Wireless Infrastructure Market Industry Outlook with 7.50% CAGR Growth Potential

Global digital transformation initiatives are driving the advancement of the Wireless Infrastructure Industry. Key growth factors include the widespread deployment of 5G technology, surging mobile data consumption, and the growing need for scalable communication networks capable of supporting billions of connected IoT devices and emerging real-time applications.

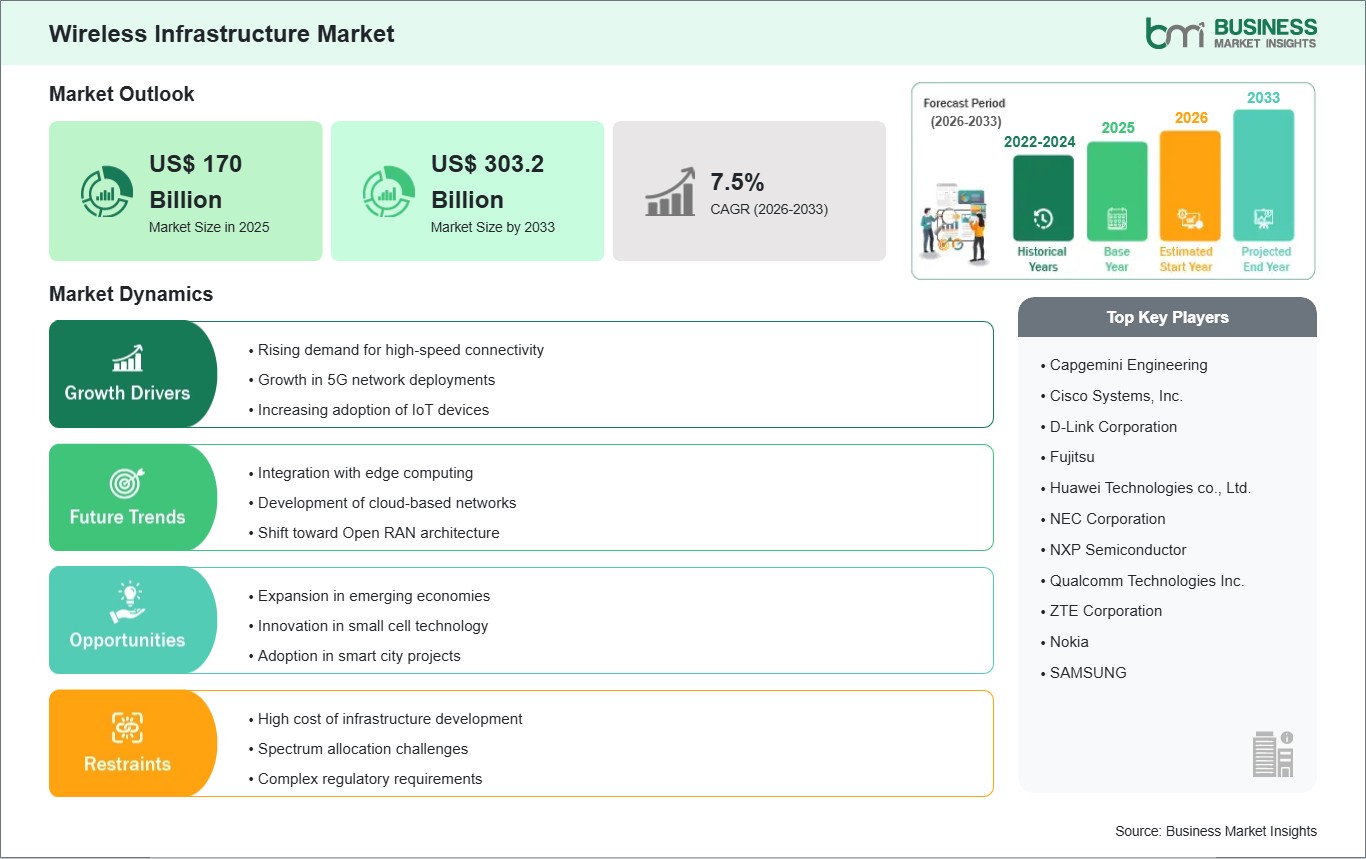

Business Market Insights projects the global Wireless

Infrastructure Market to grow substantially, reaching US$ 303.2 billion by

2033 from US$ 170 billion in 2025. The market is expected to record a CAGR of

7.50% over the forecast period spanning 2026 to 2033.

Advancements in Cloud Radio Access Networks (C-RAN), the

aggressive densification of urban small cell deployments, and the integration

of Massive MIMO (Multiple-Input Multiple-Output) antenna configurations are

fundamentally reshaping the competitive landscape. Global telecommunications

operators and neutral host providers are heavily prioritizing Open RAN (O-RAN)

architectures, edge-computing nodes, and advanced fiber backhaul integrations

to optimize spectrum efficiency, drastically reduce network latency, and

support next-generation smart city applications seamlessly.

What Is Wireless Infrastructure?

Wireless Infrastructure encompasses a comprehensive,

interconnected ecosystem of hardware components, antenna arrays, and

specialized software protocols engineered to transmit, receive, and route radio

frequency (RF) signals between mobile endpoints and the core telecommunications

network. This foundational architecture enables wireless connectivity for

everything from consumer smartphones and enterprise Wi-Fi networks to

autonomous vehicles and industrial smart factory arrays.

Modern wireless network deployments have evolved far beyond

traditional standalone cell towers. A contemporary infrastructure grid

integrates a tiered approach, utilizing high-power Macrocells for broad

geographic coverage, interwoven with thousands of localized Small Cells and

Distributed Antenna Systems (DAS) to provide dense, high-capacity signals

within urban canyons, sports stadiums, and large corporate campuses. The data

captured by these radio nodes is subsequently processed by centralized Baseband

Units (BBUs) and routed through high-speed fiber optic backhaul lines into the

global internet backbone.

Download Sample Report: https://www.businessmarketinsights.com/sample/BMIPUB00032486

Market Drivers

A primary driver for the Wireless Infrastructure Industry is

the accelerated global rollout of standalone (SA) 5G networks. Unlike previous

4G LTE generations, true 5G requires operating on higher-frequency

millimeter-wave (mmWave) spectrums. Because these high-frequency signals cannot

easily penetrate buildings or travel long distances, telecom operators are

forced to aggressively densify their networks, driving massive capital

procurement cycles for millions of new small cell nodes, localized antennas, and

remote radio heads (RRH).

The explosive growth of the Industrial Internet of Things

(IIoT) and Industry 4.0 automation serves as another vital market driver.

Modern manufacturing plants, logistics hubs, and automated ports are rapidly

transitioning away from wired ethernet connections toward Private 5G LTE

networks. These dedicated enterprise networks require localized, on-premise

wireless infrastructure to guarantee the ultra-low latency and absolute data

security necessary to coordinate high-speed robotics and automated guided vehicles

(AGVs) in real time.

Furthermore, the soaring consumer demand for uninterrupted

high-bandwidth streaming, cloud gaming, and augmented reality (AR) applications

is forcing carriers to constantly upgrade legacy equipment. Operators are

heavily investing in Cloud-RAN (C-RAN) architectures that virtualize baseband

processing, allowing them to dynamically allocate network resources during peak

traffic hours, drastically reducing hardware bottlenecks at individual cell

sites.

Market Segmentation

By Component

- Macrocells

- Small

Cells (Femtocells, Picocells, Microcells)

- Distributed

Antenna Systems (DAS)

- Remote

Radio Heads (RRH)

- Baseband

Units (BBU)

- Carrier

Wi-Fi

By Infrastructure Type

- 2G/3G

(Legacy Phase-Out)

- 4G/LTE

- 5G

Standalone & Non-Standalone

- Satellite

Connectivity

By End-User Environment

- Urban

& Dense Urban

- Suburban

& Rural

- Enterprise

& Industrial Facilities

- Public

Venues (Airports, Stadiums)

The Macrocell segment currently captures a dominant portion

of the overall market volume, serving as the critical wide-area baseline for

all global cellular coverage. However, the Small Cells technology division

represents the fastest-growing component segment by value. This hyper-growth is

propelled by the strict necessity to deploy dense small cell clusters on

utility poles and streetlamps to support the short-range propagation physics of

5G mmWave frequencies.

Regional Insights

- Asia-Pacific commands

the largest and fastest-growing share of the global wireless

infrastructure market, fueled by massive, state-backed 5G expansion

initiatives, highly concentrated urban populations, and intensive smart

manufacturing modernizations surging rapidly across China, South Korea,

Japan, and India.

- North

America represents an exceptionally high-value, mature market

footprint, heavily anchored by aggressive telecom capital expenditures,

the rapid commercialization of fixed wireless access (FWA) broadband

solutions, and robust regulatory support for Open RAN ecosystem

developments across the United States.

- Europe maintains

a highly stable market presence, catalyzed by strict European Union

digital decade targets, robust investments in cross-border 5G highway

corridors for autonomous driving, and strong regional pushes for

energy-efficient, green telecom infrastructure.

- Middle

East & Africa and South & Central America are

demonstrating steady incremental volume growth, led by massive smart city

mega-projects (such as NEOM in Saudi Arabia) and ongoing efforts to bridge

the rural digital divide via expanded 4G LTE reach and low-earth orbit

(LEO) satellite backhaul integrations.

Top Players in the Wireless Infrastructure Industry

The competitive marketplace features a high level of

consolidation among a few global telecommunications equipment heavyweights,

alongside an emerging ecosystem of specialized software firms pushing

open-source virtualization standards.

- Ericsson

AB

- Nokia

Corporation

- Huawei

Technologies Co., Ltd.

- ZTE

Corporation

- Samsung

Electronics Co., Ltd.

- Cisco

Systems, Inc.

- NEC

Corporation

- CommScope

Holding Company, Inc.

- Corning

Incorporated

- Fujitsu

Limited

Technological Innovations

The architectural shift toward Open Radio Access Networks

(O-RAN) is fundamentally democratizing modern cellular deployments.

Historically, telecom operators were locked into purchasing proprietary

hardware and software from a single vendor, making upgrades costly and rigid.

O-RAN standards disaggregate the network by introducing open interfaces,

allowing operators to mix and match radio units from one vendor with baseband

processing software from another. This interoperability fosters intense

competition, lowers deployment costs, and accelerates the introduction of

AI-driven network management tools.

Concurrently, the manufacturing landscape is rapidly

integrating Massive MIMO (Multiple-Input Multiple-Output) antenna technologies.

Traditional cell towers broadcast a single, wide beam of signal in a 120-degree

arc, wasting energy on empty spaces. Massive MIMO arrays utilize dozens or even

hundreds of miniature antennas on a single panel to employ

"beamforming." This technology dynamically shapes and focuses

individual, dedicated signal beams directly at active user devices as they

move, multiplying the total capacity of the cell site and drastically improving

connection stability for edge users.

Future Market Outlook

The future outlook for the Wireless Infrastructure Industry

remains exceptionally robust. As global commercial, urban, and industrial

infrastructures transition completely toward hyper-connected, software-defined

ecosystems, the demand for underlying bandwidth and ultra-reliable, low-latency

communications will only amplify.

Future development will be deeply concentrated in 6G

research initiatives leveraging terahertz (THz) spectrum bands, the widespread

integration of edge-computing server blades directly at the base of cell towers

to process AI tasks locally, and the deployment of "Zero-Touch"

autonomous networks that use machine learning to self-heal and re-route traffic

instantly during hardware failures. Technology providers that deliver scalable,

vendor-neutral hardware frameworks pairing high capacity with extreme energy

efficiency will successfully secure long-term global market dominance.

Frequently Asked Questions (FAQs)

What is the difference between a Macrocell and a Small

Cell in a cellular network?

A Macrocell is a traditional, high-power cell tower that

provides broad network coverage over several miles, designed to serve a wide

geographic area. A Small Cell is a low-power, miniaturized radio node installed

on streetlights or building walls that covers a very short range (often just a

few city blocks). Small cells are deployed densely to offload traffic from the

Macrocell and provide high-speed capacity in crowded urban areas.

How does a Distributed Antenna System (DAS) improve

indoor wireless connectivity?

Radio signals struggle to penetrate thick concrete, steel,

or energy-efficient glass used in large buildings, causing indoor dead zones. A

Distributed Antenna System (DAS) solves this by taking a strong cellular signal

source and distributing it through a wired network of small indoor antennas

placed throughout a stadium, hospital, or corporate campus, ensuring seamless

connectivity regardless of the building's physical structure.

Why is fiber-optic backhaul critical for modern 5G

wireless infrastructure?

While the connection from a user's phone to the cell tower

is wireless, the tower itself must connect back to the core internet a

connection known as "backhaul." 5G networks process exponentially

more data at much lower latencies than previous generations. Only high-capacity

fiber-optic cables possess the immense bandwidth and speed necessary to

transfer this massive data payload from the cell site to the core network

without creating a crippling bottleneck.

What role does virtualized Cloud-RAN (C-RAN) play in

network efficiency?

In traditional setups, every cell tower requires its own

dedicated, energy-intensive baseband processing computer at its base. Cloud-RAN

(C-RAN) virtualizes this processing power, moving the computing hardware away

from individual towers and consolidating it into a centralized, highly

efficient data center. This allows operators to pool computing resources, lower

hardware costs at the cell site, and instantly shift processing power to

whichever tower is experiencing peak traffic.

Browse More Reports:

Photolithography Equipment Market

Plate and Frame Heat Exchanger Market

About Us

Business Market Insights is a market research platform that

provides subscription service for industry and company reports. Our research

team has extensive professional expertise in domains such as Electronics &

Semiconductor; Aerospace & Defense; Automotive & Transportation; Energy

& Power; Healthcare; Manufacturing & Construction; Food &

Beverages; Chemicals & Materials; and Technology, Media, &

Telecommunications.

Contact Us

If you have any questions about this report or would like

further information, please contact us:

Contact person: Ankit Mathur

Email: sales@businessmarketinsights.com

Phone: +16467917070

Comments

Post a Comment