Investing in High-Performance Energy-Absorbing Vehicle Framing Components: The $124.67 Billion Opportunity

Technological advancements in advanced high-strength steel

(AHSS), aluminum alloys, magnesium components, engineering thermoplastics,

carbon-fiber-reinforced composites, and multi-material vehicle architectures

are transforming the automotive lightweight materials industry. These

innovations are improving structural integrity, crash performance, corrosion

resistance, manufacturing efficiency, and energy efficiency while expanding

applications across vehicle bodies, chassis systems, battery enclosures, and powertrain

components.

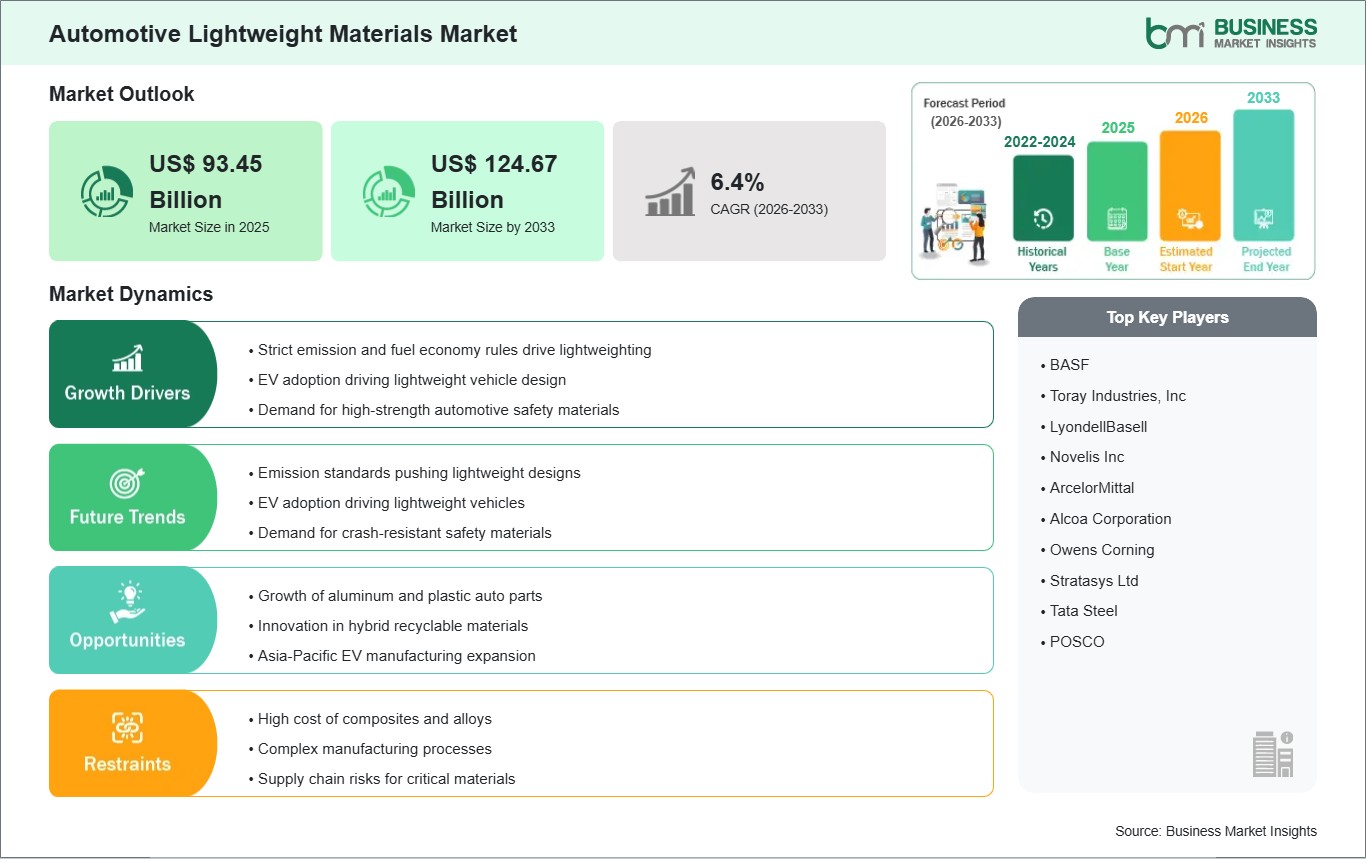

According to Business Market Insights, the global Automotive

Lightweight Materials Market is anticipated to grow at a CAGR of 3.67%

throughout the forecast period. Increasing demand for lightweight vehicle

structures, expanding electric vehicle production, and continuous innovation in

advanced material technologies are expected to propel the market from US$ 93.45

billion in 2025 to US$ 124.67 billion by 2033.

The underlying structural and functional utility of advanced

high-strength steels and light alloy extrusions relies heavily on accurate

crystal structure orientations, precision hot-stamping processing lines, and

uniform fiber-resin distribution interfaces. When utilized within high-capacity

press shops, robotic body assembly zones, or custom powertrain fabrication

centers, these materials must absorb collision energy predictably, resist

environmental corrosion, and maintain high structural stiffness without

introducing part stamping fractures or extensive tooling wear. Shifting toward

advanced laser-welded blanks, tailored rolling protocols, and automated resin

transfer molding setups allows vehicular design teams to seamlessly regulate

localized tensile strengths, optimize specific stiffness ratios, and isolate

heavy battery arrays from external impact forces. This high level of structural

material performance provides continuous manufacturing uniformity, lowers

overall lifecycle production scrap, and equips mechanical engineers with the

exact tool configurations required to supervise complex assembly sequences

smoothly.

Automotive Lightweight Materials Market Analysis

An intensive Automotive Lightweight Materials Market

analysis demonstrates that the industry is organized into distinct physical

material classifications, targeted component assembly applications, and primary

vehicular usage fields to satisfy rigid manufacturing benchmarks and

international transportation safety criteria. By material type, the marketplace

is segmented into High-Strength Steel, Aluminum, Magnesium, Plastics and

Composites, and Others. High-strength steel layouts maintain a major volume position

within global factory supply chains due to their exceptional structural

predictability, proven crash-energy absorption characteristics, and direct

drop-in compatibility with traditional high-volume welding and stamped framing

lines. Concurrently, advanced aluminum alloys are seeing accelerated

procurement across large-scale chassis networks and structural battery

enclosures, where reducing dead-weight is crucial for lowering rolling

resistance and boosting the thermal management efficiencies of modern electric

vehicle configurations.

When evaluating the specific automotive layout components

and vehicle segments that consume these premium structural materials, the

industrial ecosystem highlights an extensive footprint across multiple

structural and functional systems. By application, the industry is categorized

into Body-in-White (BIW), Powertrain, Chassis and Suspension, Interiors, and

Others. The Body-in-White (BIW) division stands as the primary volume driver

within the structural framework, heavily propelled by the rising global requirement

to build safe protective occupant cages that remain thin and lightweight. At

the same time, the powertrain and interior segments are expanding their

procurement of engineering plastics and continuous fiber laminates, replacing

complex zinc die-cast brackets and heavy structural cross-beams with

lightweight composite elements directly on the final assembly floor.

Download Sample PDF - https://www.businessmarketinsights.com/sample/BMIPUB00033668

Market Size and Projections: 2025–2033

The economic scale of the global metallurgical sector,

automated metal forming installations, and certified composite formulation

networks highlights a deep international commitment to advancing structural

vehicle efficiencies. This steady market expansion is structurally

sustained by the expanding worldwide vehicle manufacturing volume, increasing

integration of massive battery modules requiring weight compensation elsewhere

on the chassis, broader deployment of strict fuel efficiency regulations, and a

continuous corporate emphasis on embedding automated multi-material joining

technologies into standard assembly networks globally.

Market Segmentation

To provide an analytical breakdown of this high-precision

vehicular engineering and validation industry, the global market is structured

into the following explicit divisions:

- By

Material Type: High-Strength Steel, Aluminum, Magnesium, Plastics

and Composites, Others.

- By

Application: Body-in-White (BIW), Powertrain, Chassis and

Suspension, Interiors, Others.

Feature Outlook

The future performance profile and technical properties of

next-generation structural vehicle materials are defined by an industry

transition toward multi-material hybrid joining methods, recycled aluminum

alloys, and automated additive tool setups. Modern feature outlooks emphasize

the manufacturing integration of advanced self-piercing riveting and structural

adhesive technologies directly into traditional welding lines, enabling field

assembly lines to blend aluminum sheets with high-strength steel frames without

generating galvanic corrosion risks. Furthermore, upcoming material

configurations focus on ultra-thin carbon fiber mats, bio-based plastic

matrices, and structural magnesium castings engineered to handle complex

under-hood structural parts cleanly. This technical progress allows material

batches to achieve high structural uniformity over continuous processing runs,

optimizing component tool lifespans and preventing production delays across all

processing environments.

Competitive Landscape: Top Industry Players

The competitive landscape of the market is defined by

continuous alloy chemistry innovations, strict compliance with international

automotive crash safety frameworks, and multi-year supply contracts with major

global vehicle assembly groups and Tier-1 structural components networks

worldwide. Top tier raw material suppliers secure market prominence by

maximizing tensile yields, optimizing metal grain structures to resist

macro-cracking, and creating open-protocol stamping configurations that combine

with existing factory tool layouts smoothly. The top players operating within

the global market space include:

- BASF

- Toray

Industries, Inc

- LyondellBasell

- Novelis

Inc

- ArcelorMittal

- Alcoa

Corporation

- Owens

Corning

- Stratasys

Ltd

- Tata

Steel

- POSCO

These prominent industry participants concentrate their

corporate efforts on developing highly stable aluminum casting lines for

complex EV rear-underbody frames, manufacturing durable continuous fiber

thermoplastic formats to lower cycle processing times, and partnering with

sustainable mining and recycling groups to secure a dependable, low-fluctuation

raw material supply chain globally.

More Trending Reports by Business Market Insights:

Brain

Monitoring Devices Market

About Us:

Business Market Insights is a market research platform that

provides subscription service for industry and company reports. Our research

team has extensive professional expertise in domains such as Electronics &

Semiconductor; Aerospace & Defense; Automotive & Transportation; Energy

& Power; Healthcare; Manufacturing & Construction; Food &

Beverages; Chemicals & Materials; and Technology, Media, &

Telecommunications.

Contact us:

If you have any questions about this report or would like

further information, please contact us:

Contact person: Ankit Mathur

Email: sales@businessmarketinsights.com

Phone: +16467917070

Comments

Post a Comment