surgical time. Next-generation Thulium Fiber Lasers utilize an ultra-short

wavelength that is exceptionally well-absorbed by water, allowing for ultra-high-frequency

dusting of hard calculi. This allows clinical operators to cleanly vaporize

stones into a fine sediment layer with virtually zero retropulsion, vastly

accelerating stone-clearance efficiency and significantly lowering the risk of

post-operative ureteral structural injury.

Concurrently, the integration of Artificial Intelligence and

Real-Time Computer Vision into digital endourology is radically modernizing

clinical diagnostic pipelines. Traditional cystoscopic evaluations rely

entirely on the subjective, real-time visual assessment of the attending

surgeon, which can occasionally lead to the under-detection of flat,

early-stage bladder malignancies. Next-generation smart endoscope systems

incorporate real-time deep learning classification models that automatically

scan the high-definition mucosal feed. These algorithms instantly flag

anomalous vascular patterns, outline suspicious tissue borders, and provide

intraoperative navigation overlays, significantly improving diagnostic biopsy

precision and maximizing long-term patient oncological outcomes.

Future Market Outlook

The future trajectory for the Urology Devices Market remains

exceptionally positive. As global clinical protocols permanently cement

minimally invasive and robotic surgeries as the absolute standard of care, and

structural global demographic shifts continue to expand the baseline patient

pool requiring chronic renal and prostatic management, the universal

consumption of these specialized medical devices will scale steadily, defining

modern surgical efficiency protocols.

Future research and development capital will be heavily

directed toward the commercialization of digital telerehabilitation platforms

for pelvic floor monitoring, the scaling of fully biodegradable ureteral stents

that naturally dissolve post-recovery to eliminate a second extraction

procedure, and the expansion of smart, cloud-connected home peritoneal dialysis

devices. Organizations that successfully deliver high-definition disposable

instruments while keeping unit manufacturing costs competitive will comfortably

command long-term global market leadership.

Frequently Asked Questions (FAQs)

What product category currently dominates global urology

market revenue?

The Urology Instruments segment commands the dominant

revenue share, driven by the substantial initial capital investments required

to acquire and maintain multi-arm robotic surgical suites, advanced laser

lithotripsy infrastructure, and high-resolution diagnostic endovision networks.

Why are single-use disposable endoscopes expanding so

rapidly across urology clinics?

Single-use endoscopes eliminate all cross-contamination and

biofilm transmission risks between patients, bypass the highly labor-intensive

chemical sterilization and reprocessing workflows required for reusable scopes,

and ensure maximum mechanical deflection capabilities for every single

procedure.

How do thulium fiber lasers improve kidney stone ablation

procedures?

Thulium fiber lasers operate at an optimized wavelength that

maximizes energy absorption in water. This allows for ultra-high-frequency

stone dusting, transforming solid mineral stones into a fine powder instantly

while preventing retropulsion, thereby protecting delicate ureteral walls from

surgical trauma.

Which regional market is demonstrating the fastest

compound growth rate?

The Asia-Pacific region is tracking the fastest projected

compound growth rate, propelled by intensive healthcare infrastructure updates,

expanding public insurance accessibility in China and India, and a massive

regional patient demographic requiring advanced urological and nephrological

therapies.

Browse More Reports:

Kidney Dialysis Equipment Market

North America Intraocular Pressure Monitors Market

About Us

Business Market Insights is a market research platform that

provides subscription service for industry and company reports. Our research

team has extensive professional expertise in domains such as Electronics &

Semiconductor; Aerospace & Defense; Automotive & Transportation; Energy

& Power; Healthcare; Manufacturing & Construction; Food &

Beverages; Chemicals & Materials; and Technology, Media, &

Telecommunications.

Contact Us

If you have any questions about this report or would like

further information, please contact us:

Contact person: Ankit Mathur

Email: sales@businessmarketinsights.com

Phone: +16467917070

Comments

Post a Comment