Vascular Access Devices Market Future Outlook and 7.67% CAGR Trends

Global advancements in healthcare

delivery and patient management are driving the evolution of the Vascular

Access Devices Industry. Key growth factors include the increasing prevalence

of chronic diseases, growing demand for long-term infusion therapies, expanding

surgical activity, and the adoption of advanced vascular access technologies

designed to reduce catheter-associated complications and improve treatment

effectiveness.

Business Market Insights

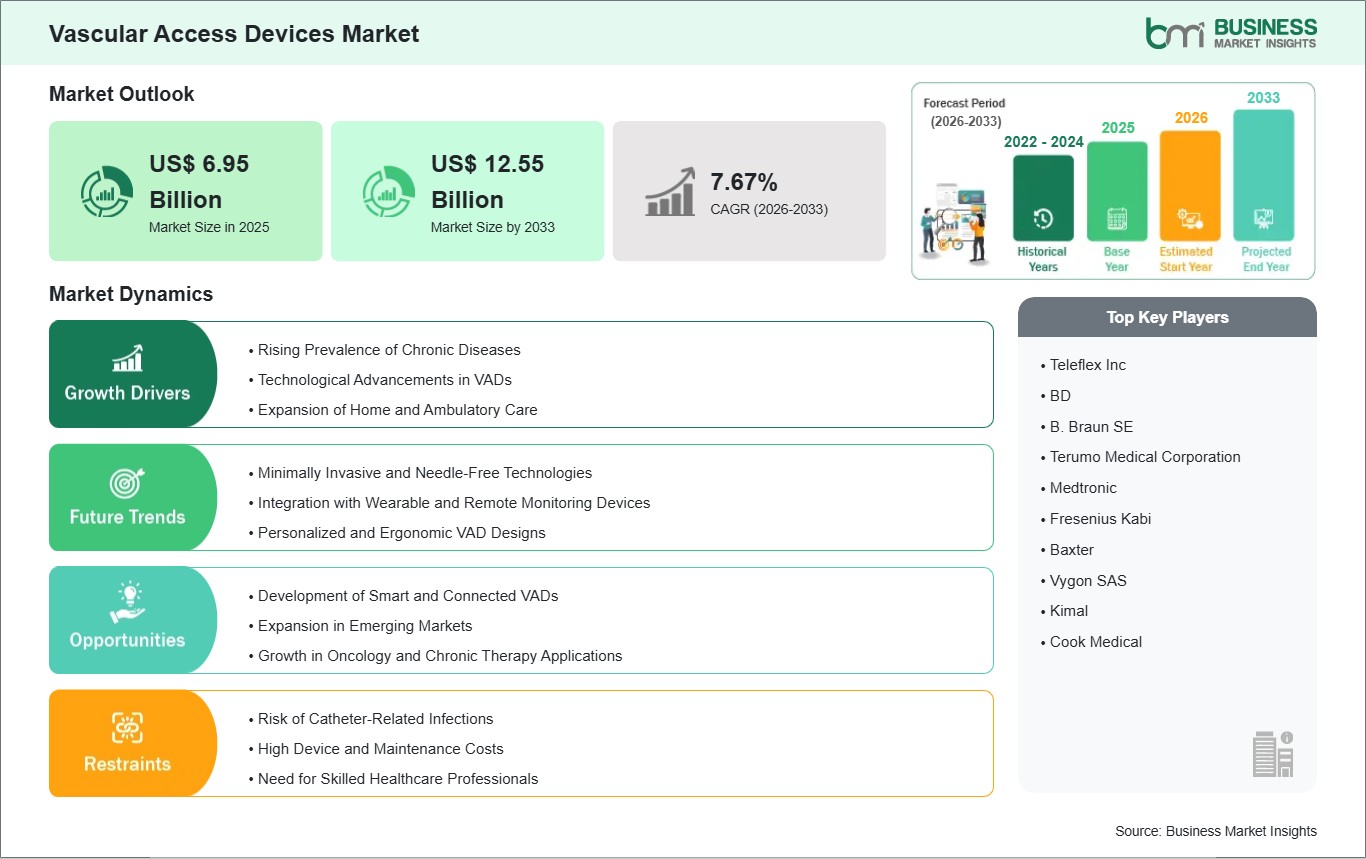

projects the global Vascular

Access Devices Market to grow substantially, reaching US$ 12.55

billion by 2033 from US$ 6.95 billion in 2025. The market is expected to record

a CAGR of 7.67% over the forecast period spanning 2026 to 2033.

Advancements in antithrombogenic

surface modifications, antimicrobial lumen coatings, integrated ultrasound

guidance systems, and real-time catheter tip-placement verification

technologies are completely redefining the competitive landscape. Leading medical

device conglomerates are investing significant capital to optimize catheter

geometry, introduce passive needle shielding features, and develop highly

biocompatible polymers like advanced polyurethane and silicone formulations.

These engineering developments are directly calculated to mitigate Central

Line-Associated Bloodstream Infections (CLABSIs), eliminate accidental

needlestick injuries among clinical staff, and streamline vascular placement

workflows across acute, ambulatory, and home infusion environments globally.

What Is a Vascular Access

Device?

A vascular access device (VAD) is

a specialized, medically engineered catheter designed to be inserted into the

human central or peripheral circulatory system to establish reliable,

continuous, or intermittent access to the bloodstream. Unlike standard therapeutic

delivery tools, modern vascular access platforms are sophisticated

fluid-delivery systems designed to withstand varying fluid pressures, prevent

vessel wall degradation, and minimize immunogenic responses. These systems are

carefully integrated with specialized hubs, luer-lock connectors, and

sutureless securement systems to maintain absolute structural integrity

throughout their indicated clinical dwell time.

Operating across distinct clinical

tiers, vascular access devices are categorized based on their anatomical

insertion point and therapeutic duration. Peripheral systems, such as short

peripheral intravenous catheters (PIVCs) and midline options, are designed for

short-to-intermediate therapies where medications possess standard osmolarity

profiles. Conversely, Central Vascular Access Devices (CVADs) including

Peripherally Inserted Central Catheters (PICCs), non-tunneled central venous

catheters, and totally implantable subcutaneous ports are threaded directly

into large-caliber veins, terminating within the superior vena cava. This

direct central positioning allows for the immediate dilution of highly irritant

or hyperosmolar solutions, such as intensive chemotherapy cocktails, long-term

total parenteral nutrition (TPN), and specialized biological agents,

safeguarding the integrity of peripheral vasculature.

Download Sample Report: https://www.businessmarketinsights.com/sample/BMIPUB00032633

Market Drivers

A primary driver accelerating the

global Vascular Access Devices Industry is the Escalating Global Prevalence of

Chronic Diseases and Associated Long-Term Intravenous Therapies. The worldwide

surge in new cancer diagnoses, chronic kidney disease (CKD) requiring regular

hemodialysis, advanced cardiovascular disorders, and severe autoimmune

conditions has generated an unprecedented volume of patients requiring repeated

or long-term vascular entry. Because targeted oncology protocols demand serial

chemotherapy administration and regular biomarker testing over extended

operational cycles, the clinical onboarding of durable, pressure-rated central

lines and implantable ports has become non-negotiable for protecting remaining

patient venous capital and maximizing treatment compliance scores.

The rapid clinical migration

toward Safety-Engineered Catheters and Stringent Regulatory Occupational Health

Mandates represents another fundamental driver. Institutional safety networks

and international healthcare watchdogs have established zero-tolerance

guidelines regarding needlestick injuries and clinical cross-contamination

vectors. In response, modern healthcare procurement systems are prioritizing

next-generation vascular catheters equipped with passive integrated needle

shields, needleless valves, and advanced antimicrobial coatings. These features

automatically isolate sharp elements upon withdrawal and inhibit the formation

of microscopic cellular biofilms, allowing hospitals to lower overall

complication rates and achieve full alignment with occupational safety

regulations.

Furthermore, the structural shift

toward Outpatient Care, Ambulatory Infusion Centers, and Home Healthcare

Ecosystems is acting as a powerful growth catalyst. Driven by a universal push

to contain escalating hospital inpatient costs and alleviate pressure on acute

care wings, many complex clinical therapies are transitioning directly to the

community care space. Specialized vascular devices like extended-dwell midlines

and PICCs allow patients to receive sophisticated intravenous antibiotic

treatments or parenteral fluids safely within their homes. This continuous

decentralized volume expansion is heavily supported by the deployment of

intuitive, user-friendly catheter configurations that require less intensive

specialist maintenance, encouraging long-term market expansion outside

traditional hospital walls.

Market Segmentation

By Product Type

- Short

Peripheral Intravenous Catheters (PIVCs) (The volume-leading segment

driven by ubiquitous short-term hospital admissions and a continuous shift

toward premium safety-engineered models)

- Midline

Catheters (Bridging the gap between standard peripheral and central lines

for intermediate 1-to-4 week therapeutic timelines)

- Peripherally

Inserted Central Catheters (PICCs) (Widely utilized for

intermediate-to-long term therapies due to bedside placement convenience

and reduced insertion risks)

- Central

Venous Catheters (CVCs) (High-capacity, multi-lumen units essential for

intensive care, hemodynamic monitoring, and acute resuscitation)

- Implantable

Ports (Subcutaneous, long-term access solutions heavily preferred within

oncology and outpatient infusion cycles)

- Accessories

(Catheter securement devices, antimicrobial patches, needleless

connectors, and specialized luer-access systems)

By Route of Insertion

- Intravenous

(The dominant entry segment utilized for immediate, high-velocity systemic

delivery of medications, blood products, and vital fluid volumes)

- Subcutaneous

(Deployed primarily for localized implantable port reservoirs and

continuous targeted tissue infusions)

By Application

- Drug

Administration (The absolute largest application vertical, driven by the

expanding volume of intravenous antibiotic therapies, biologics, and

chemotherapy regimens)

- Fluid

and Nutrition Administration (Crucial for critical care parenteral

nutrition pathways and extensive intraoperative fluid balancing)

- Transfusion

of Blood Products (Essential for emergency trauma responses, complex

hematological therapies, and major surgical suites)

- Other

Applications (Including serial diagnostic testing, central venous pressure

monitoring, and therapeutic apheresis)

By End-User

- Hospitals

and Clinics (The leading purchasing vertical commanding massive

institutional fleets, supported by concentrated clusters of highly skilled

vascular access teams)

- Ambulatory

Surgical Centers (ASCs) (Poised for high compound growth fueled by the

global migration toward same-day minimally invasive surgical protocols)

- Other

End Users (Expanding rapidly through dedicated home infusion agencies,

standalone dialysis clinics, and specialized diagnostic centers)

The Short Peripheral Intravenous

Catheters segment commanded the dominant revenue and volume share of the global

market matrix in 2025, maintaining its clear position due to the high volume of

routine hospital admissions requiring basic intravenous lines. Concurrently,

the Drug Administration segment led the application matrix owing to the

baseline reliance on intravenous pathways for modern therapeutics, while the

Central Vascular Access Devices vertical is tracking high projected growth

rates, propelled by expanding oncology pipelines and multi-lumen therapy

requirements globally.

Regional Insights

- North

America holds the premier revenue share of the global vascular

access devices market, controlling a significant portion of the total

geographic matrix. This leadership is sustained by a mature, highly

technical healthcare network, strict institutional clinical guidelines

regarding CLABSI prevention, and deep financial reimbursement frameworks

for premium safety-engineered devices. High integration of advanced

image-guided catheter placement solutions solidifies the region as the

primary hub for high-value technology adoption.

- Europe maintains

a highly regulated, substantial market presence, characterized by a strong

clinical preference for safety-compliant, needleless architectures and

advanced antimicrobial coatings. Regional development across Germany,

France, the UK, and Italy focuses heavily on value-based healthcare

procurement, expanding home infusion care models, and adhering to rigorous

European safety marking directives to minimize workplace contamination

vectors.

- Asia-Pacific represents

the fastest-growing geographic block, recording a lucrative growth

trajectory during the forecast matrix. Driven by rapid hospital

modernization campaigns, surging middle-class disposable capital,

expanding insurance accessibility, and a massive patient demographic

suffering from severe chronic and lifestyle illnesses across China, India,

and Japan, this region is generating immense volume requirements. Major

multi-national firms are actively expanding their localized production

footprints here to capitalize on the rapid expansion of healthcare

infrastructure.

- Rest

of the World (Middle East & Africa and South America) is

demonstrating steady, progressive expansion patterns. Growth across South

America is heavily anchored by expanding medical centers in Brazil and

Argentina, while the Middle East is recording an uptick in premium

critical care facilities and dedicated oncology clinics within urban

metropolitan hubs, driven by public healthcare diversification

initiatives.

Top Players in the Vascular

Access Devices Industry

The industrial landscape features

high corporate consolidation, with top-tier multi-national medical technology

corporations managing a substantial portion of global market value through

extensive patent cross-licensing, rigorous regulatory clearance loops, and

comprehensive hospital group purchasing contracts.

- BD

(Becton, Dickinson and Company)

- B.

Braun Medical Inc.

- Teleflex

Incorporated

- Medtronic

plc

- Edwards

Lifesciences Corporation

- ICU

Medical, Inc. (including Smiths Medical)

- Cook

Medical LLC

- AngioDynamics,

Inc.

- Argon

Medical Devices, Inc.

- Terumo

Corporation

Technological Innovations

The industrial onboarding of

Advanced Antimicrobial and Antithrombogenic Material Coatings represents a

massive technological milestone for the vascular access sector. Historically,

long-term indwelling catheters were highly susceptible to immediate bacterial

colonization and fibrin sheath formation, which frequently forced premature

device removal and initiated costly hospital infections. Next-generation

catheters feature specialized surfaces infused with chlorhexidine gluconate,

silver sulfadiazine, or advanced hydrophilic polymers that actively repel

bacterial adhesion and inhibit thrombus formation. These smart surface

modifications maintain long-term device patency, protect patient vessel health,

and dramatically lower institutional CLABSI rates without altering baseline

catheter insertion protocols.

Concurrently, the integration of

Real-Time Tip-Placement Verification Systems and Miniaturized Ultrasound

Guidance has fundamentally revolutionized clinical insertion safety.

Historically, verifying the accurate placement of a central line required a post-procedural

chest X-ray, creating distinct operational delays and exposing patients to

radiation. Modern vascular access platforms leverage integrated stylets

utilizing magnetic tracking and electrocardiogram (ECG) tech to monitor the

catheter tip's precise path through the vasculature in real time. This

immediate feedback allows clinicians to execute accurate adjustments directly

at the bedside, ensuring optimal placement within the superior vena cava,

eliminating secondary positioning procedures, and maximizing clinical workflow

efficiency.

Future Market Outlook

The future trajectory for the

Vascular Access Devices Market remains exceptionally robust. As global health

models permanently cement long-term targeted therapies as the standard of care

and clinical environments continue to demand advanced needle-free and

infection-resistant solutions, the global consumption of safety-engineered

catheters and automated visualization systems will scale continuously, defining

the parameters of modern clinical fluid management.

Future research and development

capital will be heavily directed toward the commercialization of fully

bio-resorbable securement materials, the development of smart sensors

integrated into catheter hubs capable of tracking real-time local flow rates or

detecting early signs of interstitial fluid infiltration, and the optimization

of ultra-durable homecare midlines designed for remote telerehabilitation

tracking. Organizations that successfully balance superior anti-infective

material properties with competitive, scalable manufacturing cost margins will

comfortably command long-term global market leadership.

Frequently Asked Questions

(FAQs)

What product category currently

commands the dominant revenue share in the vascular access devices market?

The Short Peripheral Intravenous

Catheters (PIVCs) segment holds the largest share of the market matrix, driven

by their widespread, non-cyclical utilization in routine hospitalizations,

emergency care admissions, and short-term drug administration protocols

worldwide.

How do integrated tip-placement

verification systems improve patient safety?

Integrated tip-verification

technologies use real-time ECG and magnetic tracking to guide clinicians during

central catheter insertion. This ensures the tip terminates perfectly within

the superior vena cava, completely eliminating the need for post-procedural

chest X-rays and reducing mechanical insertion complications.

Why are antimicrobial and

antithrombogenic coatings critical for long-term catheters?

These advanced surface

modifications actively inhibit bacterial colonization and prevent the

accumulation of platelets and fibrin sheaths on the catheter walls. This

significantly reduces the risks of catheter occlusion and Central

Line-Associated Bloodstream Infections (CLABSIs), extending the usable dwell

time of the device.

Which geographic region is

recording the fastest compound growth rate for vascular access devices?

The Asia-Pacific region is

tracking the fastest projected compound growth rate, propelled by massive

hospital infrastructure expansions, rising healthcare investments, an aging

population, and a surging regional burden of lifestyle illnesses like diabetes

and cardiovascular disorders.

Browse More Reports:

Western Europe Cancer Chemotherapy Market

South and Central America Cancer Radiation Therapy Market

GCC Neurovascular Catheters Market

About Us

Business Market Insights is a

market research platform that provides subscription service for industry and

company reports. Our research team has extensive professional expertise in

domains such as Electronics & Semiconductor; Aerospace & Defense;

Automotive & Transportation; Energy & Power; Healthcare; Manufacturing

& Construction; Food & Beverages; Chemicals & Materials; and

Technology, Media, & Telecommunications.

Contact Us

If you have any questions about

this report or would like further information, please contact us:

Contact person: Ankit Mathur

Email: sales@businessmarketinsights.com

Phone: +16467917070

Comments

Post a Comment